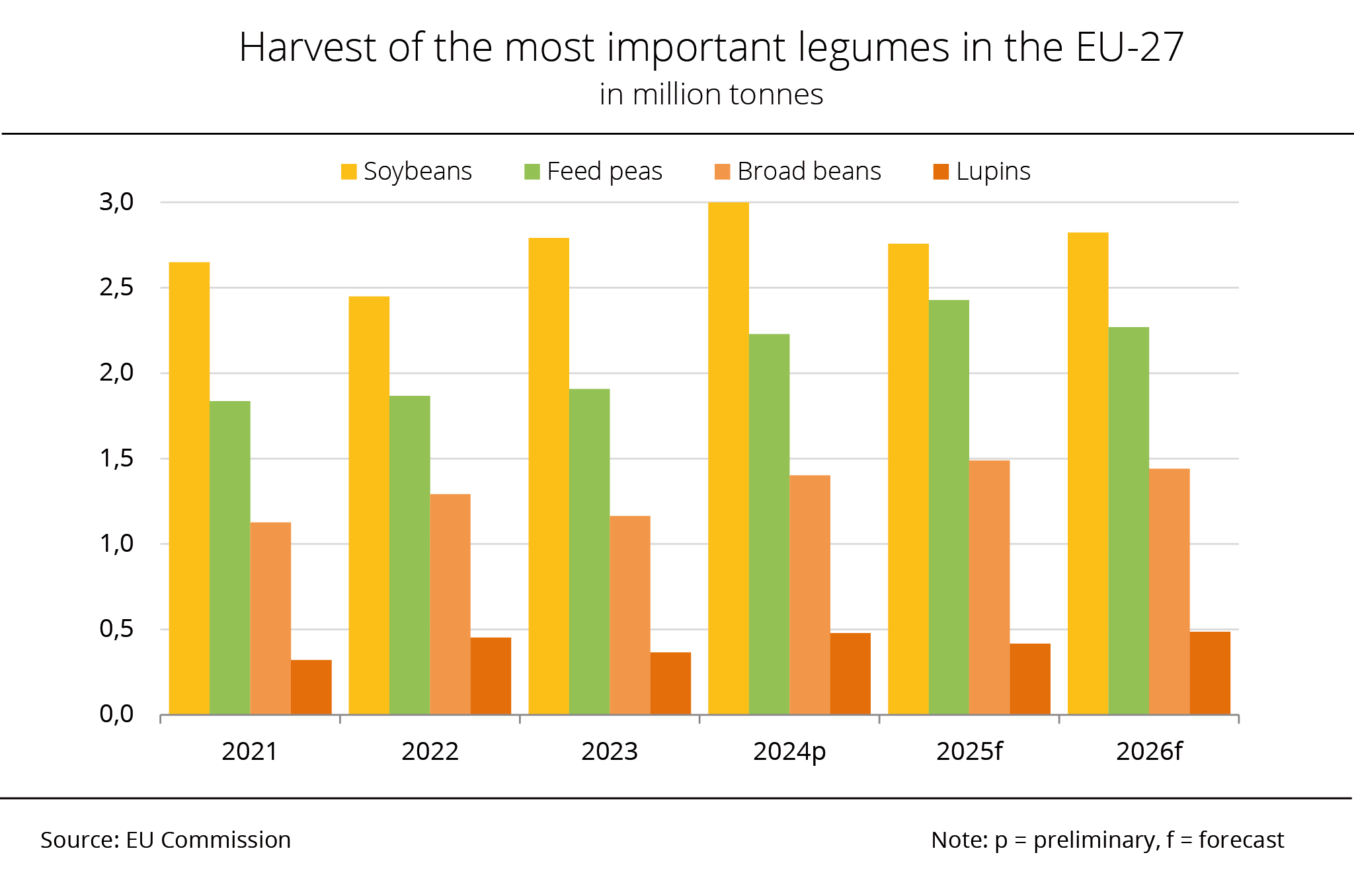

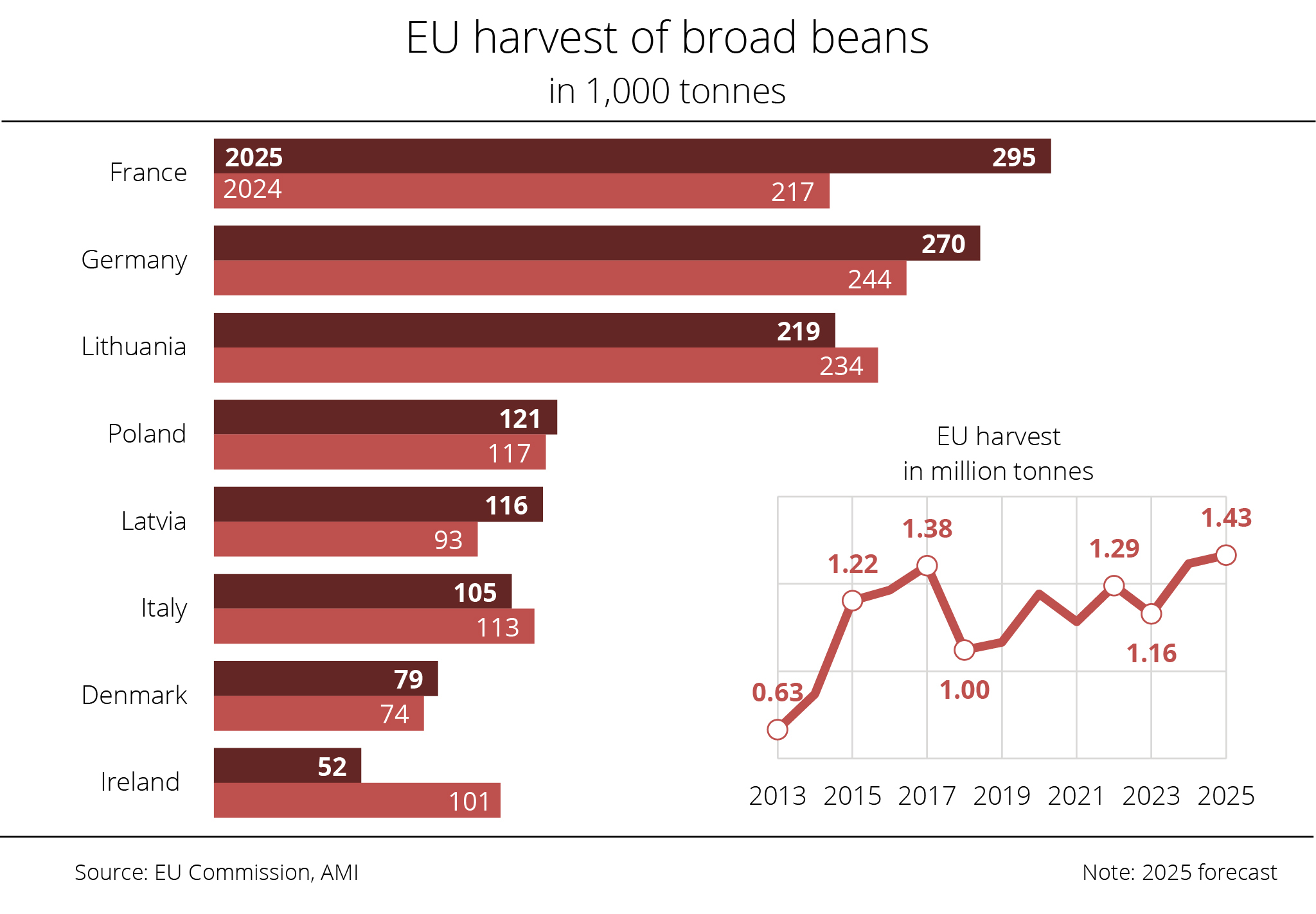

Chart of the week (31 2026): EU Commission estimates broad bean harvest just below previous year's record

Berlin, 29 July 2026 – Production of broad beans has gained considerable importance in the EU. According to the EU Commission, the 2026 harvest is expected to almost reach the previous year's record level. France remains the EU's most important producer of broad beans, followed by Lithuania.

Berlin, 29 July 2026 – Production of broad beans has gained considerable importance in the EU. According to the EU Commission, the 2026 harvest is expected to almost reach the previous year's record level. France remains the EU's most important producer of broad beans, followed by Lithuania.

In its latest estimate, the European Commission projects the 2026 EU broad bean harvest at just over 1.48 million tonnes, a marginal decline from the previous year. The harvest would nevertheless exceed the five-year average of 1.29 million tonnes by just over 15 per cent. At the same time, it would be the second highest production volume on record.

Despite a slight decrease in area planted with broad beans, production is expected to remain virtually steady, as the EU Commission projects higher average yields in key production regions. Given the heatwave at the end of June and the extreme weather events of recent weeks, however, it seems doubtful whether these will actually be achieved, as these circumstances are likely to have reduced the yields of summer crops. Across the EU, broad beans are grown on approximately 523,000 hectares. This translates to a drop of almost 6,000 hectares, or 1.1 per cent, compared with the previous year.

The Union zur Förderung von Oel- und Proteinpflanzen e.V. (UFOP) expects the EU protein strategy recently presented by the EU Commission to provide positive momentum for the long-term stabilisation and further development of the cultivation of broad beans and other grain legumes in Europe. Farmers are keen to grow these crops. However, the benefits these crops provide for biodiversity and greater diversity in crop rotation should be adequately rewarded.

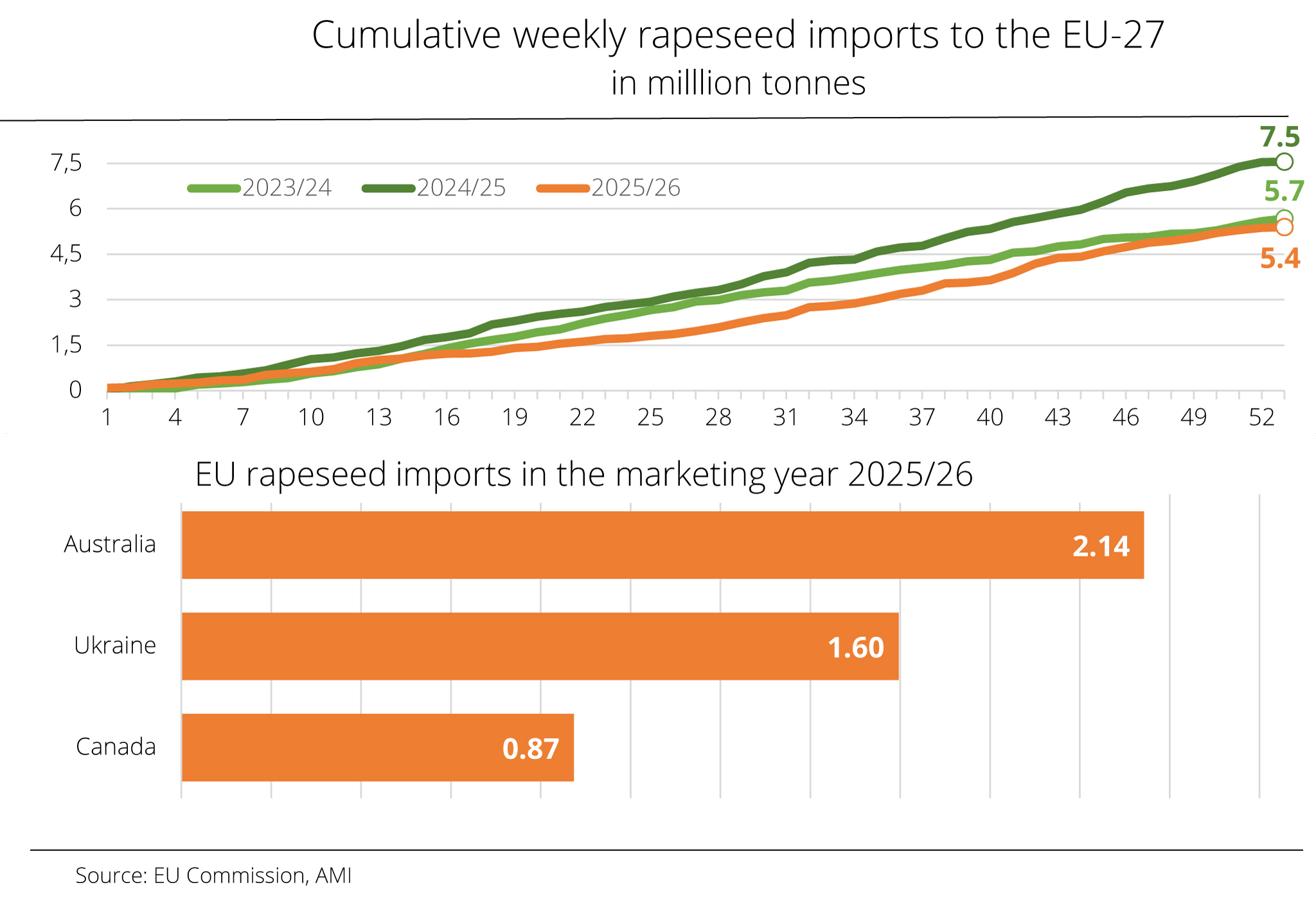

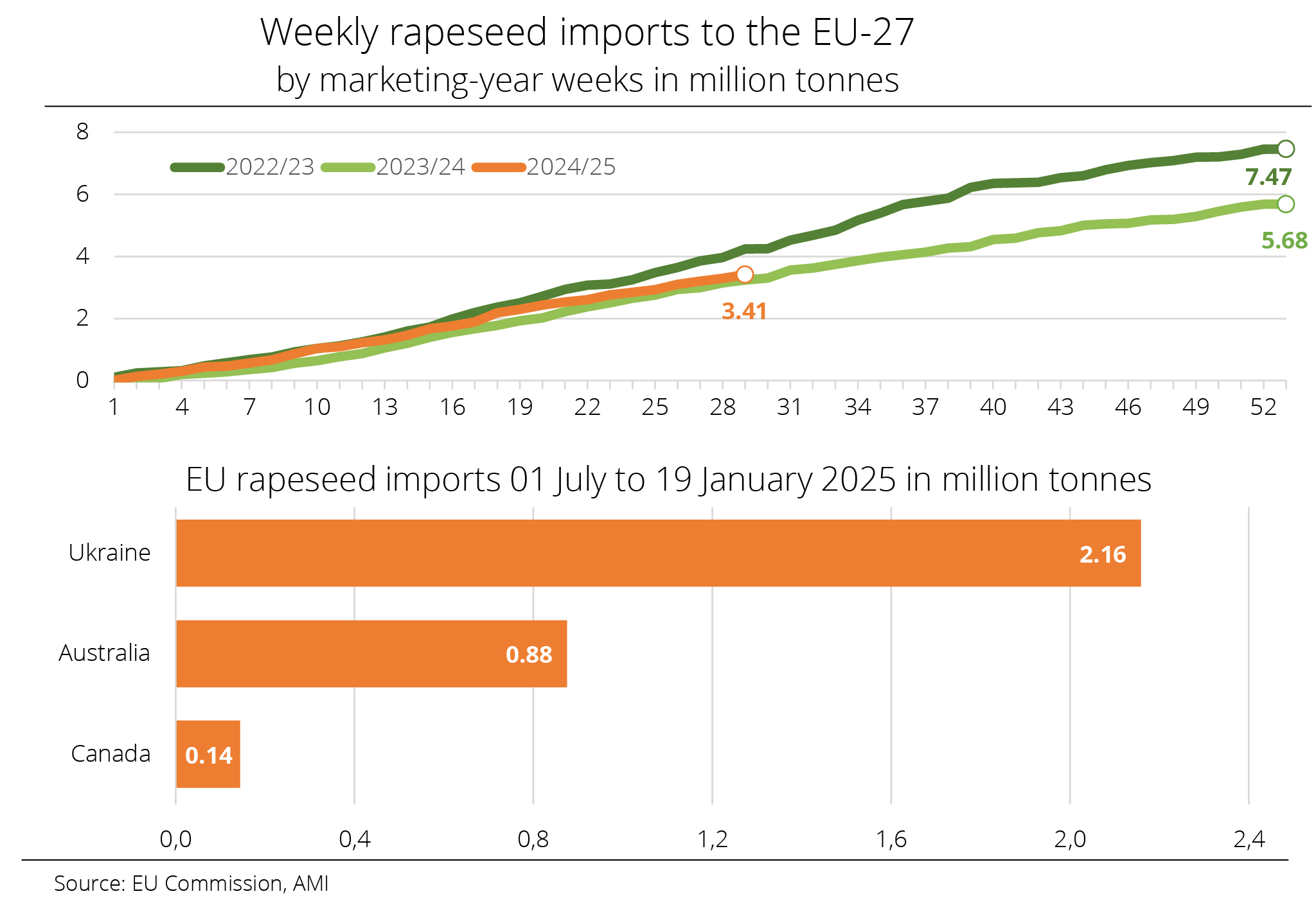

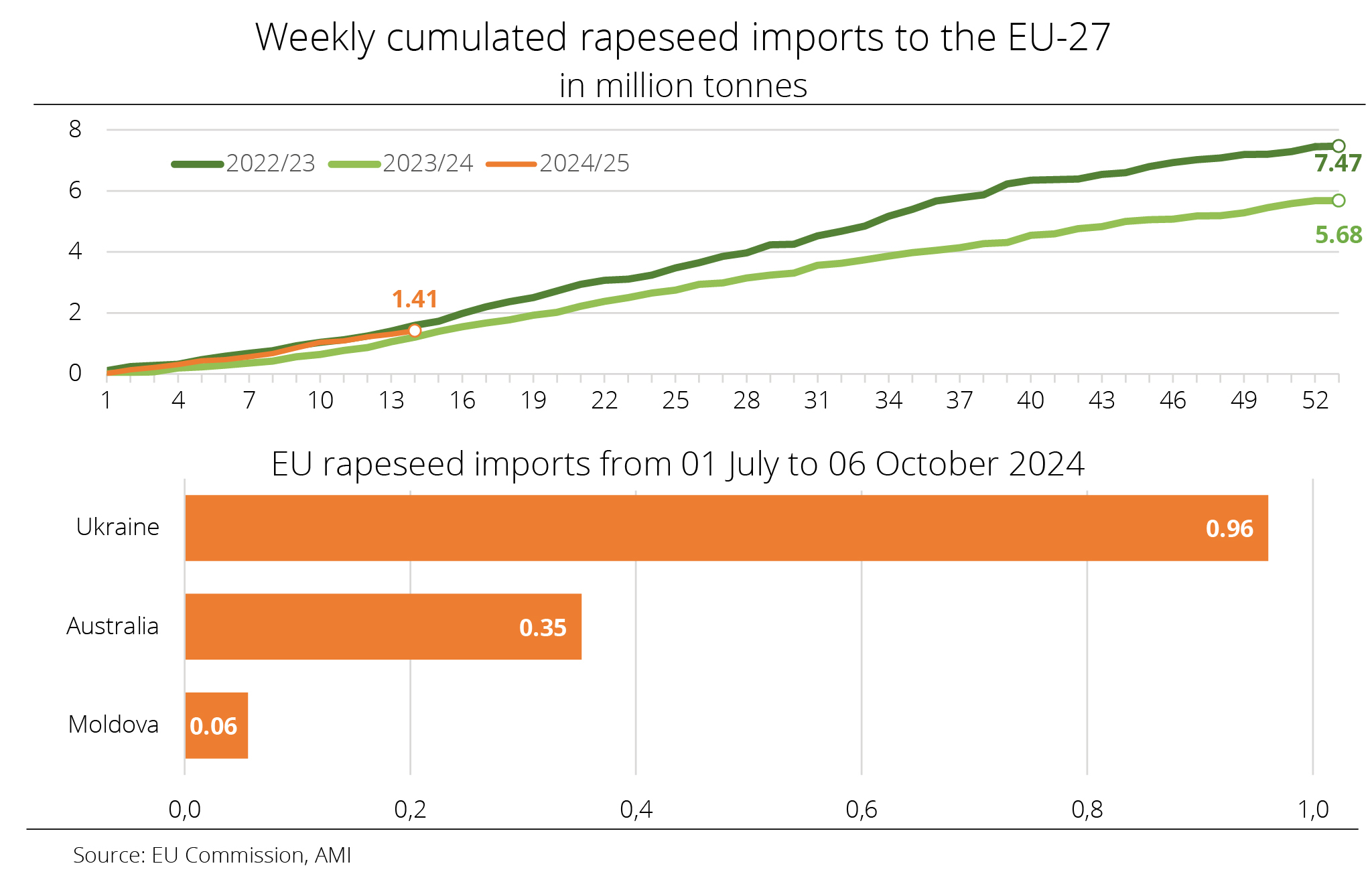

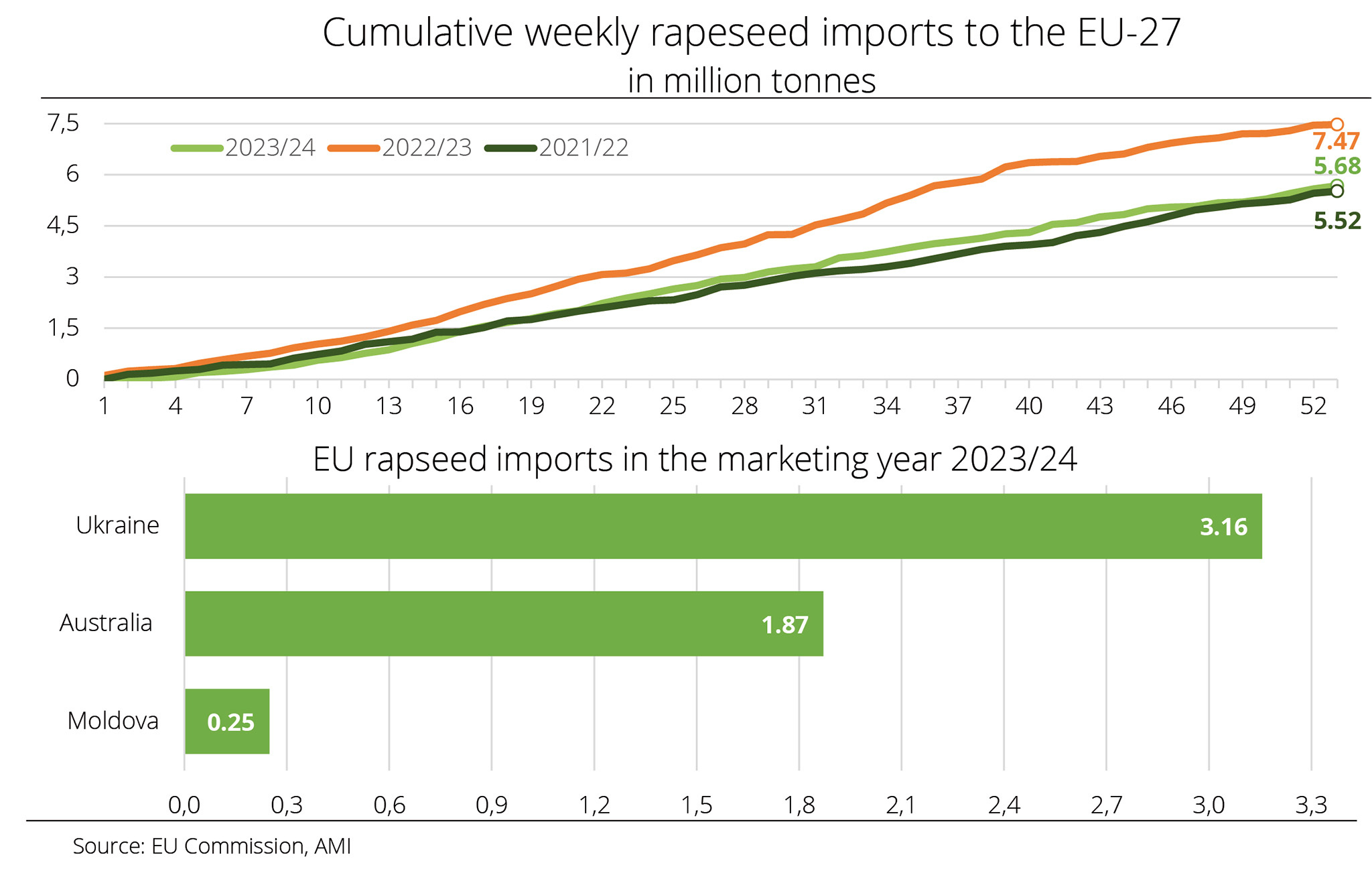

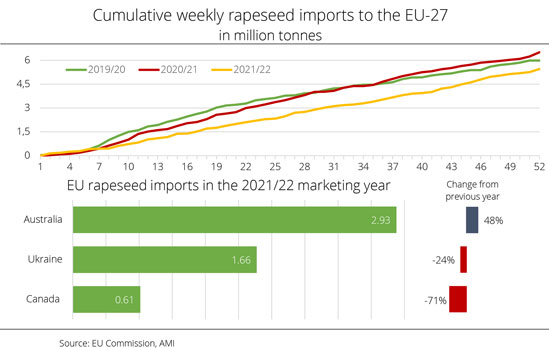

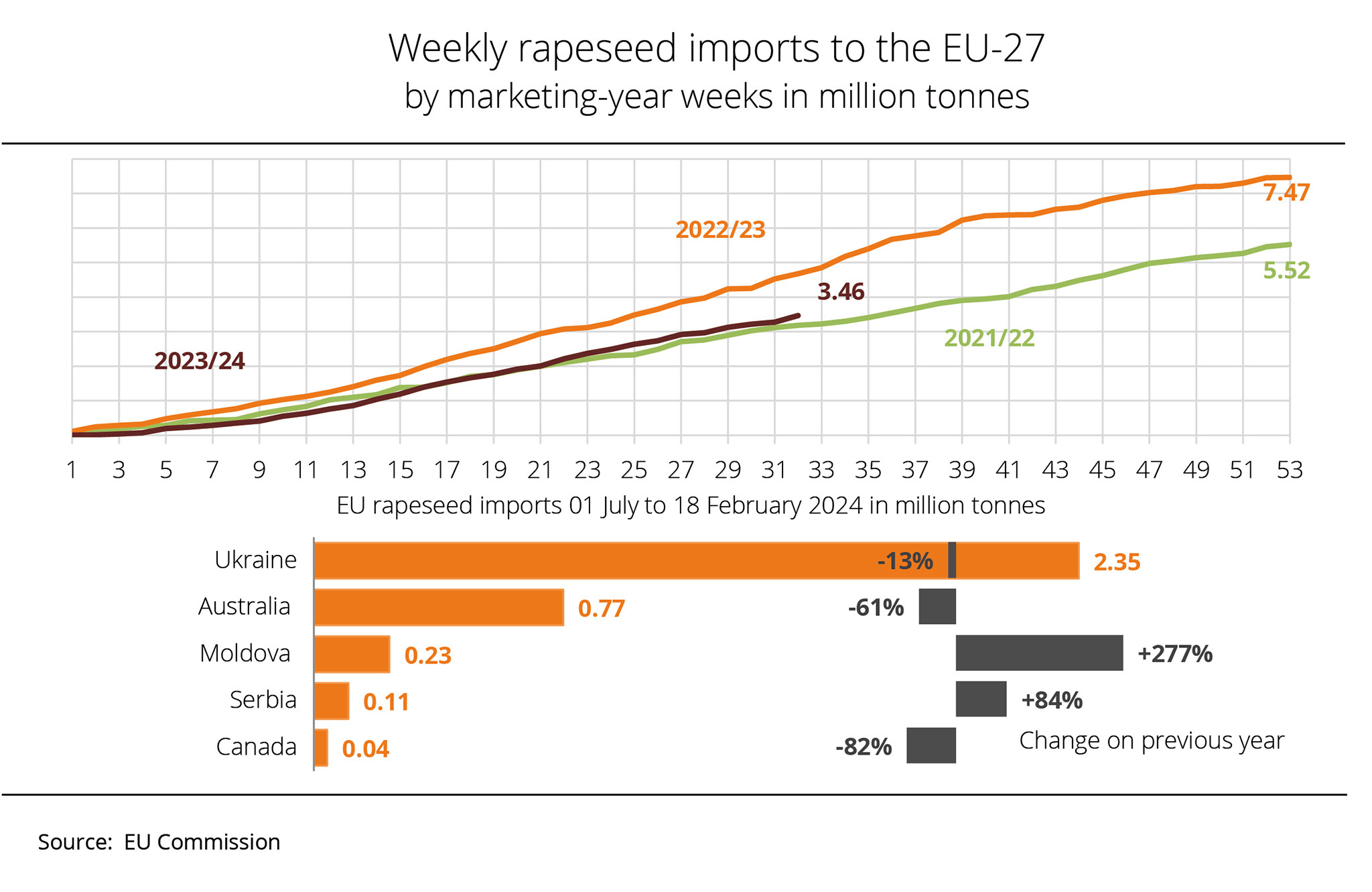

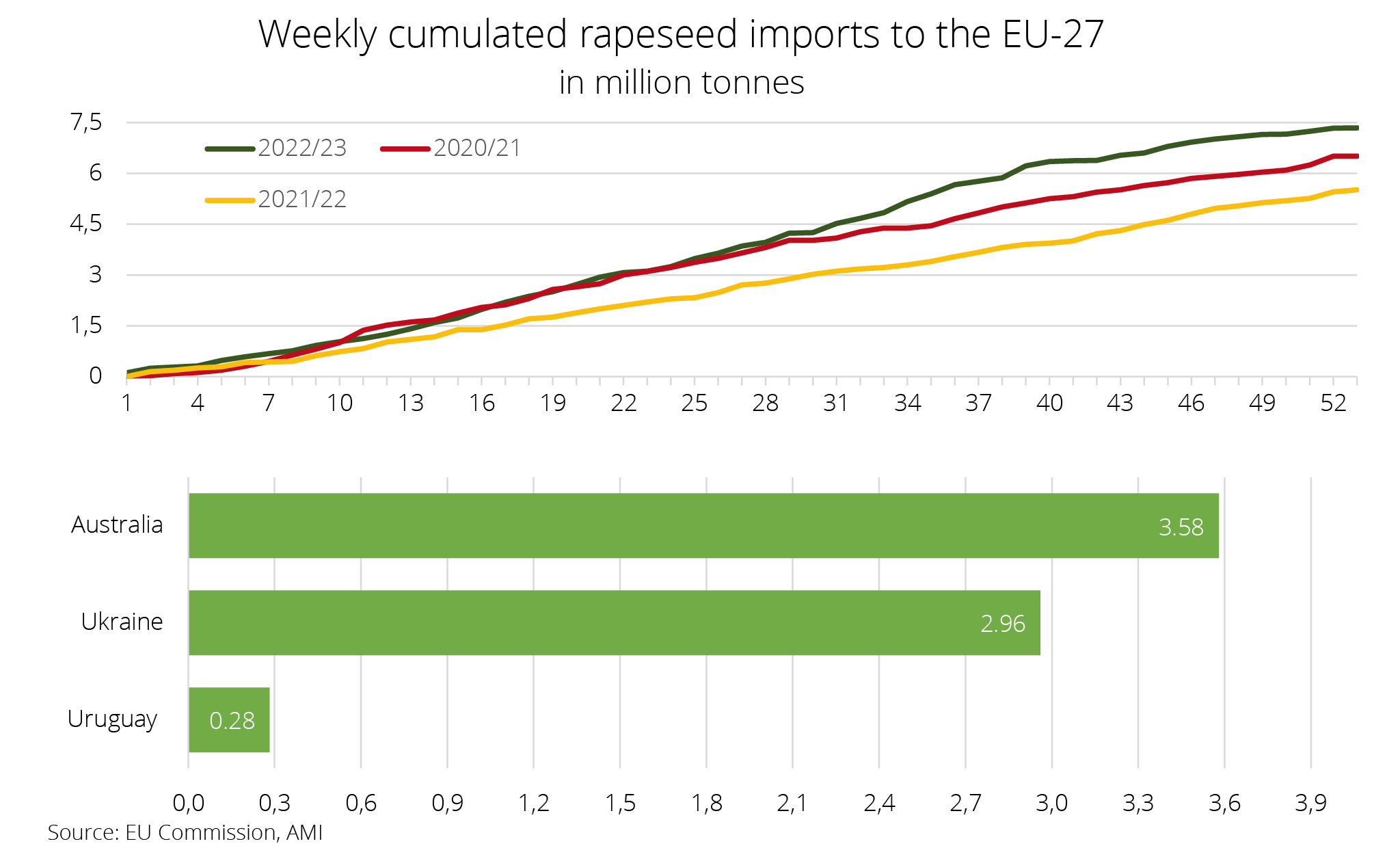

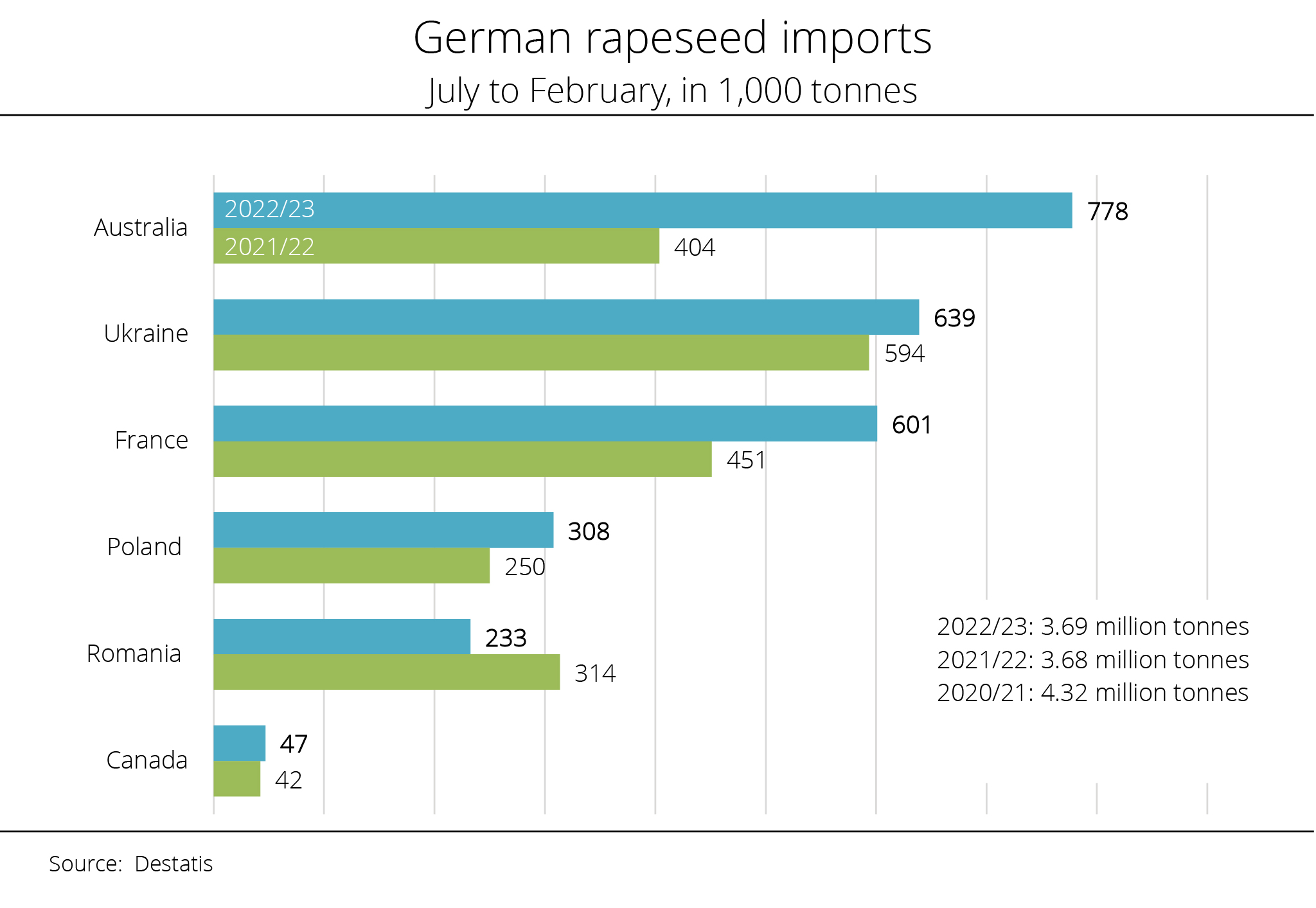

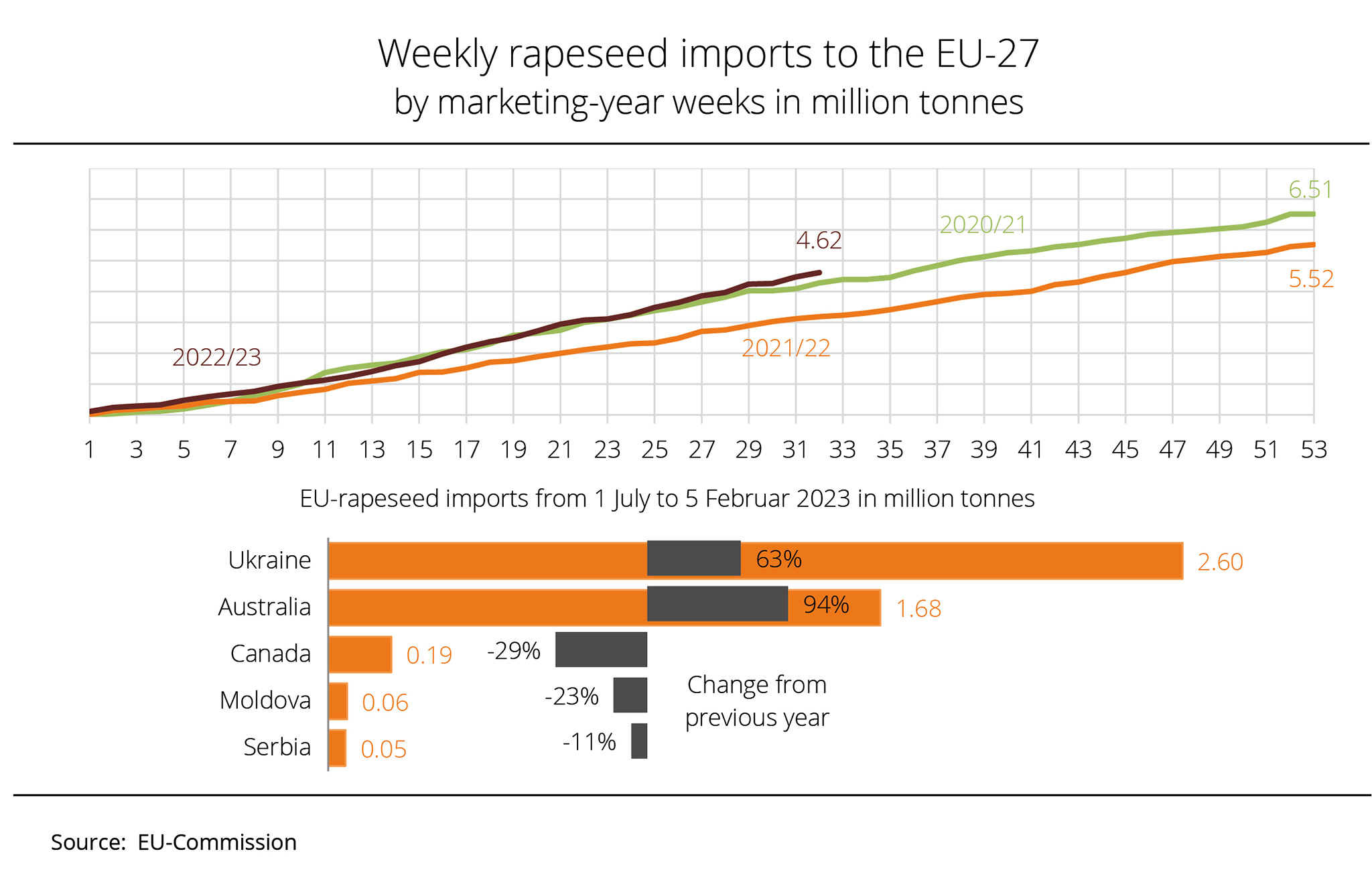

Chart of the week (30 2026): Australia remains the primary rapeseed supplier to the EU

UFOP: Adapt rapeseed cultivation for the 2027 harvest to farms' crop rotation limits

Berlin, 22 July 2026 – According to data from the EU Commission, EU-27 rapeseed imports from non-EU countries during the 2025/26 season fell well short of the previous year's volume of 7.5 million tonnes, reaching 5.4 million tonnes. The EU's import demand declined mainly due to an increase in the EU harvest. The Union zur Förderung von Oel- und Proteinpflanzen (UFOP) is therefore hoping for a similarly good yield from the 2026 EU rapeseed harvest, despite the extreme weather conditions of recent weeks. National quota requirements resulting from the implementation of RED III currently define feedstock demand. This should primarily benefit producers in the EU.

Berlin, 22 July 2026 – According to data from the EU Commission, EU-27 rapeseed imports from non-EU countries during the 2025/26 season fell well short of the previous year's volume of 7.5 million tonnes, reaching 5.4 million tonnes. The EU's import demand declined mainly due to an increase in the EU harvest. The Union zur Förderung von Oel- und Proteinpflanzen (UFOP) is therefore hoping for a similarly good yield from the 2026 EU rapeseed harvest, despite the extreme weather conditions of recent weeks. National quota requirements resulting from the implementation of RED III currently define feedstock demand. This should primarily benefit producers in the EU.

EU rapeseed imports from non-EU countries declined sharply compared to the previous year. The primary supplier countries are Australia and Ukraine. Shipments from Australia declined approximately 41 per cent to 2.1 million tonnes compared to the 2024/25 season. Deliveries from Ukraine dropped around 34 per cent, falling to 1.6 million tonnes. Imports from Canada also fell short of the previous year's volume. At 870,000 tonnes, the country’s exports to the EU remained significantly below the 1.1 million tonnes recorded the previous year. However, because Canadian farmers grow genetically modified varieties, the use of rapeseed oil derived from Canadian sources is restricted in the EU. As a result, imports from Canada are mainly used for biofuel production.

The EU's continued high level of import demand has prompted the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) to call on rapeseed producers to fully utilise their farms' potential for sustainable rapeseed cultivation when planning crop rotation for the 2027 harvest. The UFOP has pointed out that, following the recalculation, the NUTS 2 default greenhouse gas emission saving values for rapeseed used in biofuel production are now significantly better. The association has highlighted that German rapeseed grown on so-called mineral soils shows the best default values for greenhouse gas emission saving in the EU, adding that this locational advantage should be taken into account in sourcing and marketing the feedstock.

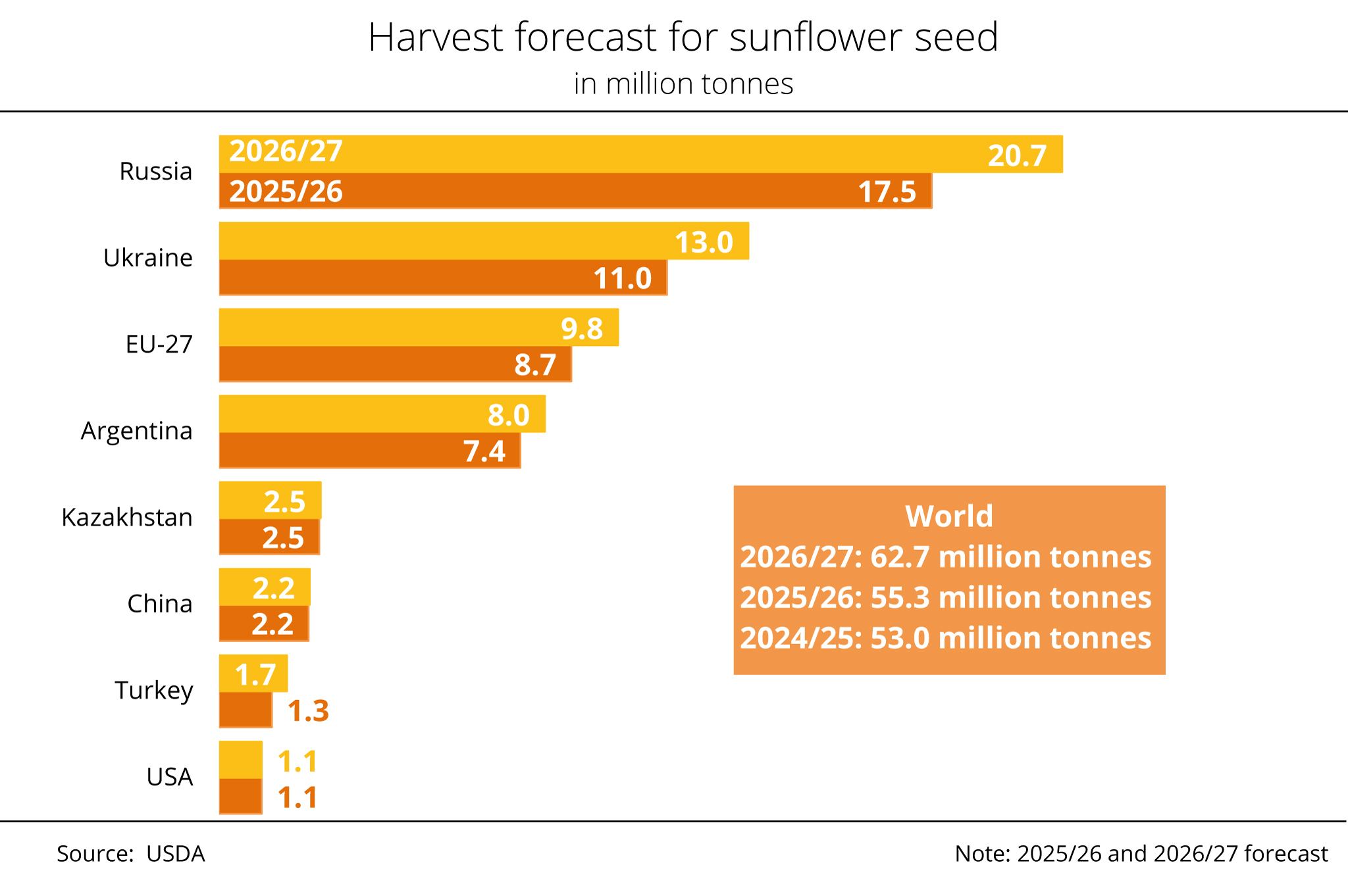

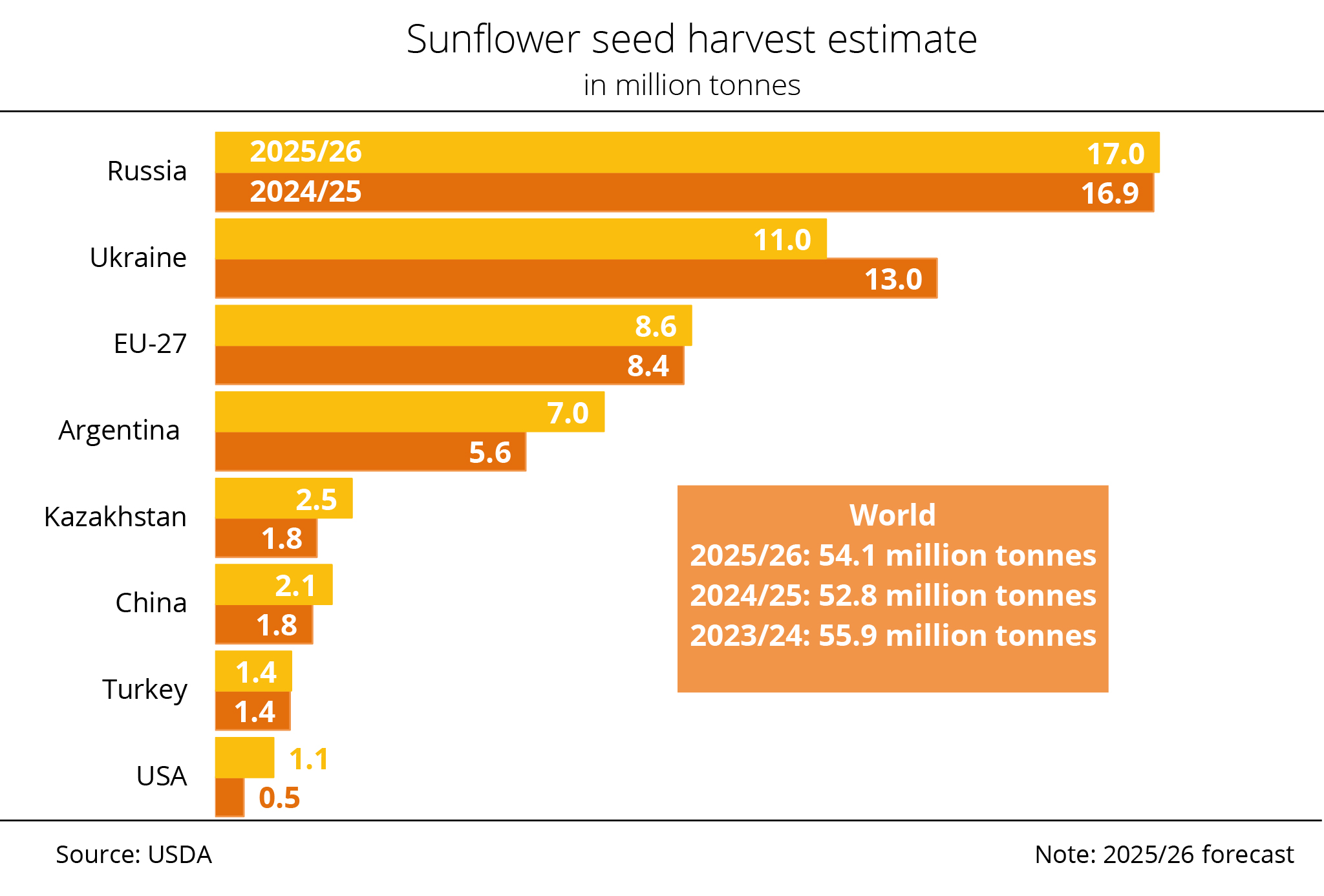

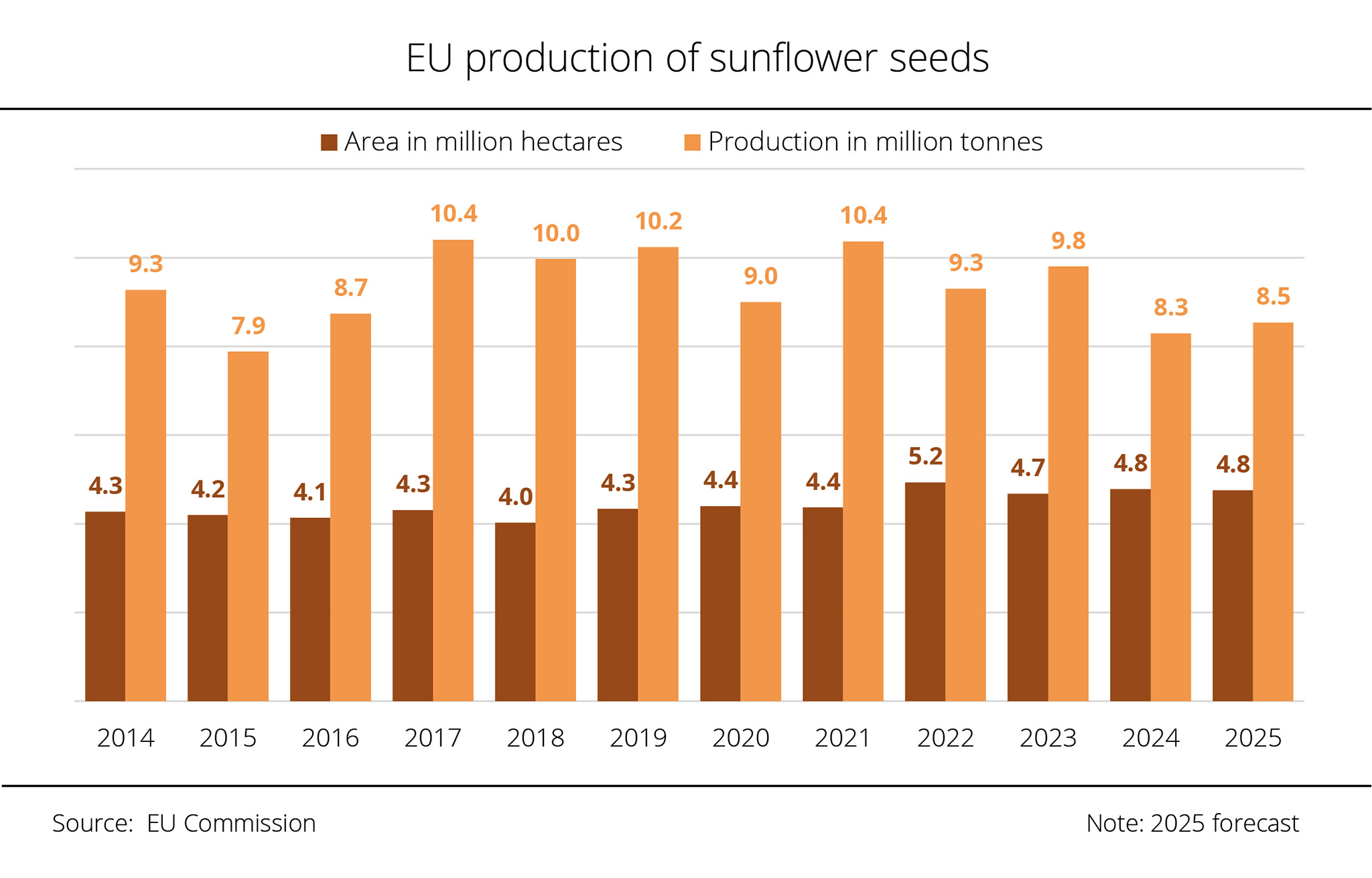

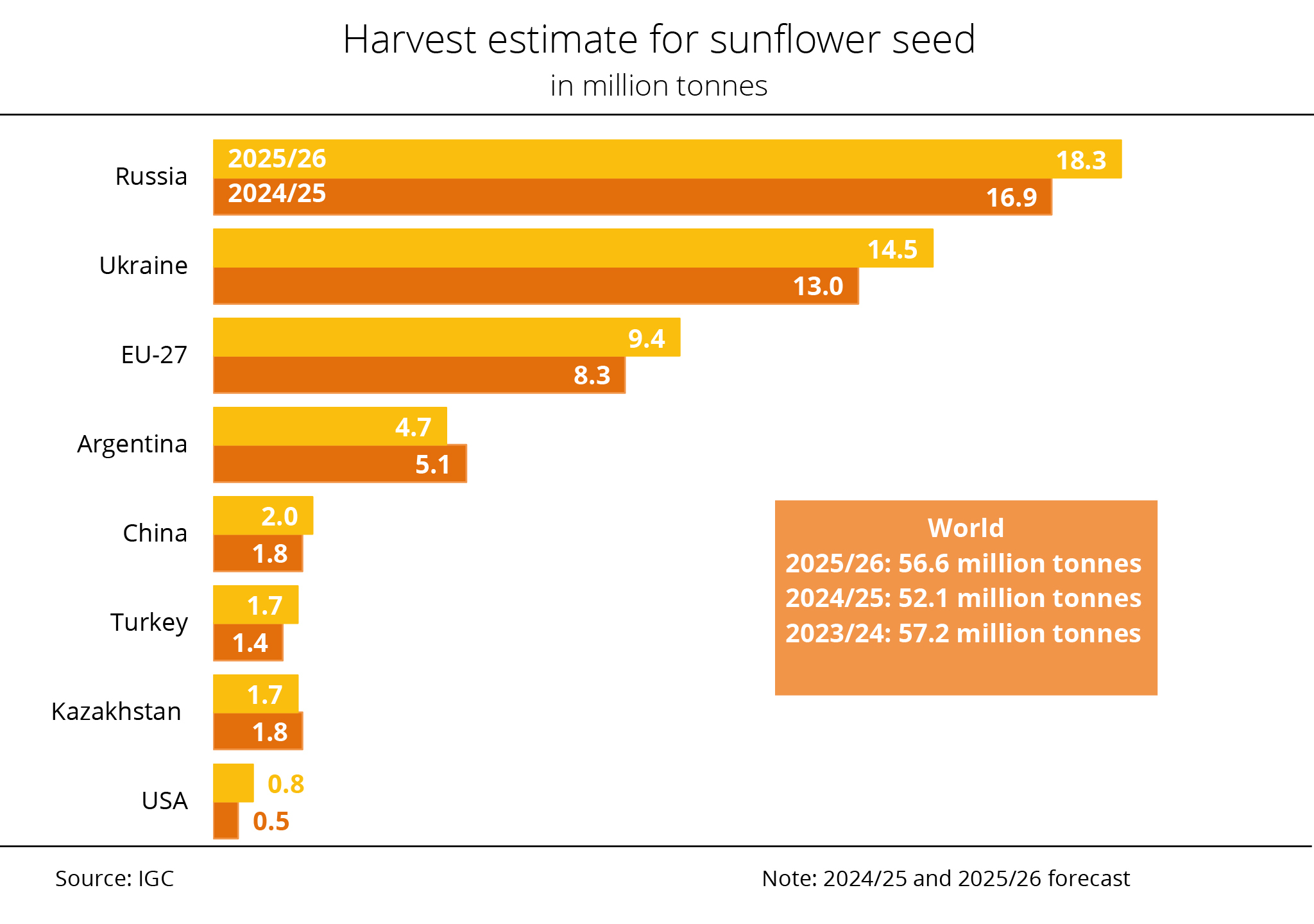

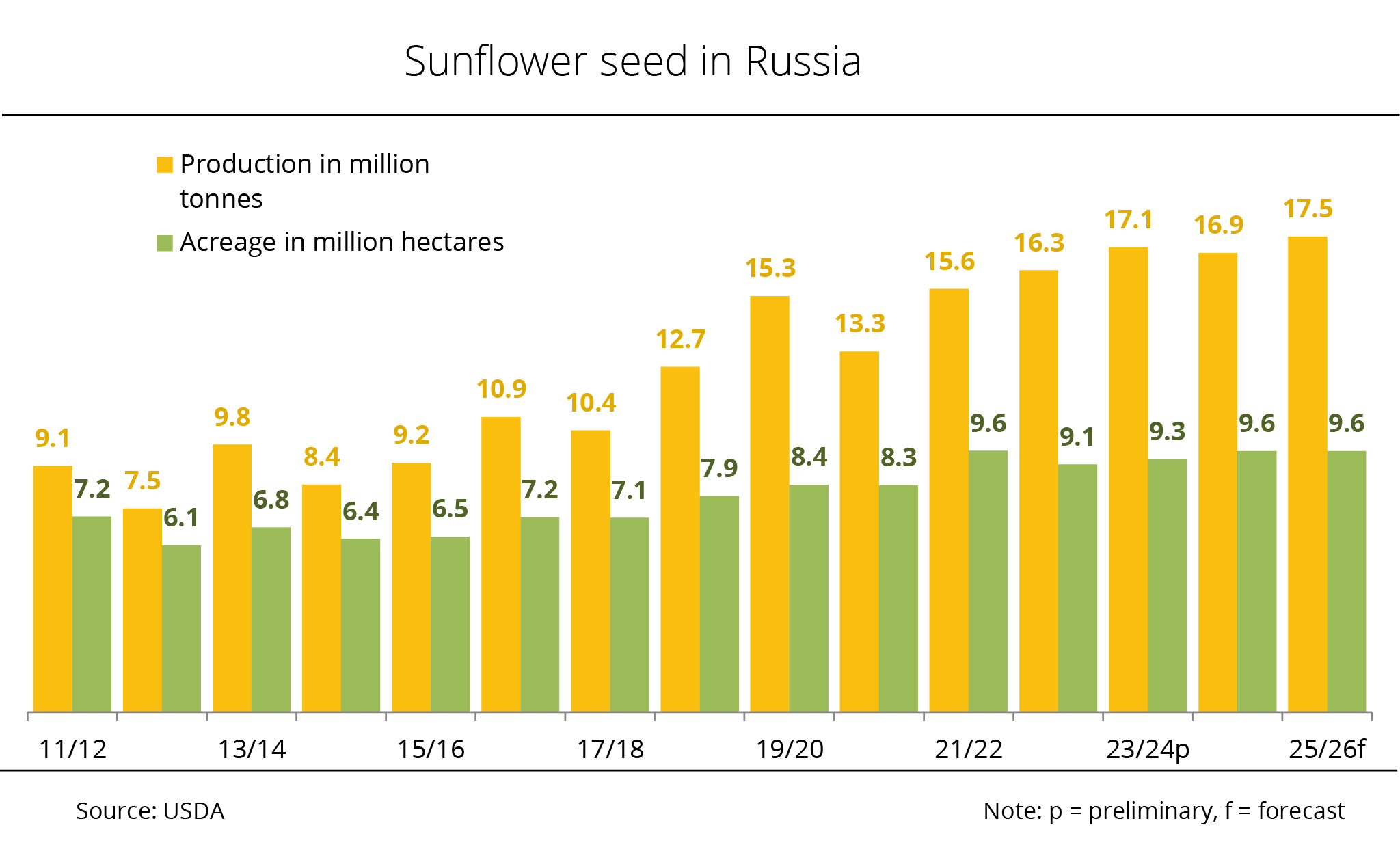

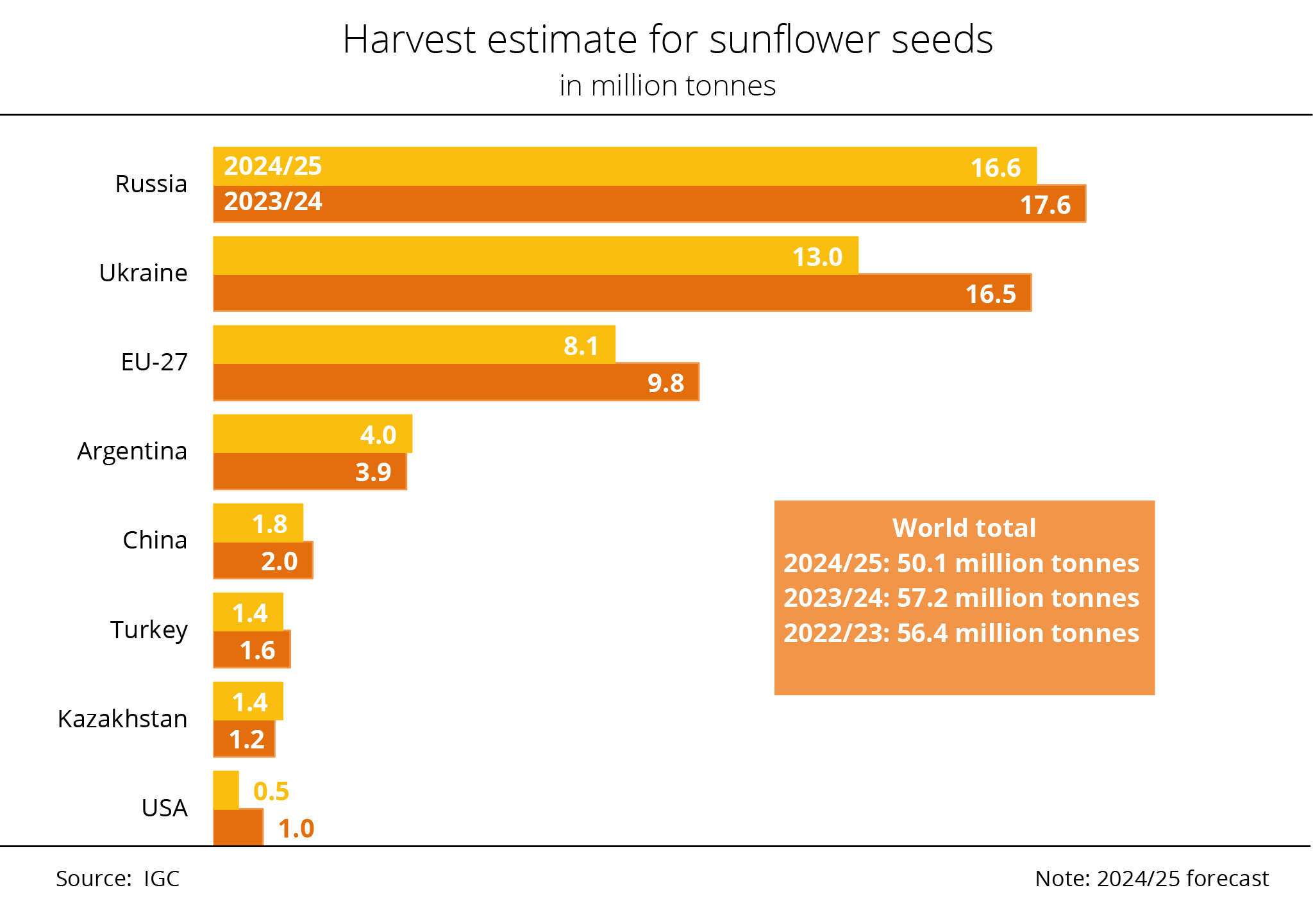

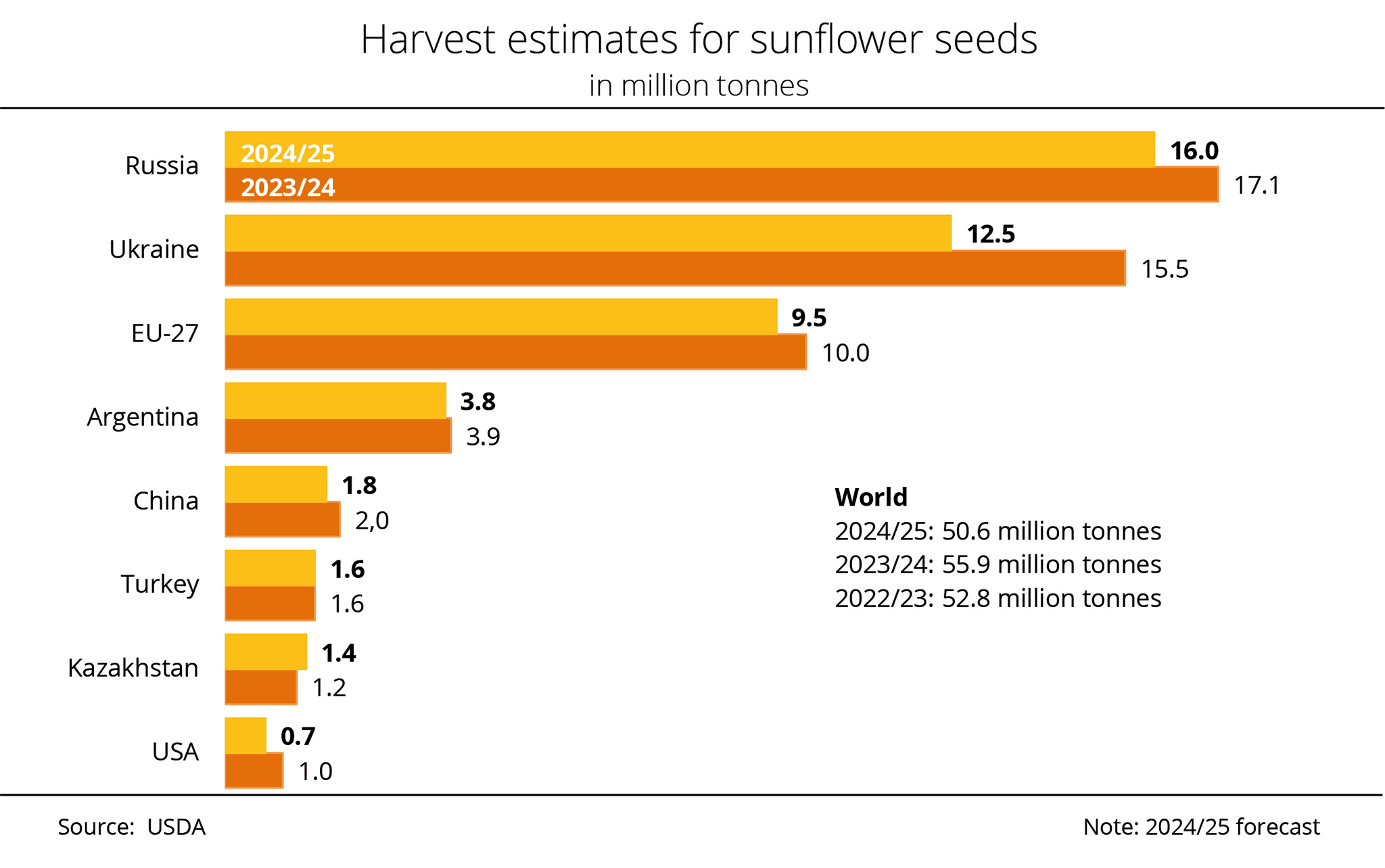

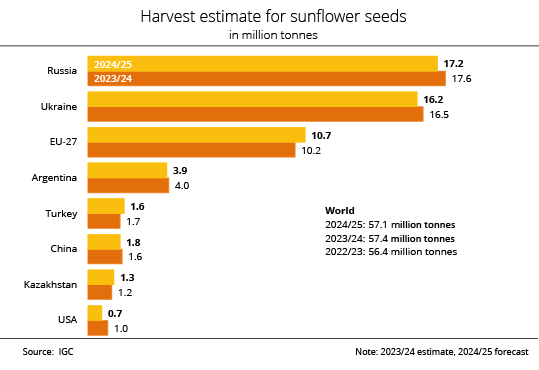

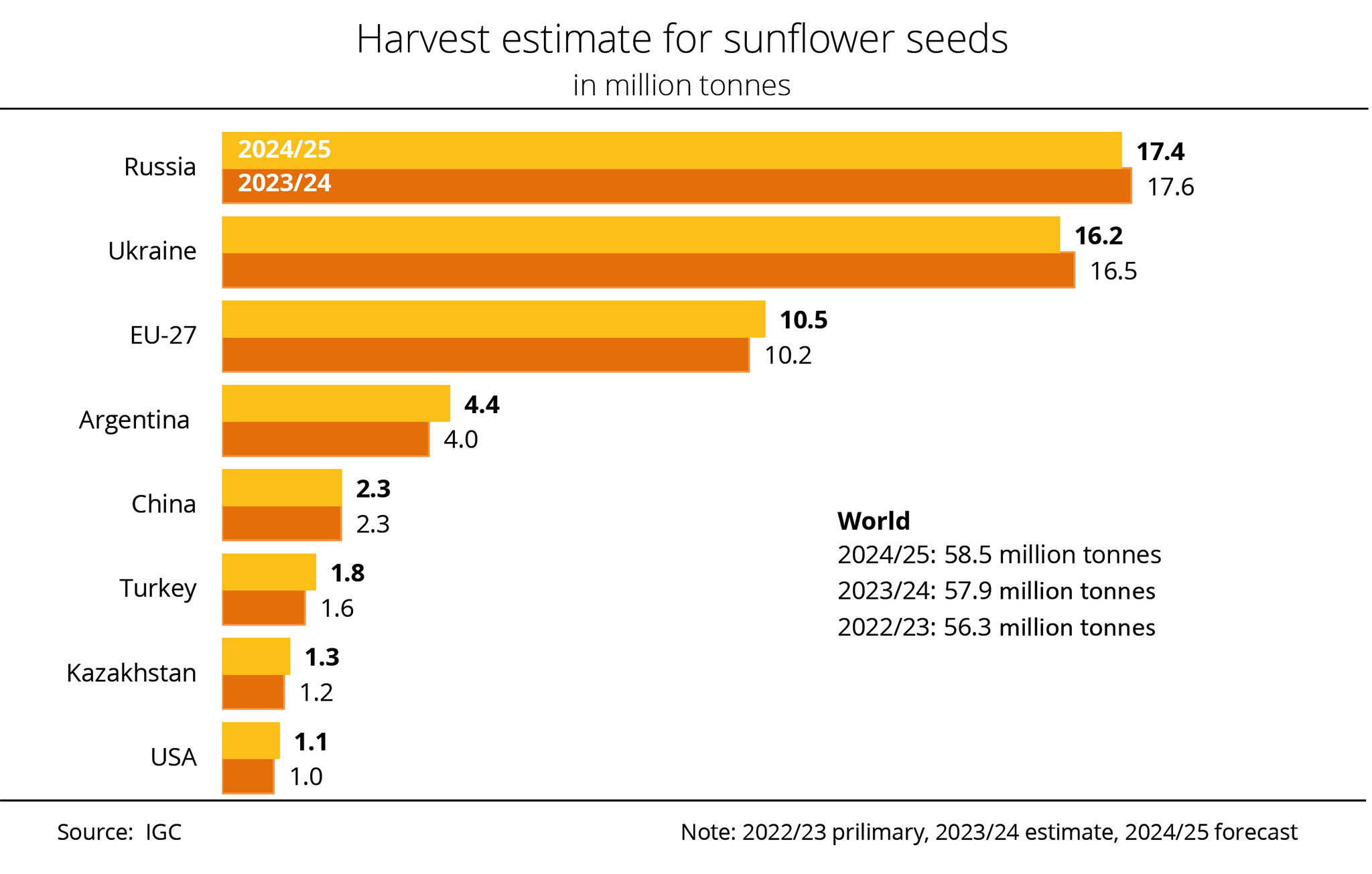

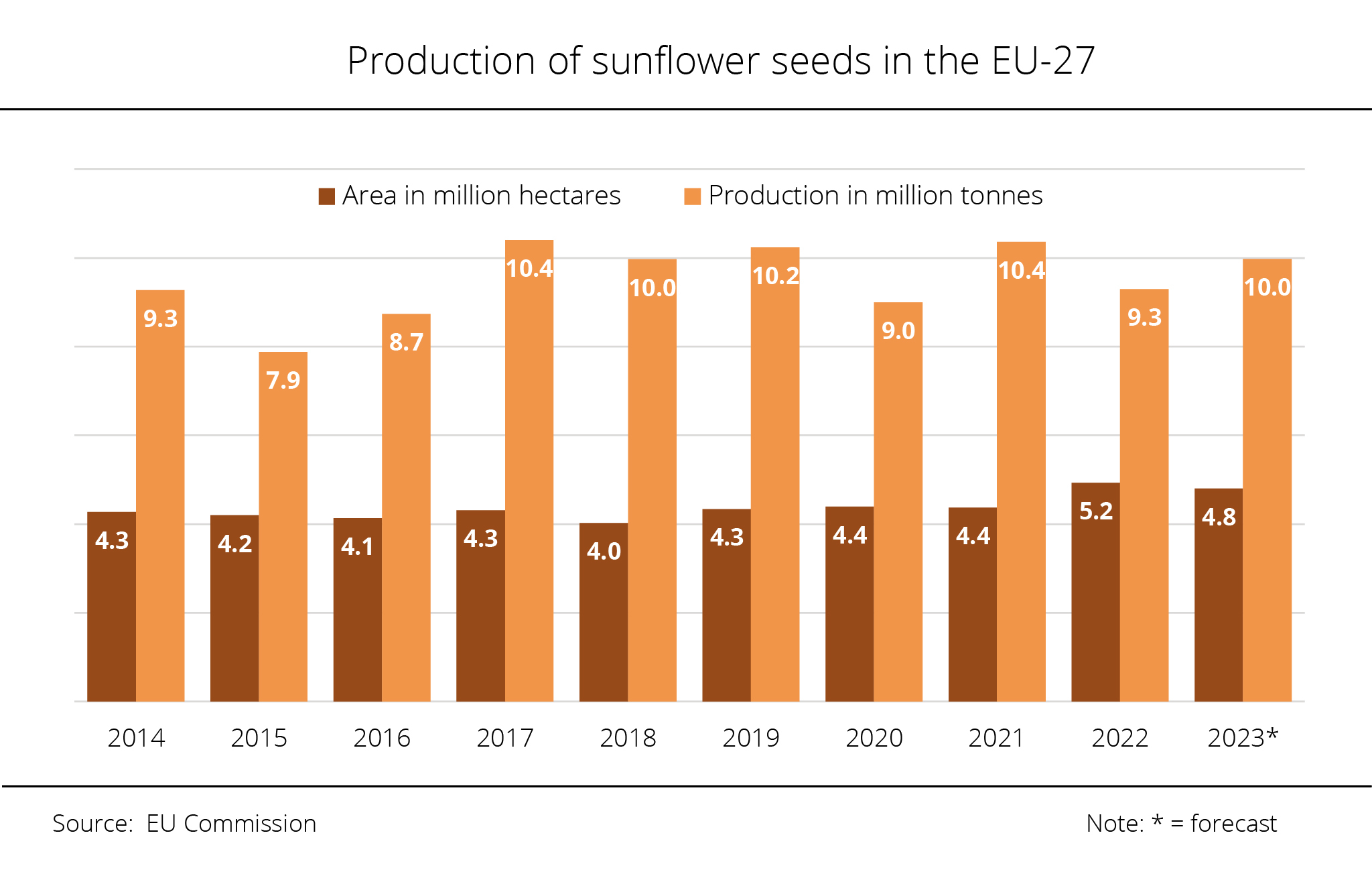

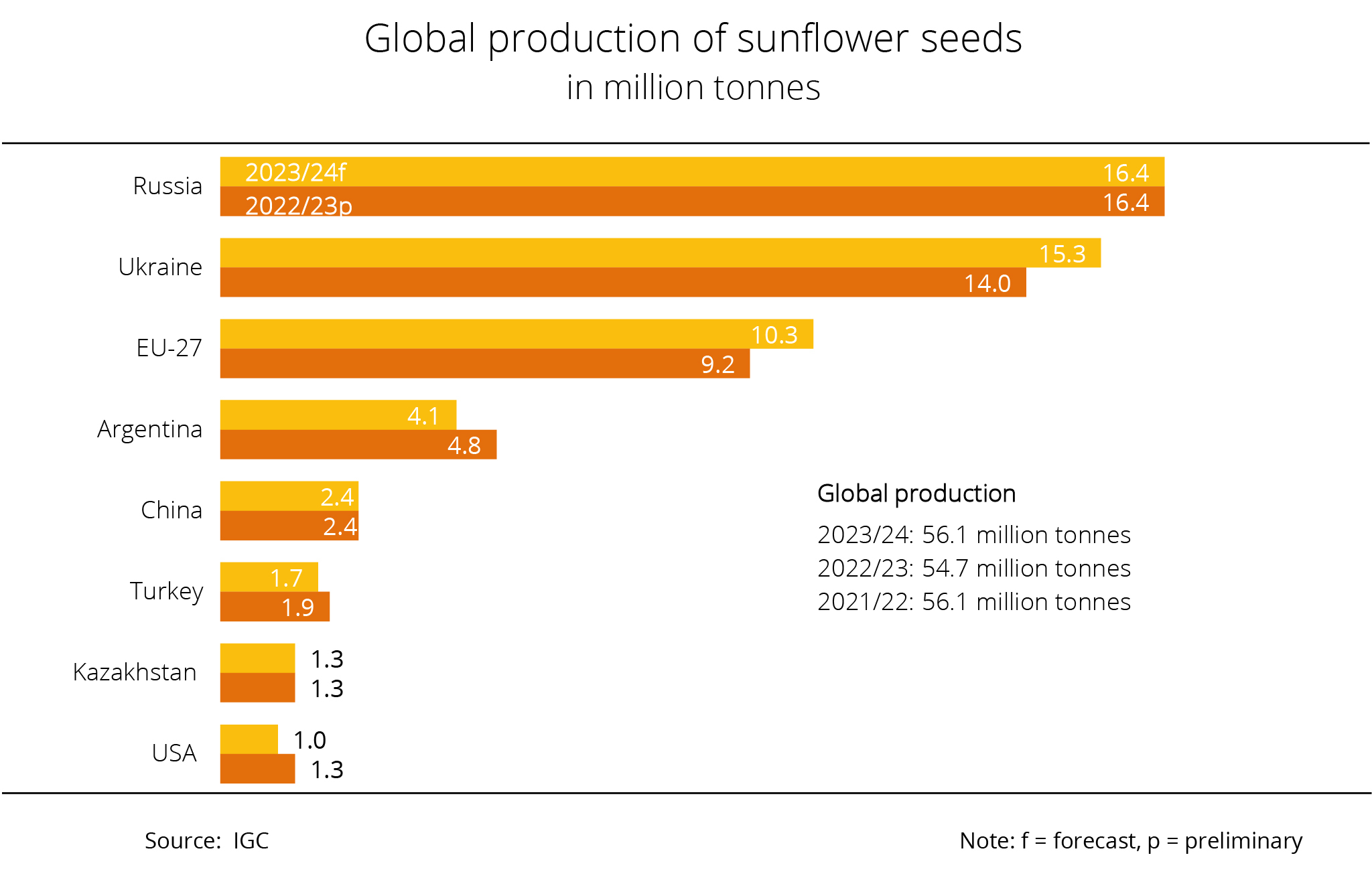

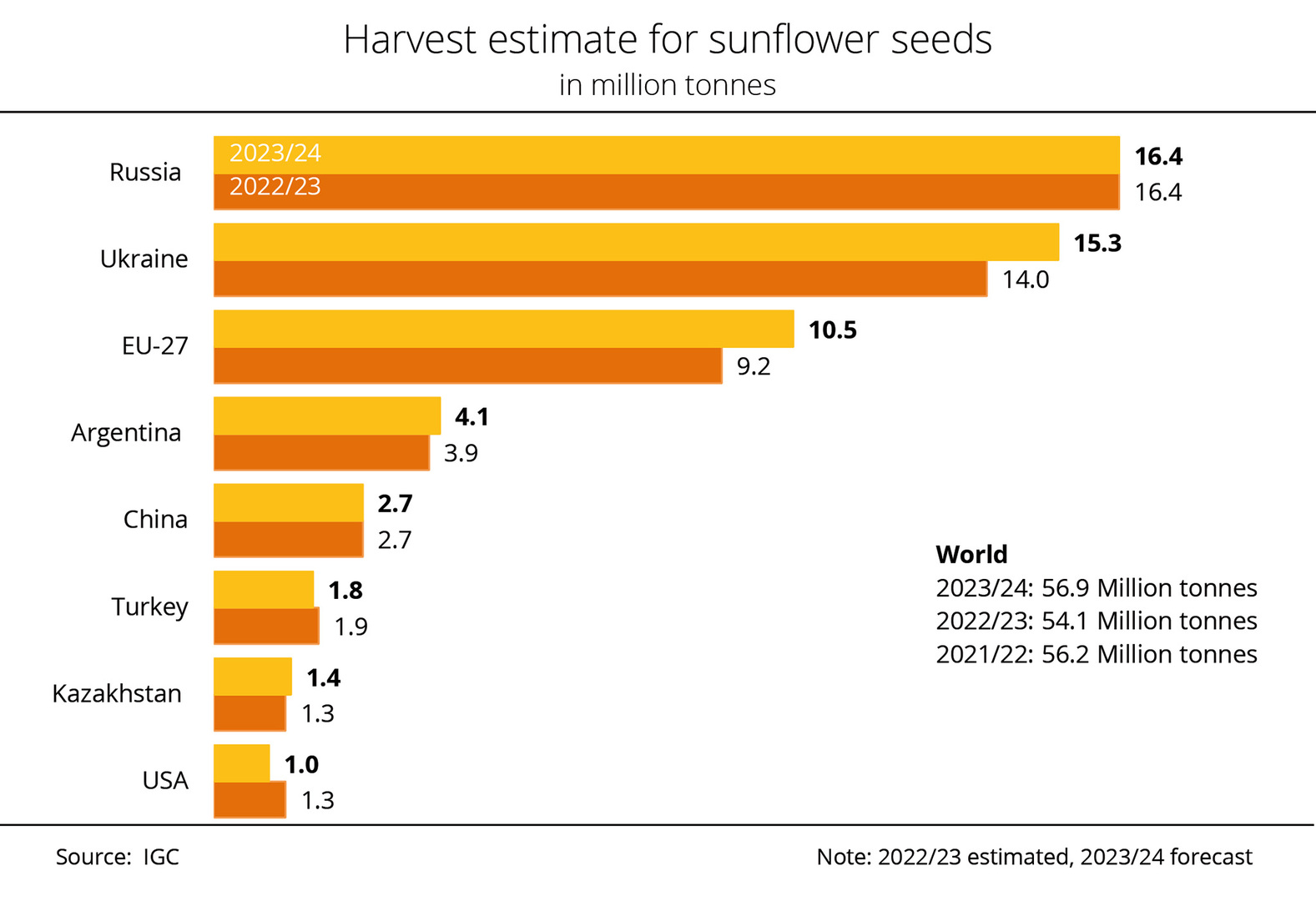

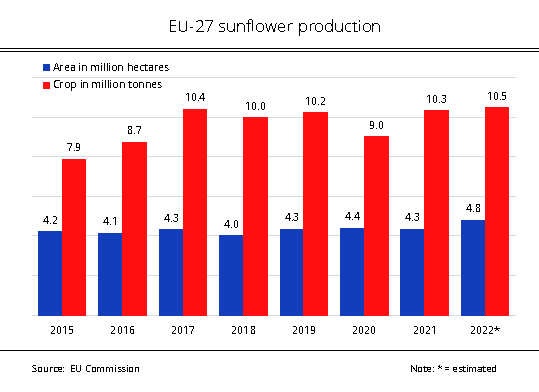

Chart of the week (29 2026): USDA expects sharp increase in sunflower seed production in 2026/27

Berlin, 15 July 2026 – Russia, Ukraine and the EU account for roughly three quarters of global sunflower seed production. In these key regions, 2026/27 harvests are expected to exceed those of the previous year, thereby presumably raising global production to a new record level.

According to the latest data from the US Department of Agriculture (USDA), global sunflower seed production in the 2026/27 season is set to reach around 62.7 million tonnes. This translates to a year-on-year increase of well above 13 per cent, setting a new record. The key factor behind this rise is expected larger harvests in Eastern Europe and the EU. For Russia, which remains the world's largest producer of sunflower seed, the USDA projects approximately an 18 per cent increase over 2025/26, bringing the harvest to 20.7 million tonnes. The same applies to Ukraine. For the EU-27, the USDA currently forecasts a harvest of 9.8 million tonnes, which would be up just over 13 per cent from the previous year's 8.7 million tonnes.

The Argentine harvest is also expected to be higher. According to research by Agrarmarkt Informations-Gesellschaft (mbH), the country is expecting the largest sunflower seed harvest in its history in the 2026/27 crop year. Production increases are also forecast for Kazakhstan, China and Turkey. On the other hand, the harvest in the US will probably fall short of the previous year's level.

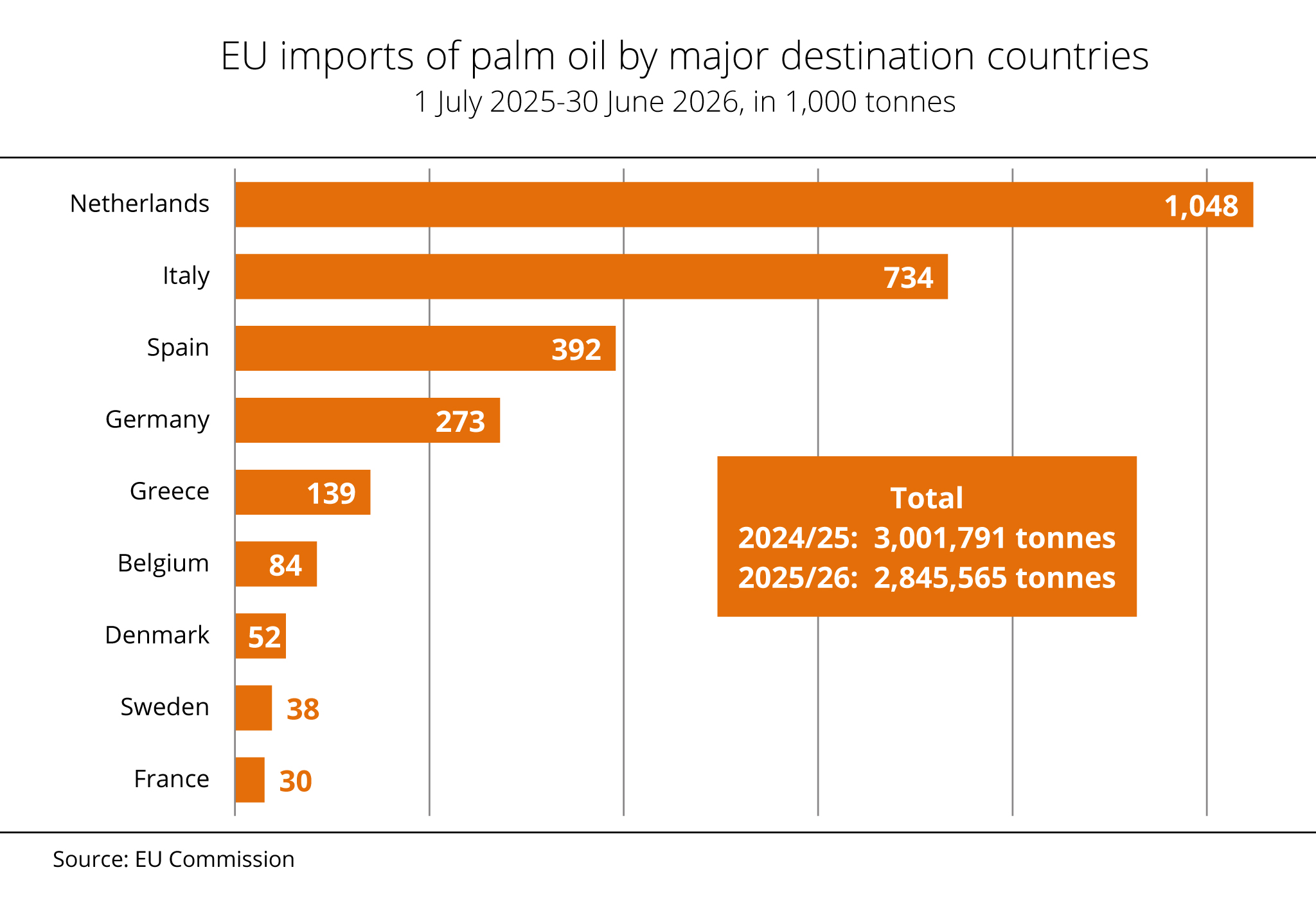

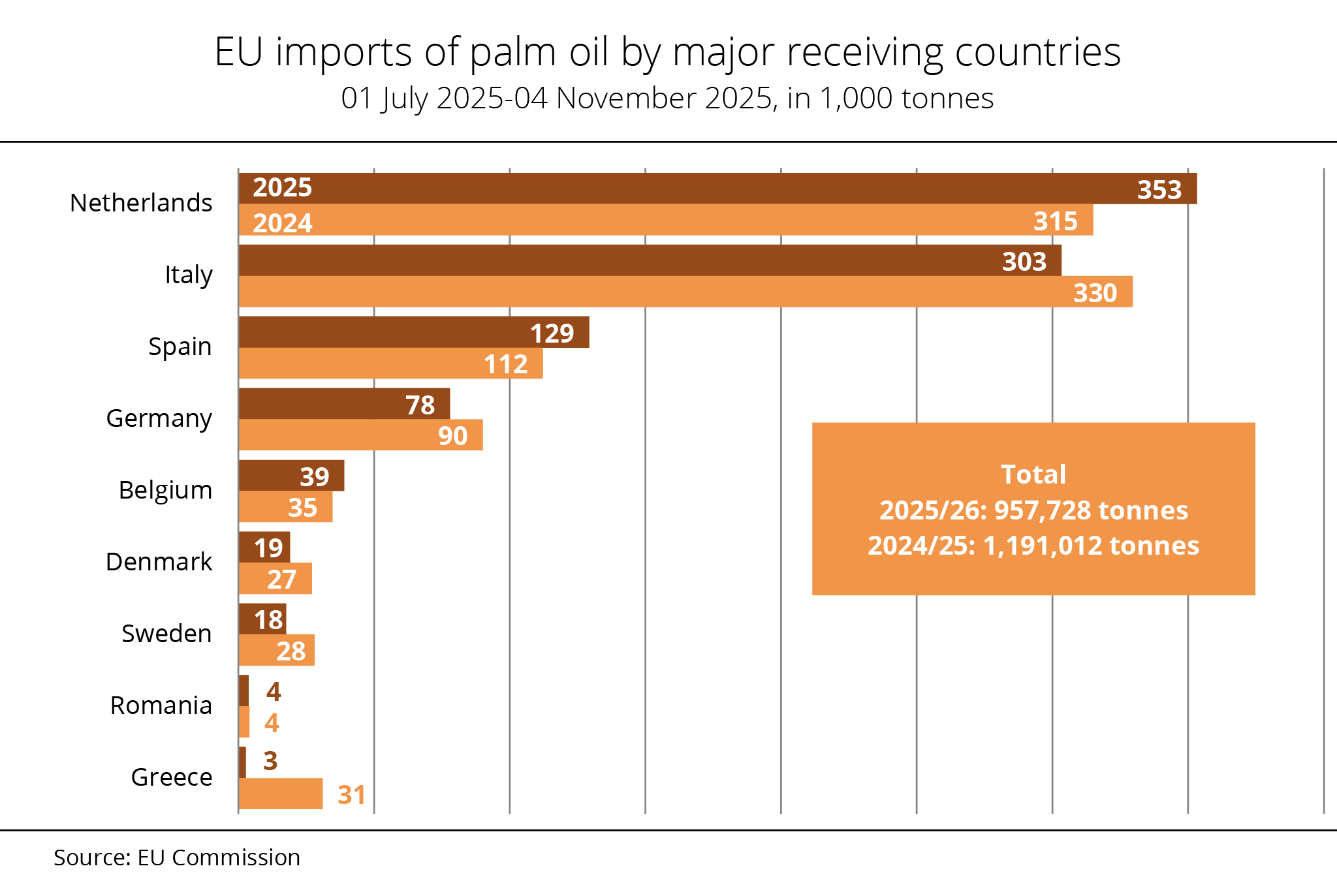

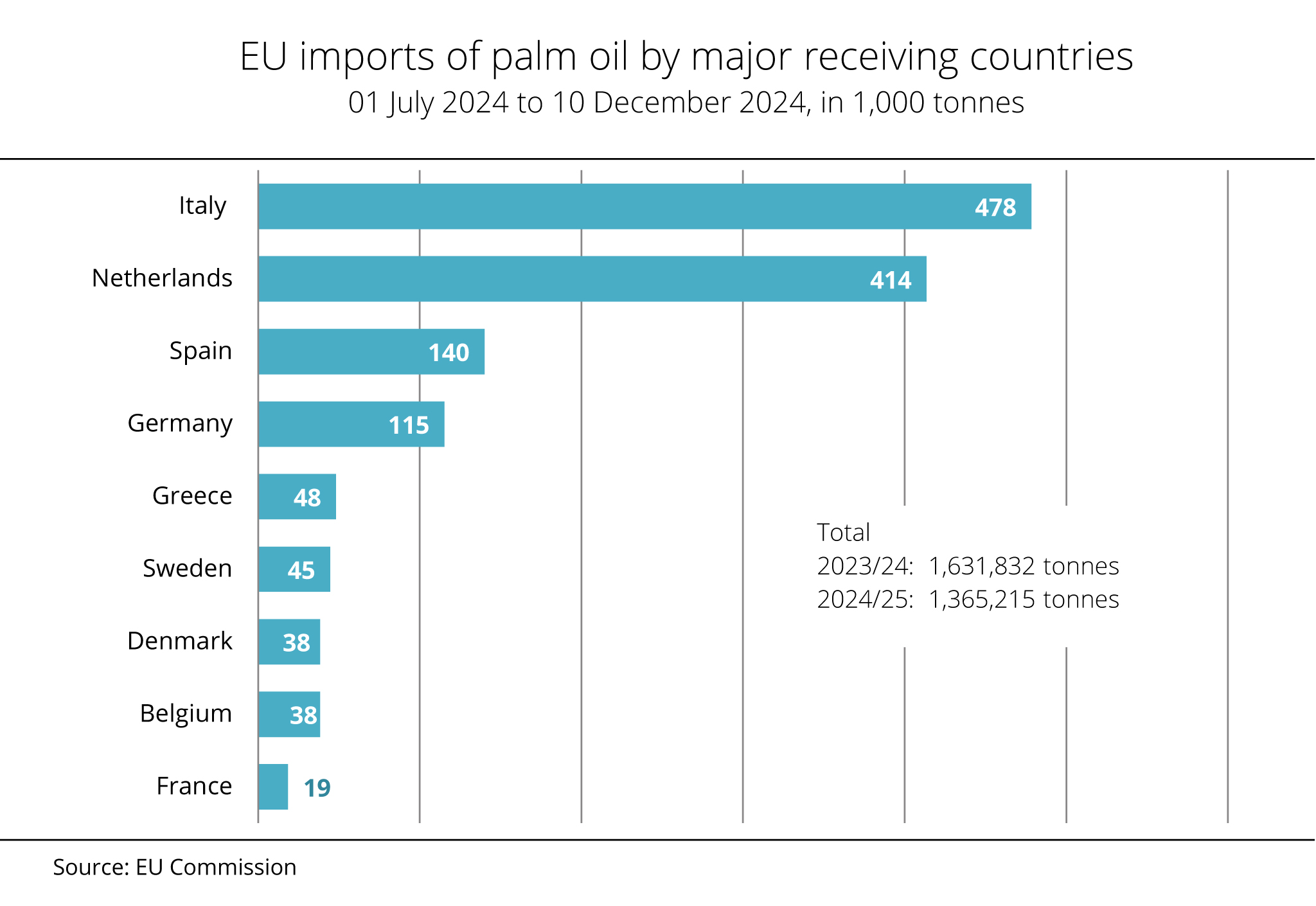

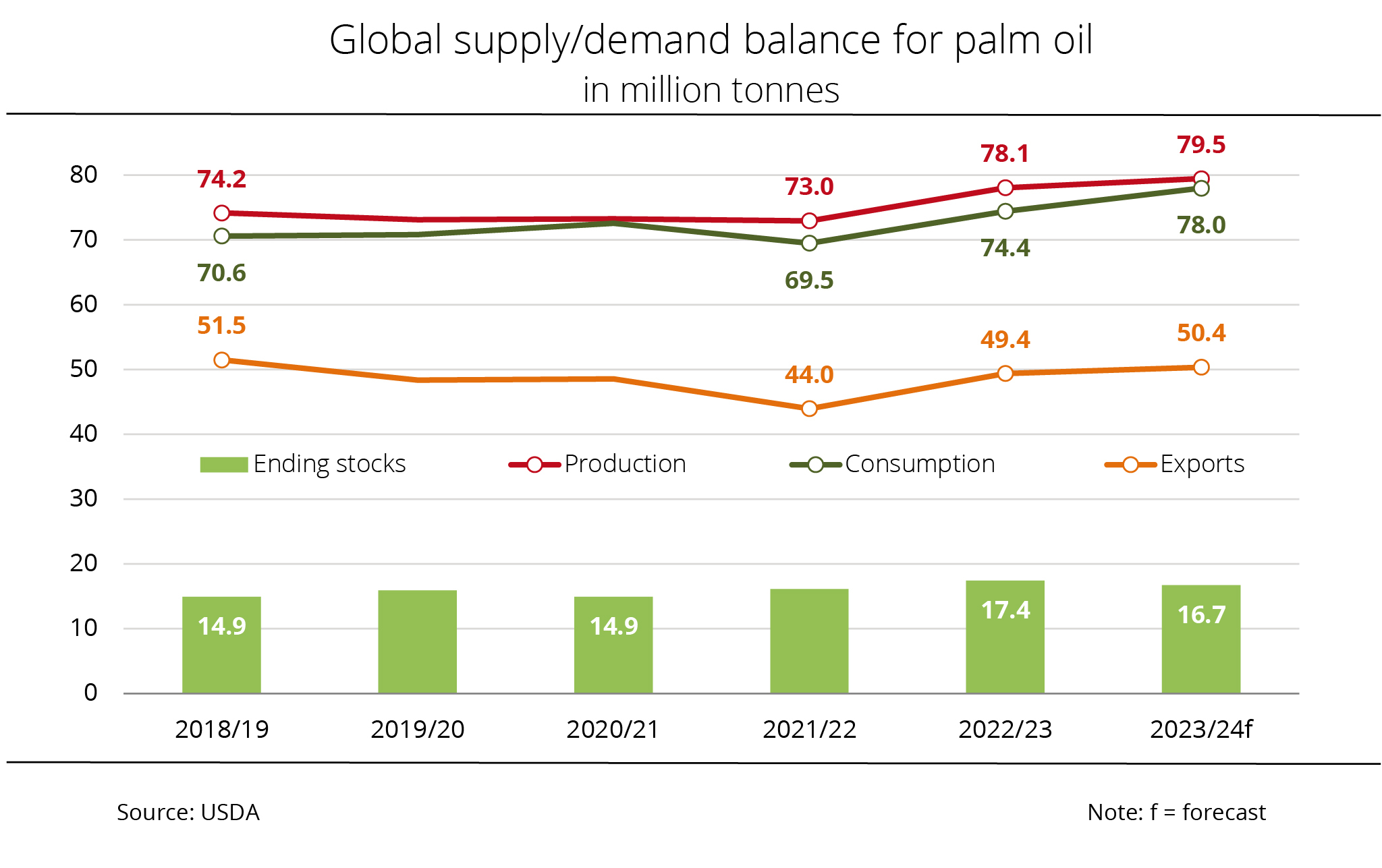

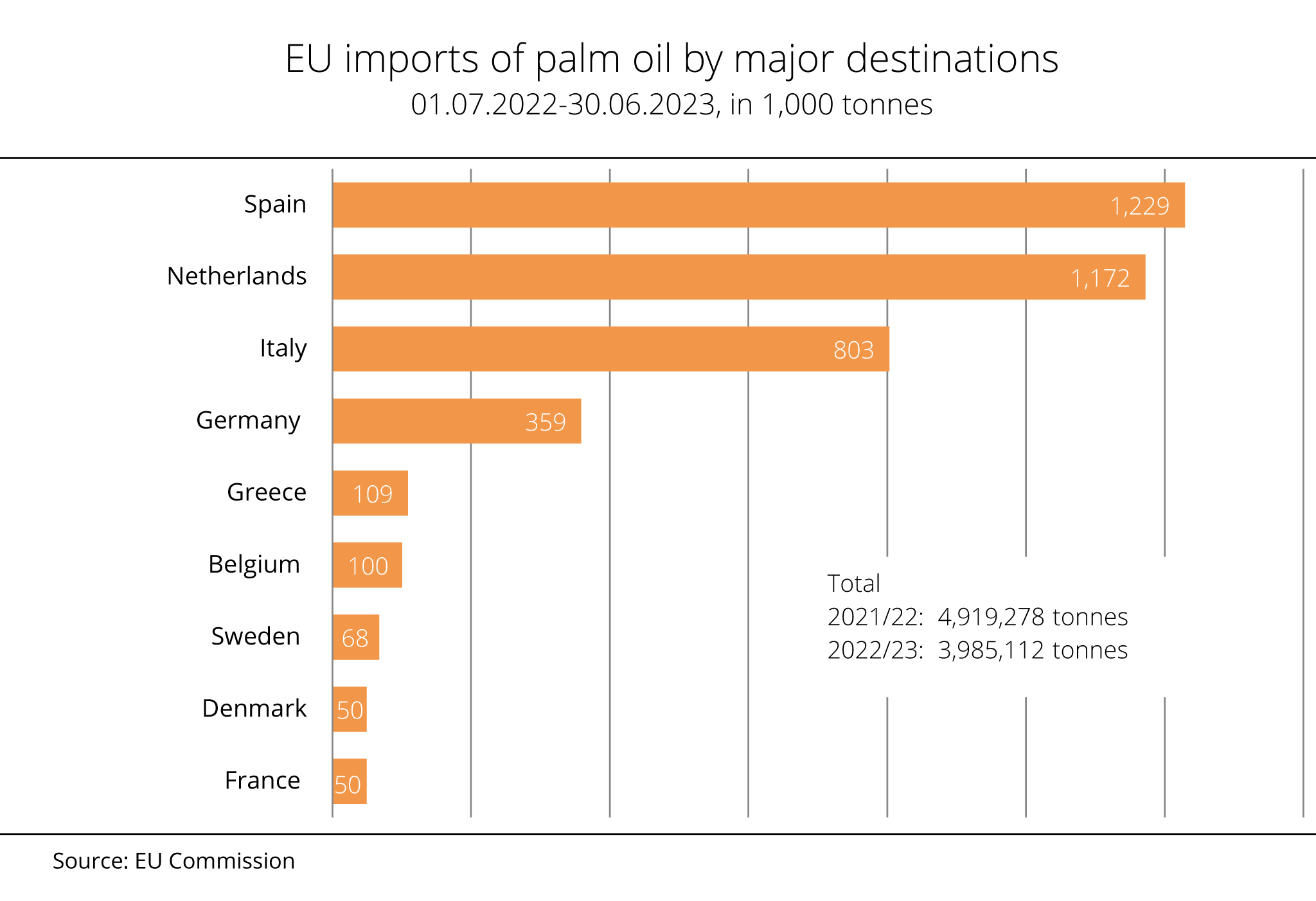

Chart of the week (28 2026): EU palm oil imports declined further

Berlin, 9 July 2026 – EU Member States imported less palm oil in the marketing year 2025/26 than in the previous year. Imports totalled approximately 2.85 million tonnes, representing a decline of just over 5 per cent compared with a year earlier.

Berlin, 9 July 2026 – EU Member States imported less palm oil in the marketing year 2025/26 than in the previous year. Imports totalled approximately 2.85 million tonnes, representing a decline of just over 5 per cent compared with a year earlier.

The Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) attributes this to the EU-wide changes in legal requirements in Member States such as Germany and France, under which palm oil-based biofuels are excluded from counting towards national quota obligations or from receiving tax incentives as a result of the iLUC classification of palm oil. Moreover, according to the Evaluation Report of the Federal Office for Agriculture and Food (BLE), average greenhouse gas savings from palm oil-based biofuels amount to 77.5 per cent, 10.5 percentage points lower than those achieved by biofuels derived from waste oils and fats. This commodity group is displacing palm oil in Germany and the EU. The trend is also reflected in the import volumes of this feedstock category. According to investigations conducted by the Agrarmarkt Informations-Gesellschaft mbH (AMI), imports increased from 3.64 million tonnes in 2023 to 4.60 million tonnes in 2025. The double counting system, which has since been abolished in Germany, for the use of certain waste oils and fats had accelerated the displacement effect.

The Netherlands remains the leading importer within the European Union. At approximately 1.05 million tonnes, the country imported roughly 9 per cent more palm oil than in 2024/25. It should be noted, however, that Dutch ports such as Rotterdam and Amsterdam act as central gateways for overseas imports into the EU. In other words, some of these imports will have been redirected to other Member States. Furthermore, the Netherlands is one of the leading European biofuel production locations.

Italy ranks as the second largest importer of palm oil, receiving nearly 734,000 tonnes, which represents a 12 per cent decline from the previous year. In contrast, Spain raised its imports significantly, by 35 per cent, to approximately 392,000 tonnes. Germany increased its imports 20 per cent to roughly 273,000 tonnes. UFOP attributes this rise to growing demand from the food and chemical industries, with the feedstuff industry also representing a major market for palm oil. Greece and France also recorded increases. In contrast, demand in Denmark and Sweden fell sharply. While Denmark decreased its palm oil imports 38 per cent to roughly 52,000 tonnes, Swedish imports virtually halved, reaching just under 38,000 tonnes.

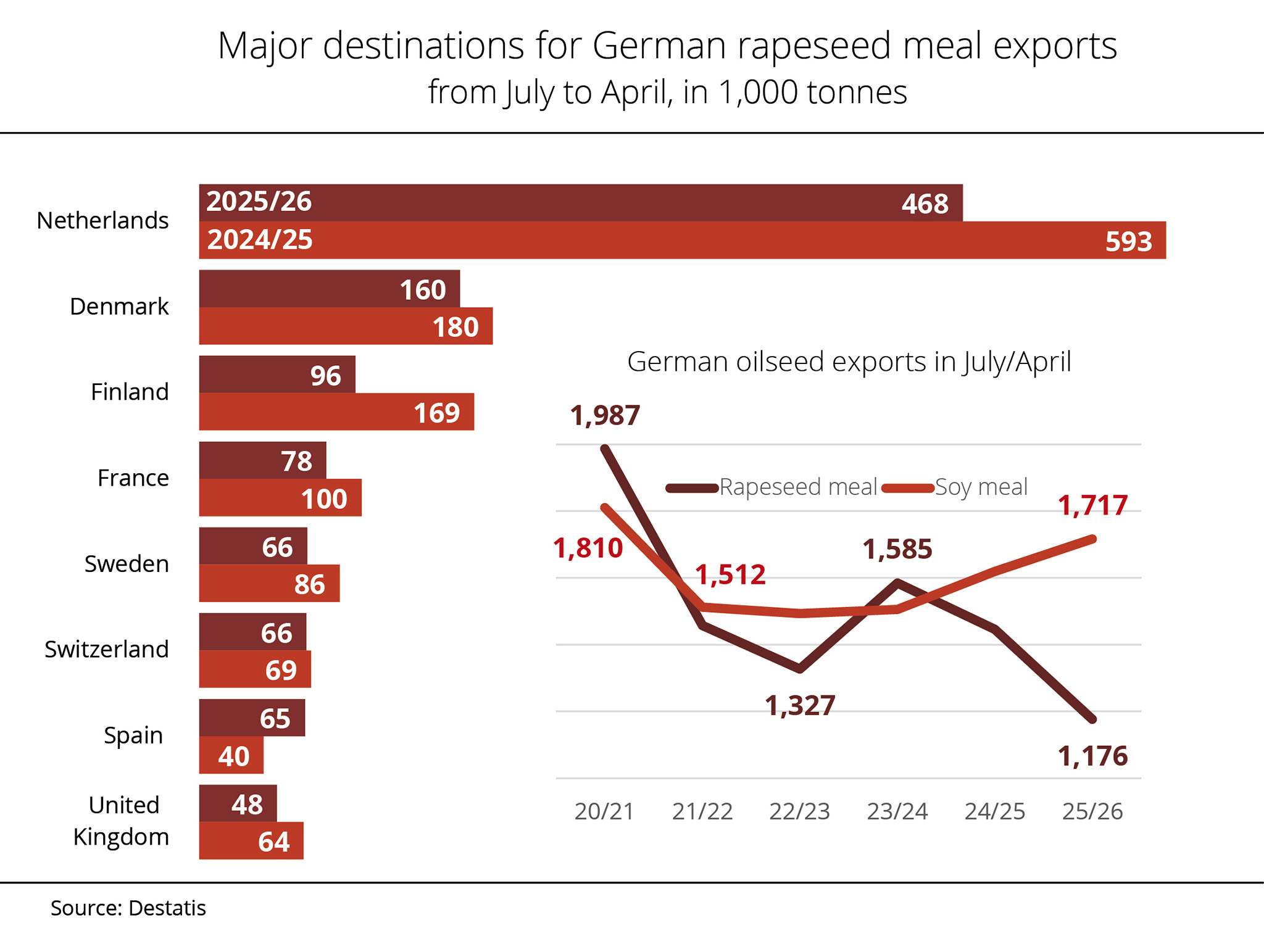

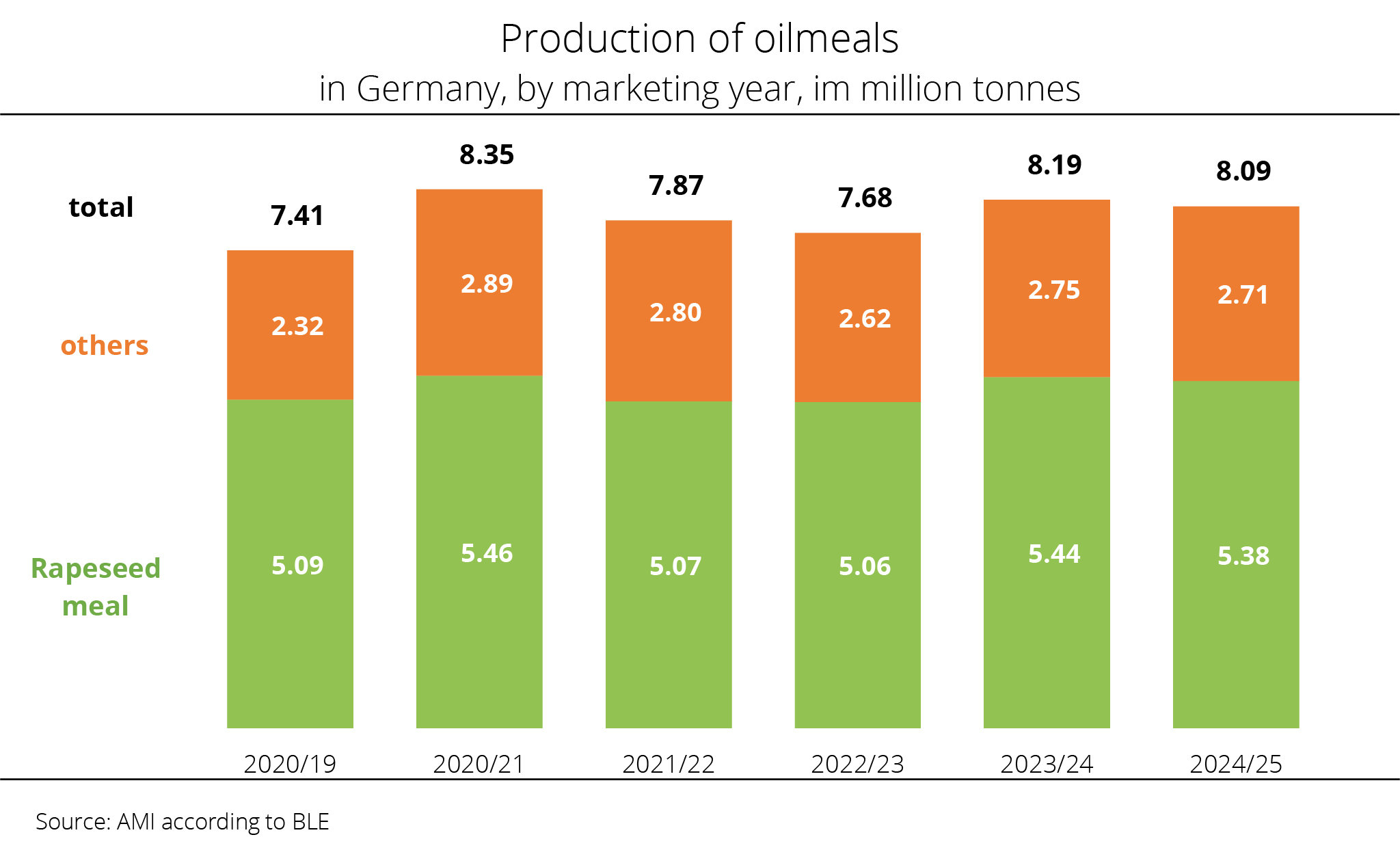

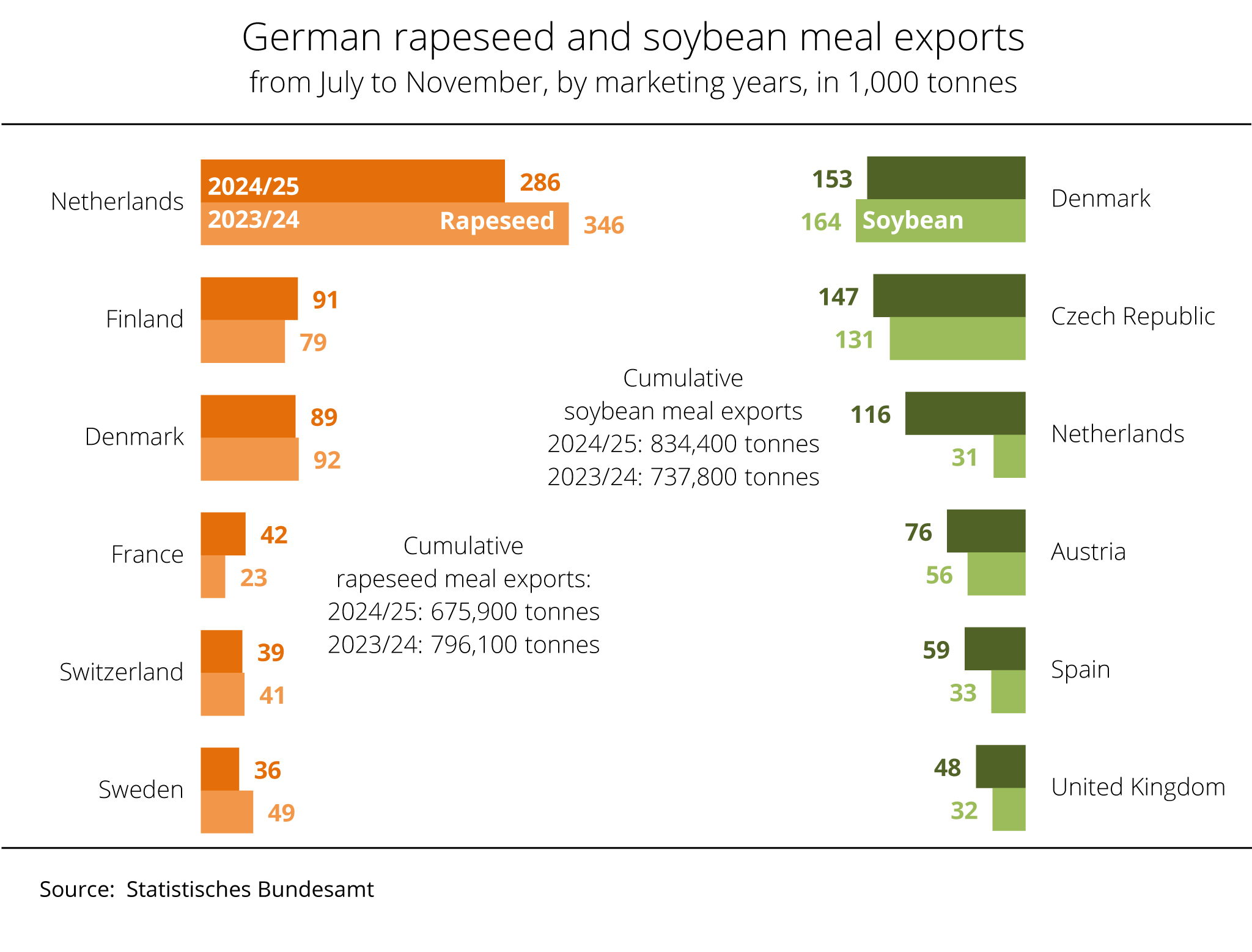

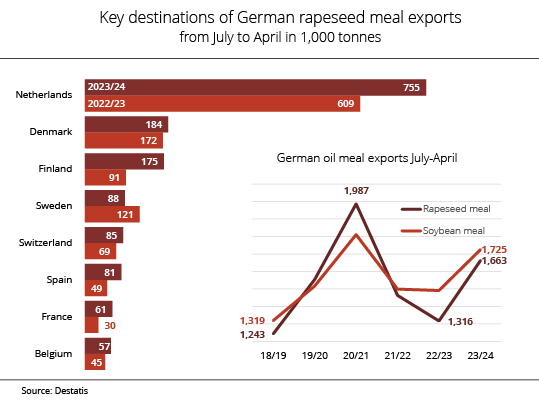

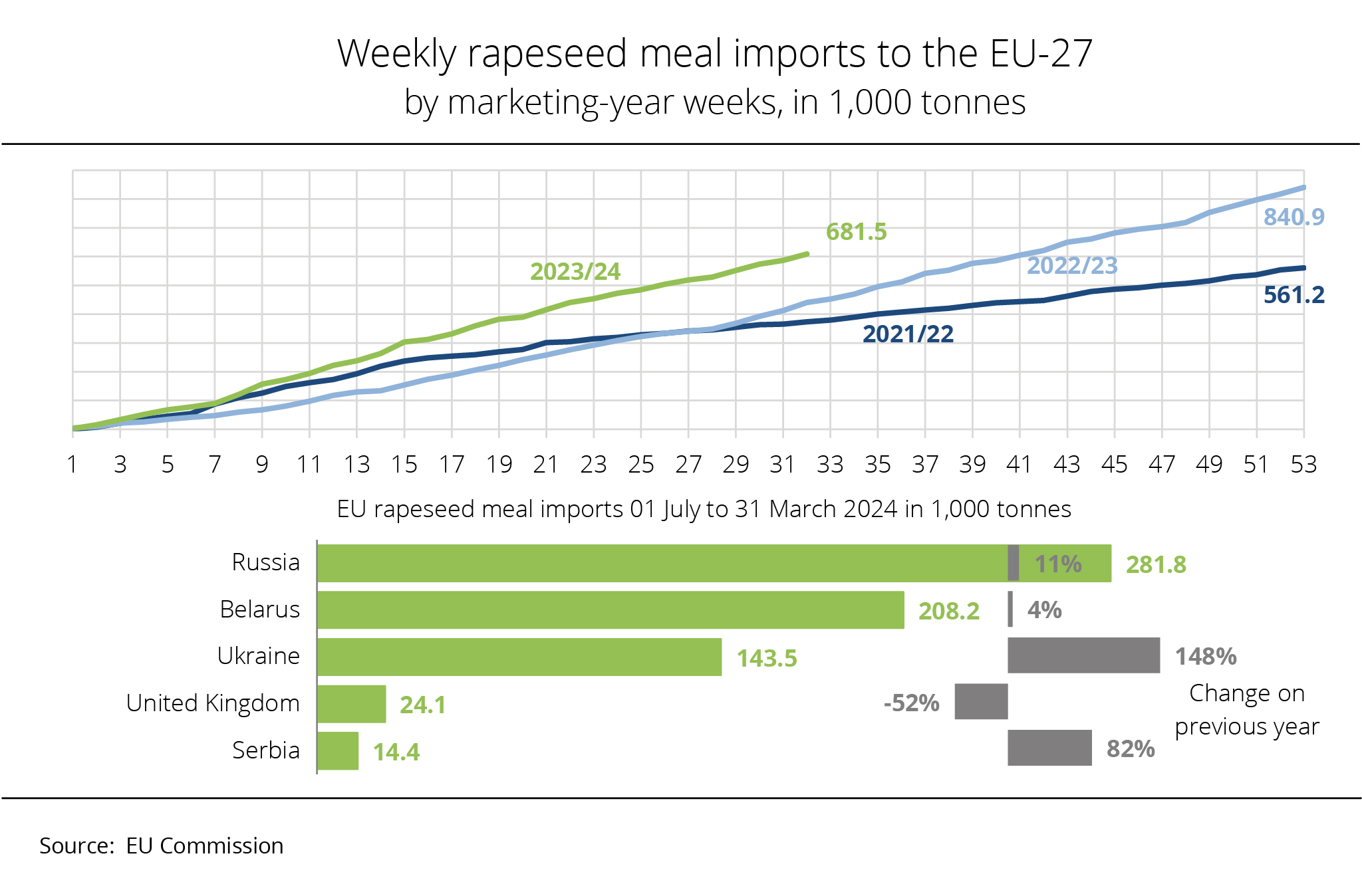

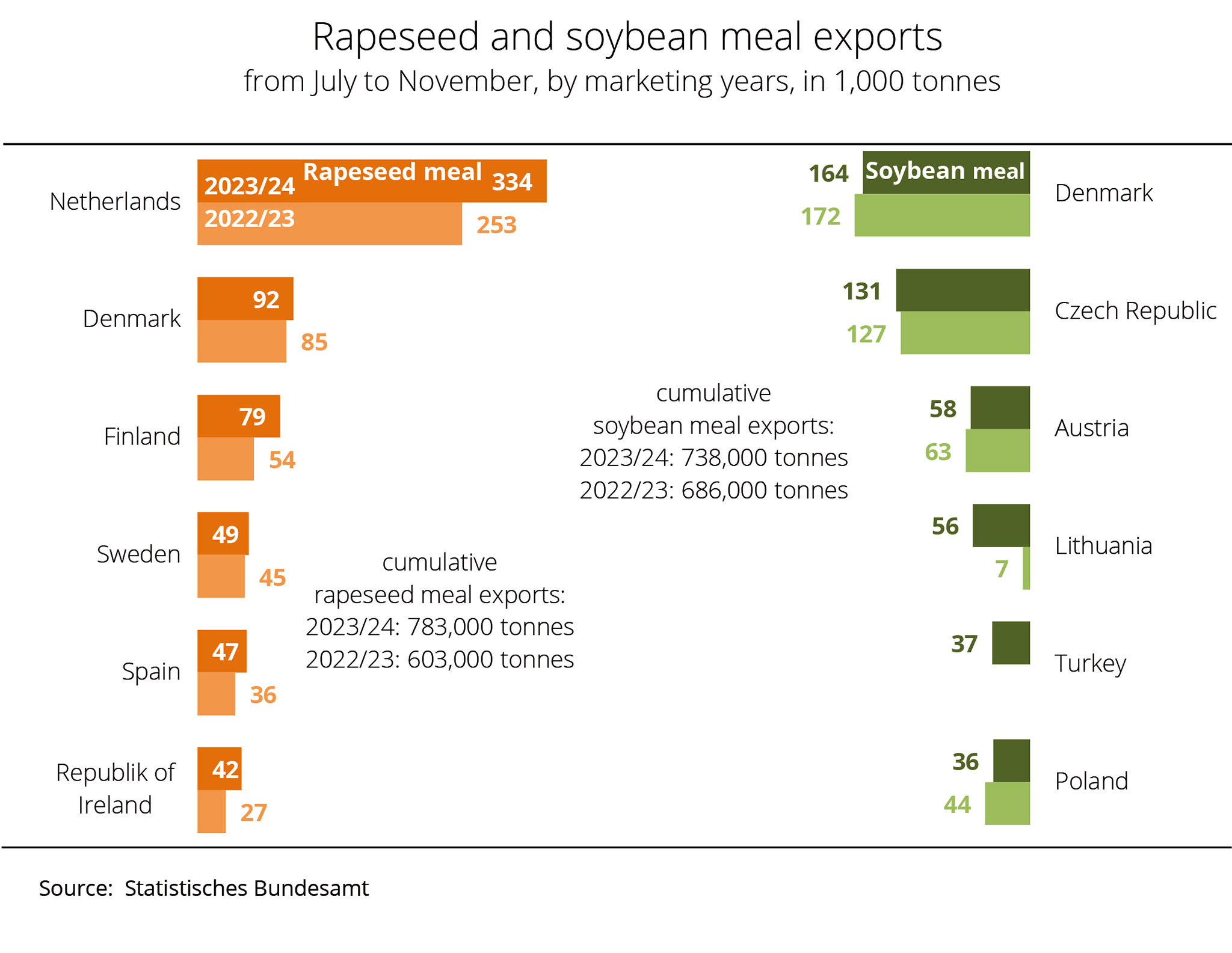

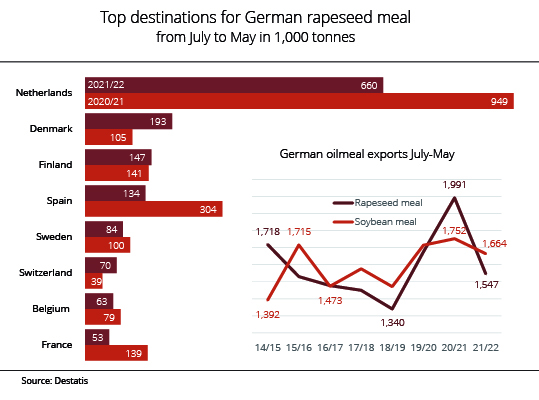

Chart of the week (27 2026): German rapeseed meal exports well below the previous year’s level

Berlin, 1 July 2026 – German exports of rapeseed meal declined noticeably in the current crop year 2025/26 compared with the previous year. Above all, shipments to key EU destination countries dropped significantly.

Berlin, 1 July 2026 – German exports of rapeseed meal declined noticeably in the current crop year 2025/26 compared with the previous year. Above all, shipments to key EU destination countries dropped significantly.

According to data from the German Federal Statistical Office, Germany exported nearly 1.2 million tonnes of rapeseed meal from July 2025 to April 2026, representing a decline of approximately 19 per cent from the year-earlier period. The Netherlands remained the most important market, taking 468,000 tonnes, although this was down 21 per cent year on year. Exports to Denmark decreased 11 per cent, reaching just over 160,000 tonnes. Shipments to Finland fell particularly sharply, declining 43 per cent to 96,000 tonnes.

Outside the EU, Switzerland remained a major market, with exports totalling just under 66,000 tonnes, down 4 per cent. Deliveries to the UK also declined considerably, falling 26 per cent to nearly 48,000 tonnes. Individual markets such as Spain (up 64 per cent to approximately 65,000 tonnes) recorded increases, however, these were not sufficient to offset the declines in the key markets.

According to research by Agrarmarkt Informations-Gesellschaft mbH, export growth was constrained by a more limited supply of rapeseed meal, stable domestic demand, and increasing competition from alternative protein sources such as soya meal, which narrowed the scope for exports in the current crop year.

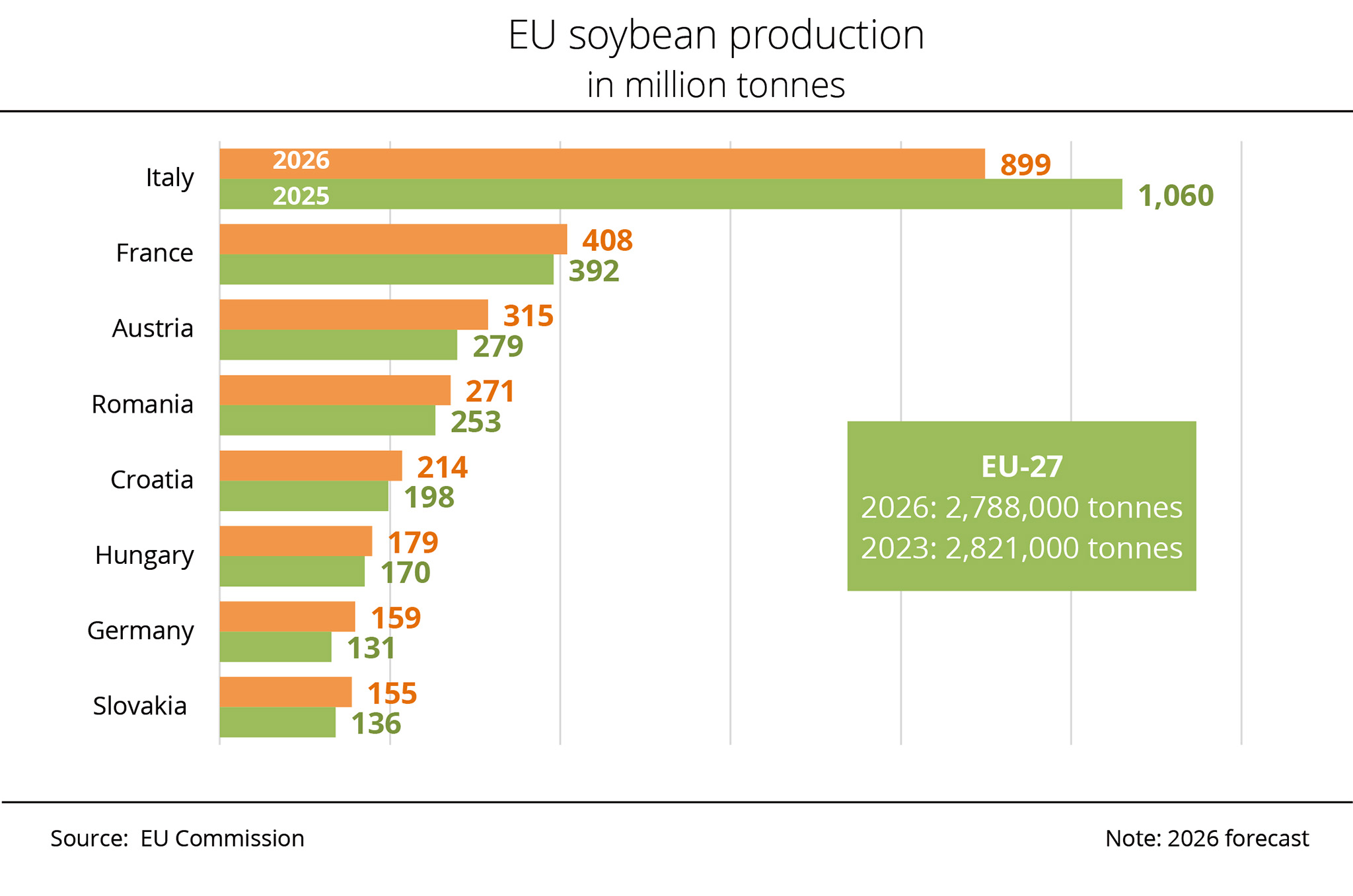

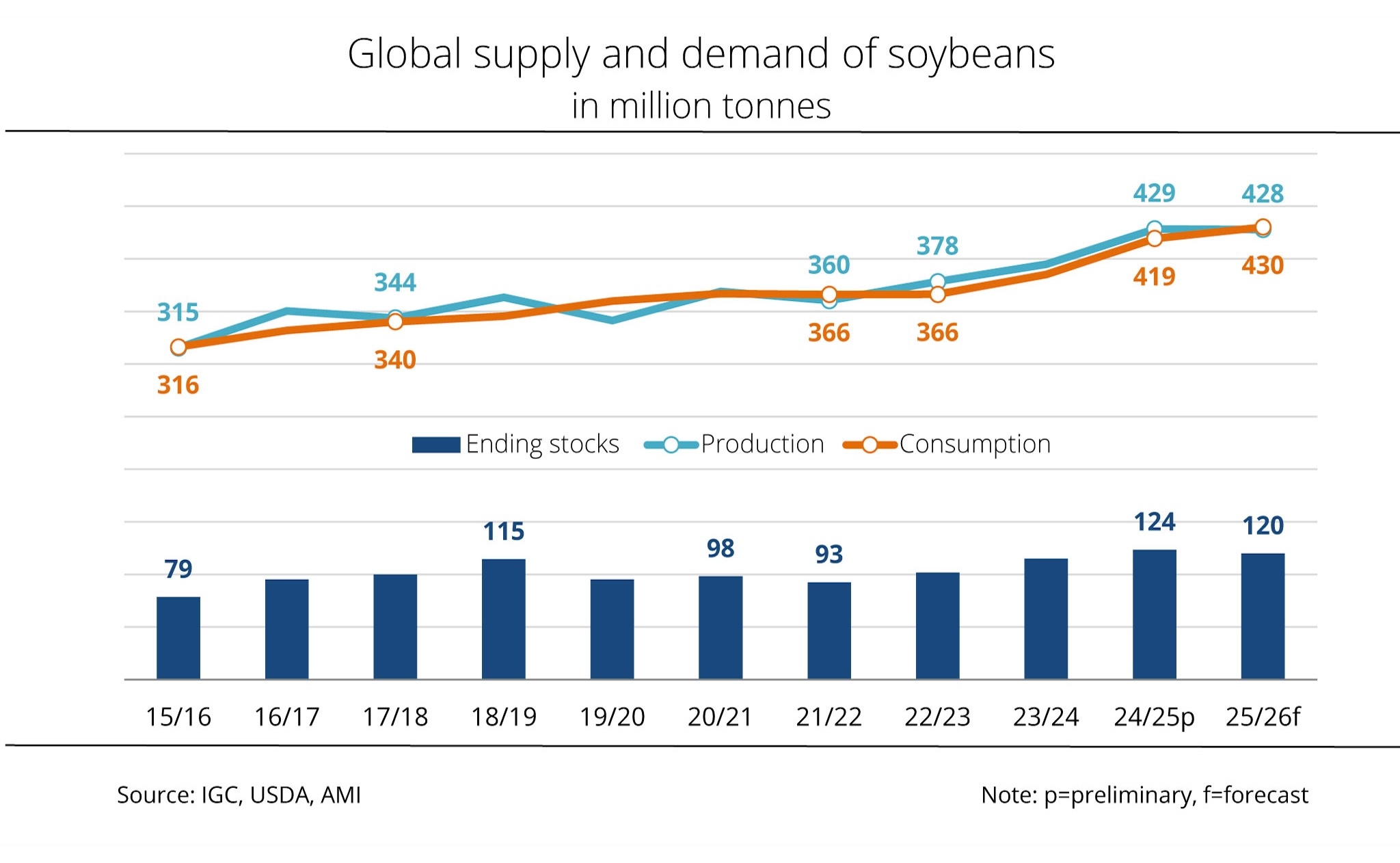

Chart of the week (26 2026): Soybean production 2026 – Germany's output set to hit record level

Berlin, 24 June 2026 – According to an estimate by the EU Commission, soy supply in the EU‑27 in the 2026/27 marketing season is set to fall below the previous year's level. The main reason for the lower output is a significant reduction in Italian production. On the other hand, Germany's harvest is set to reach a record level. However, according to the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP), there is still considerable potential for growth.

The association holds that EU soybean farming is generally on the upswing, pointing out that EU Commission information indicates that EU soybean production has tripled over the past decade, although output is set to decline in 2026 for the second year running. UFOP places reliance on the funding opportunities provided by the announced national and European protein plans. Given the desolate situation in the grain and sugar markets, demand-driven diversification of crop rotation is the order of the day, UFOP has stated.

According to UFOP, the EU Commission's Directorate-General for Energy's plan to classify soybeans globally as a high-iLUC feedstock will have counterproductive effects on the desired expansion of European soybean production. The association has called upon both the Council and the Parliament to stop the draft delegated regulation. Encouragingly, this week a majority of the members of the European Parliament’s ITRE Committee (Committee on Industry, Research, and Energy) voted in favour of a motion put forward by the EPP, ECR, and Renew political groups, recommending that the European Parliament block the European Commission’s planned classification of soy. According to UFOP, it is now up to the Parliament's plenary assembly to follow this recommendation.

For the current crop year, soybean production is expected to reach just under 2.8 million tonnes, representing a decline of around 1 per cent compared with 2025. According to investigations conducted by Agrarmarkt Informations‑Gesellschaft mbH, the main reason for the slight reduction in soybean supply in the EU-27 is lower yield expectations.

Italy is expected to remain the largest producer in the EU, with output projected at 899,000 tonnes, representing a decrease of about 15 per cent year-on-year. In other words, the Italian soybean harvest would reach the lowest level in five years. In contrast, the Commission expects France, the second largest EU supplier of soybeans, to record a 4 per cent increase to 408,000 tonnes. Other Member States are also expected to see increases in soybean production compared with the previous year.

Soybean production in Germany is expected to be especially dynamic. The EU Commission expects an increase of just over 21 per cent compared with 2025, reaching 159,000 tonnes. This means that the harvest will probably reach the highest level ever. In other words, despite the limited absolute volume compared with other EU Member States, Germany is gaining importance. The expansion of soybean cultivation areas and output underlines Germany's role as a growing market, supported by rising demand for domestic protein sources.

Chart of the week (25 2026)

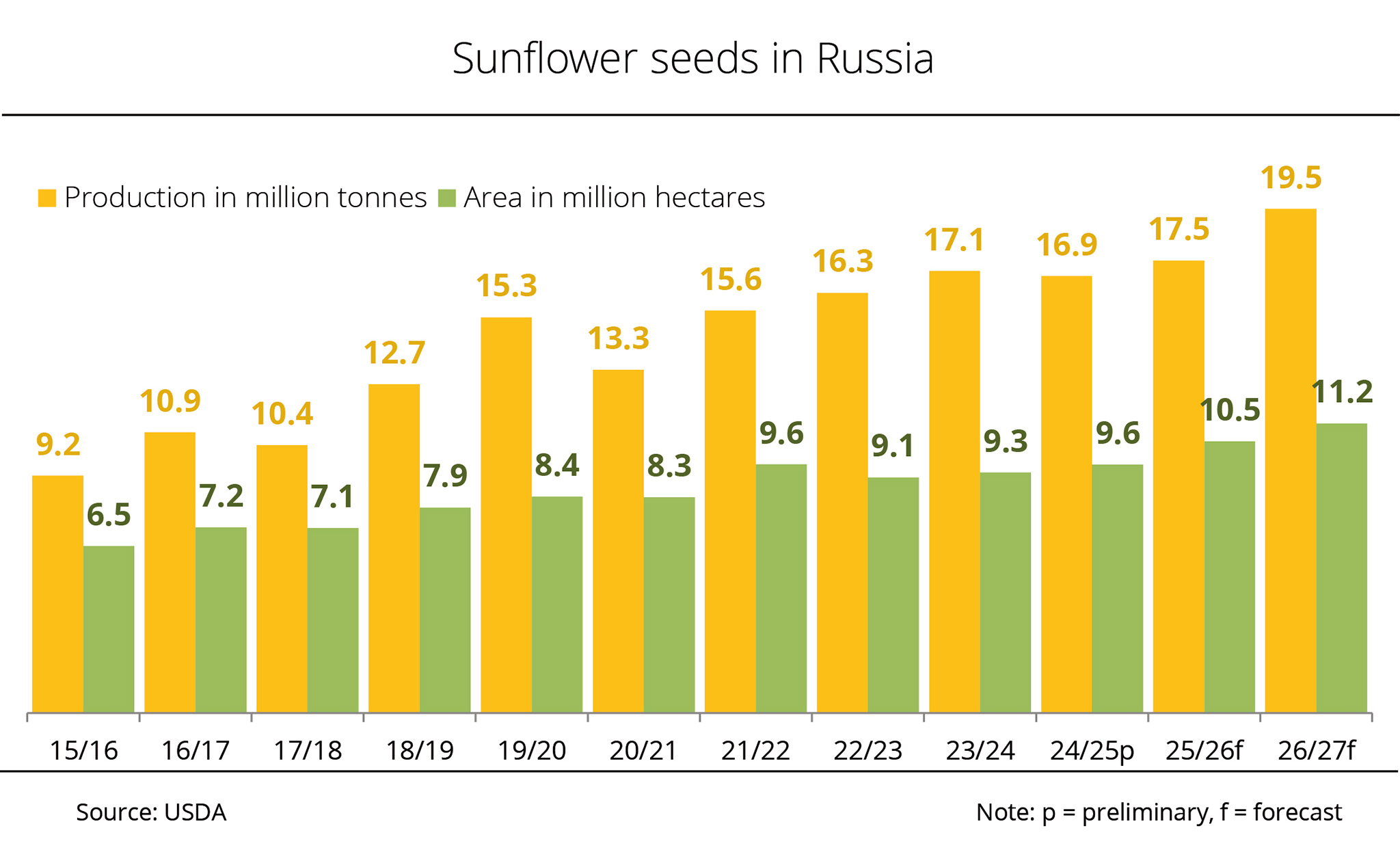

Record year for Russia's sunflower seed production

Berlin, 17 June 2026 – Russia is the world's largest producer of sunflower seed. The harvest is expected to reach a new record high in the coming season due to a significant expansion in crop area and a slight increase in yields.

Berlin, 17 June 2026 – Russia is the world's largest producer of sunflower seed. The harvest is expected to reach a new record high in the coming season due to a significant expansion in crop area and a slight increase in yields.

The US Department of Agriculture (USDA) has recently presented its June estimate for global oilseed production. The estimate indicates that Russian sunflower seed output in the upcoming crop year will reach 19.5 million tonnes. This would represent an increase of roughly 11 per cent compared with the current season and would mark a new record crop.

The key factor behind this increase is an expansion in sunflower area, with acreage expected to rise around 7 per cent year-on-year, reaching 11.2 million hectares. In addition, yields are projected to increase to 17.4 decitonnes per hectare, exceeding the previous year's level of 16.7 decitonnes per hectare.

According to research by Agrarmarkt Informations‑Gesellschaft mbH, this means that Russia remains the world's leading producer of sunflower seed, ahead of Ukraine and the EU-27.

Chart of the week (24 2026)

Primary use determines iLUC assessment of soya and rapeseed

According to the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP), the debate over indirect land use change (iLUC) requires a differentiated and appropriate understanding of the factors that determine producer prices. Whereas in the case of rapeseed, trends in the vegetable oil markets influence the pricing process and, consequently, farmers' crop-choice decisions, the 80 per cent protein content is the key factor in the pricing and cultivation of soybeans. UFOP has therefore reiterated its criticism of the proposed classification of soybeans as a high-iLUC feedstock when soybean oil is used for biofuel production and such biofuel is counted towards the quota obligations in EU Member States.

According to the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP), the debate over indirect land use change (iLUC) requires a differentiated and appropriate understanding of the factors that determine producer prices. Whereas in the case of rapeseed, trends in the vegetable oil markets influence the pricing process and, consequently, farmers' crop-choice decisions, the 80 per cent protein content is the key factor in the pricing and cultivation of soybeans. UFOP has therefore reiterated its criticism of the proposed classification of soybeans as a high-iLUC feedstock when soybean oil is used for biofuel production and such biofuel is counted towards the quota obligations in EU Member States.

The association has called on the EU agricultural ministers and the European Parliament to stop the European Commission's draft to classify soybeans as a high-iLUC feedstock, allowing for a proper methodological review to be carried out. According to UFOP, it would be absurd if the planned classification of soybean oil were to undermine the European and German protein plans. Soybeans, peas and broad beans are the most important large-grained pulses in the EU and are gaining more and more importance as GM-free sources of protein, helping to extend crop rotations and contributing to security of supply.

UFOP has pointed out that, against this background, it should be recognised that additional demand from the energy sector for soybean oil would make a significant contribution toachieving these objectives. This utilisation option should therefore not be blocked. An expansion of soybean production in the EU is both desirable and necessary. UFOP has stated that, in contrast, the protection of primeval forests and biotopes in South America should be implemented on a polluter-pays basis. This aspect does not appear to have been adequately addressed during the Mercosur negotiations.

Chart of the week (23 2026)

Increase in grain legume area in Germany

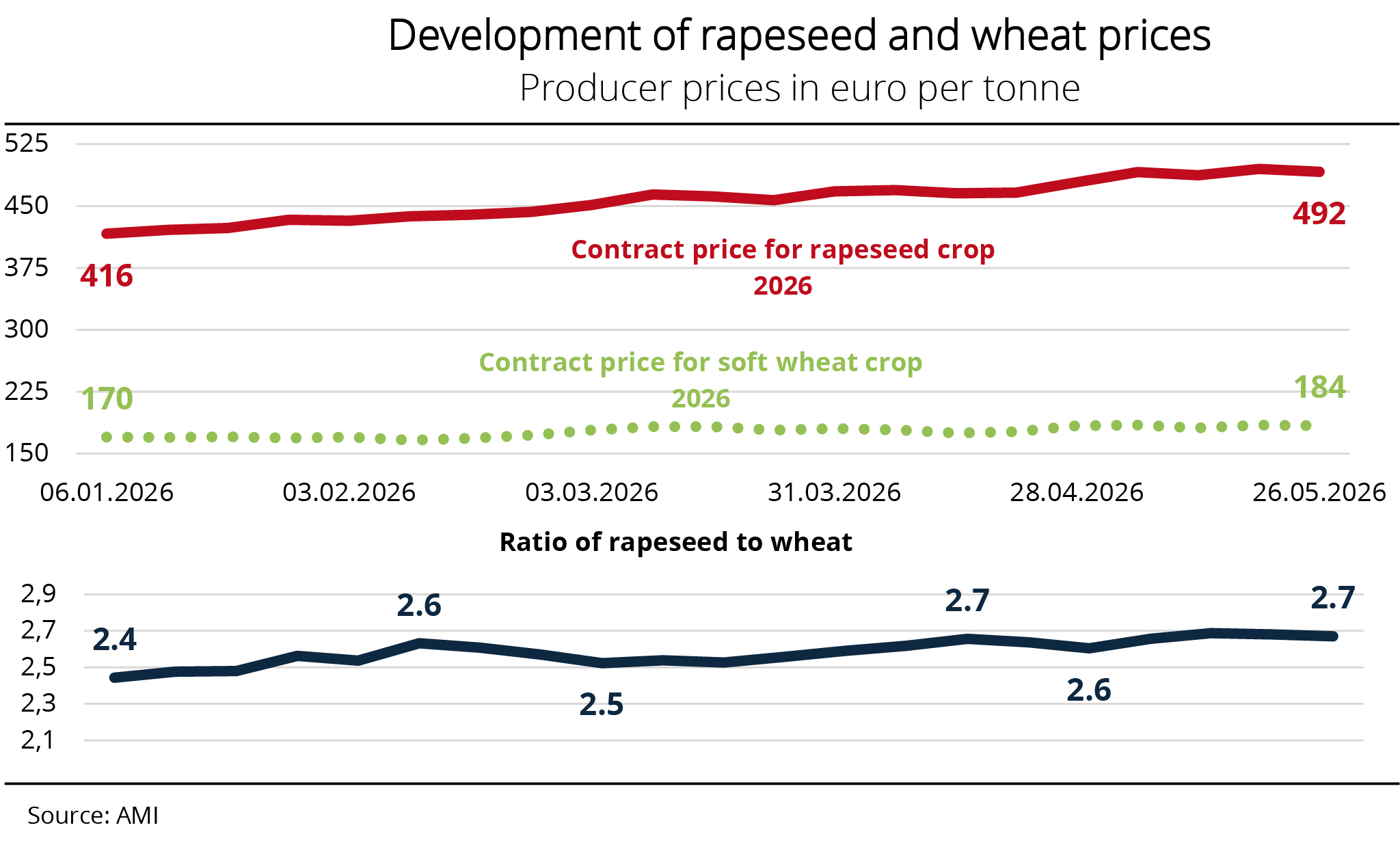

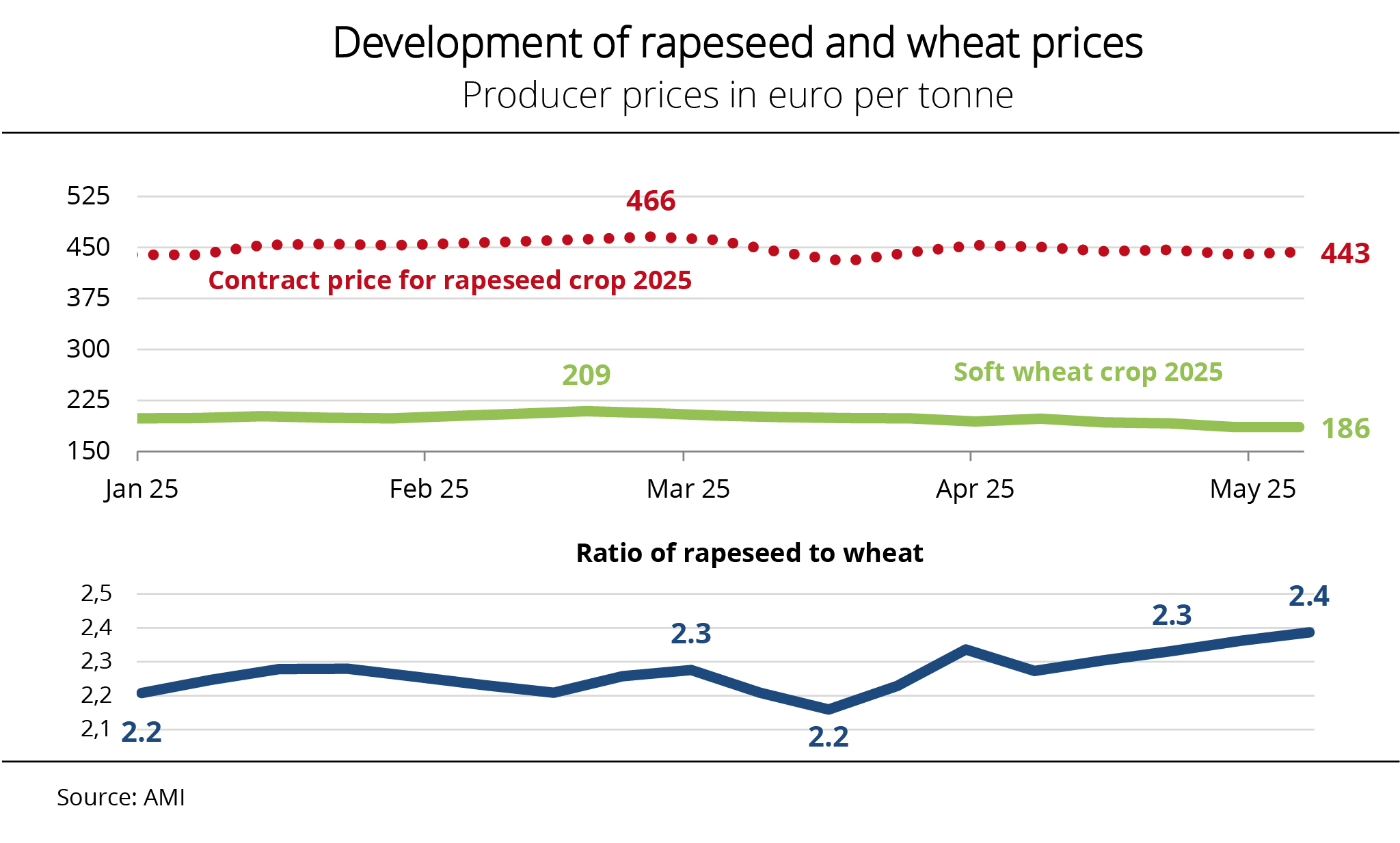

The price gap between forward contract prices for soft wheat and rapeseed from the 2026 crop has recently widened to a ratio of 1:2.7, further increasing the incentive for farmers to sow rapeseed for the 2027 harvest.

At the end of May 2026, rapeseed growers in Germany received an average of just under EUR 492 per tonne ex farm for forward contracts for the 2026 crop, more than twice the price buyers paid for one tonne of soft wheat. Rising energy prices resulting from geopolitical tensions in the Middle East have recently led to stronger prices on the Paris futures market, thereby also supporting producer prices for rapeseed. However, the resulting momentum was largely short-lived, with fundamental data remaining the key factor influencing medium-term market trends.

Producer prices for soft wheat from the 2026 crop also strengthened over the past few weeks, though to a lesser extent than those of rapeseed. At EUR 184 per tonne, they were around EUR 1.50 per tonne lower than at the same time in 2025. Current activities on the domestic market have focused on clearing warehouses and fulfilling forward contracts, with new business remaining the exception.

All things considered, the current price ratios clearly suggest that winter rapeseed is the better option. Fundamental data are stable and there are no signs of any major supply bottlenecks. Regional weather risks continue to exist but are cushioned across the EU by expansions of the production area. This means that, in general, winter rapeseed continues to offer attractive economic prospects for crop rotation and remains a competitive option for the 2026/27 season.

Chart of the week (22 2026)

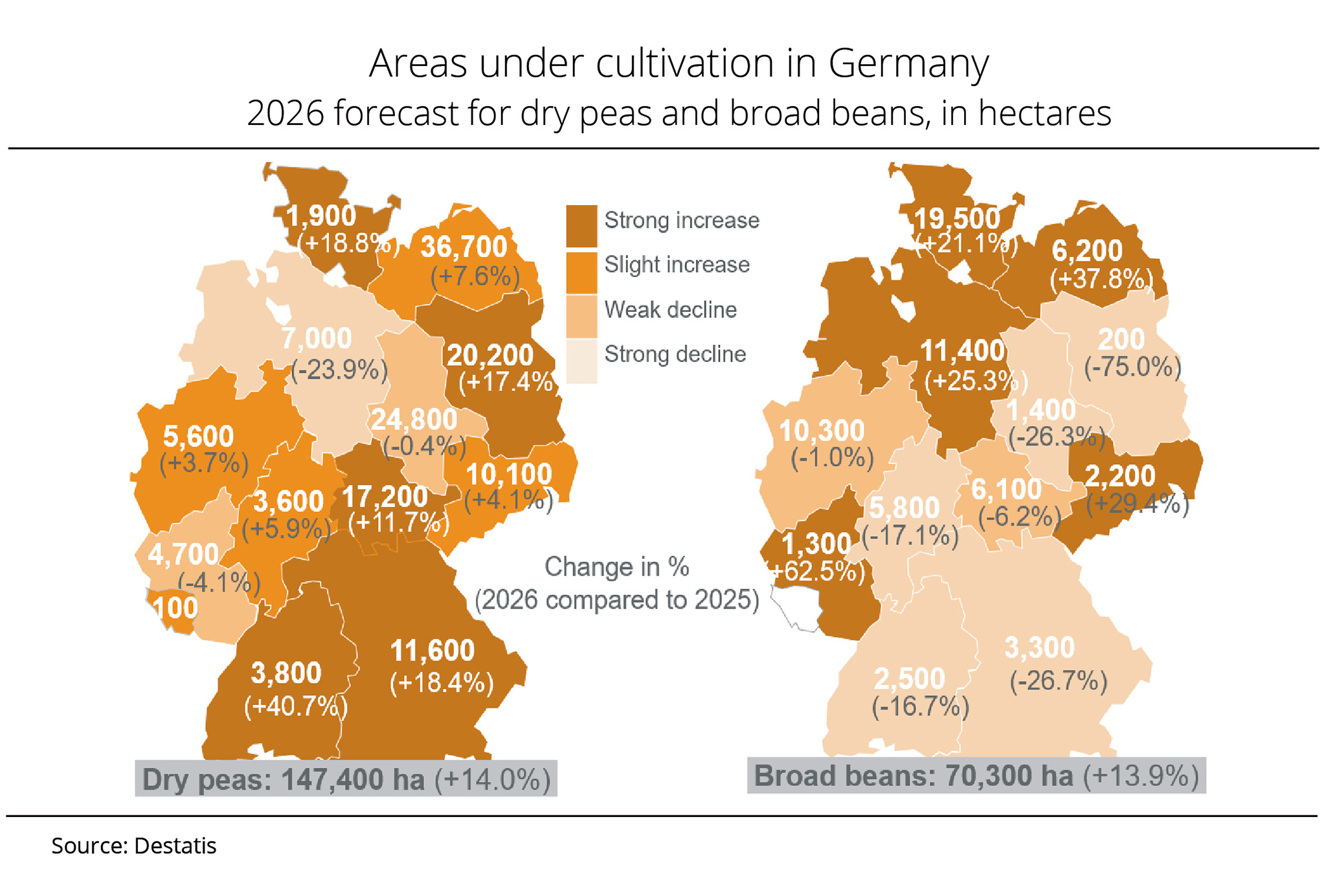

Increase in grain legume area in Germany

The German Federal Statistical Office expects a sharp expansion in grain legume area for the 2026 harvest. Production of dry peas, broad beans and soybeans has been expanded noticeably in Germany. The Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) fears that the European Commission’s plan to classify soybeans as a high-iLUC feedstock will result in massive collateral damage to soybean cultivation in the EU. UFOP has called on the German Minister of Agriculture Alois Rainer and members of the EU Parliament to stop the draft delegated regulation.

According to the German Federal Statistical Office's latest forecast of grain legume cultivation area for the 2026 harvest, the dry pea area in Germany has expanded to approximately 147,400 hectares, representing a 14 per cent rise compared to the previous year. With the exception of Lower Saxony, Rhineland Palatinate and Saxony-Anhalt, all German states are recording increases in production area. Baden-Wuerttemberg is expected to record the biggest expansion in area with an increase of 40.7 per cent, reaching 3,800 hectares. Schleswig-Holstein and Bavaria are projected to see increases of 18.8 per cent and 18.4 per cent respectively. Mecklenburg-Western Pomerania, the most important German state in terms of area, is expected to record an increase of 7.6 per cent, bringing the pea area to 36,700 hectares.

The German Federal Statistical Office also anticipates a substantial expansion in broad bean area. The 2026 broad bean area is estimated at 70,300 hectares, representing an increase of 13.9 per cent compared with 2025. However, changes vary by region. Whereas expansions prevail in the north-west, some declines have been recorded in other regions.

Soybean cultivation is also expected to have grown significantly Germany in 2026. The soybean area is expected to reach around 51,000 hectares, representing an increase of 17.8 per cent year on year. Production remains mainly located in southern Germany, with Bavaria reporting an area of 24,100 hectares (+5.7 per cent) and Baden-Wuerttemberg 7,700 hectares (+4.1 per cent). The largest percentage increases are expected in eastern Germany, with Mecklenburg-Western Pomerania doubling its area to 1,600 hectares (+100 per cent), and Saxony-Anhalt and Saxony expanding the soybean area to 6,200 hectares (+87.9 per cent) and 2,600 hectares (+ 36.8 per cent) respectively. In general, all German states are expected to see expansions in area.

The Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) regards the trend in production area as confirmation that the agricultural sector is increasingly expanding the diversity of crops in crop rotation to include grain legumes as atmospheric nitrogen-fixing flowering plants, thereby unlocking new potential for added value in arable farming. However, according to UFOP, for the positive trend to continue, it is essential that growing these crops remains profitable for farmers. The association has therefore welcomed the protein strategies announced both by the EU Commission and the German Ministry of Agriculture which aim to support production through a wide range of business incentives and thus make a sustainable contribution to protein supply.

However, the plan by the European Commission’s Directorate-General for Energy to classify soybeans worldwide as a so-called high-iLUC feedstock has met with little understanding. This could seriously undermine the desired development of farming in Europe. UFOP has therefore called upon both Council and Parliament to stop the draft delegated regulation. From UFOP's perspective, it is downright absurd that the fact that soybeans contain only 20 per cent oil should classify them as a high-iLUC feedstock when used for biofuel production. This would also deprive EU-grown soybeans of an option for creating added value. What is more, the regulation would also effectively hold European soybean cultivation responsible for a misguided international policy on rainforest protection. The UFOP has therefore called on Federal Minister Rainer to support Austria’s initiative at the Council of Agriculture Ministers in order to stop the draft. UFOP has also called on the European Parliament to put a stop to this regulatory nonsense and instead develop a polluter-pays approach to effectively tackle deforestation in South America.

Chart of the week (21 2026)

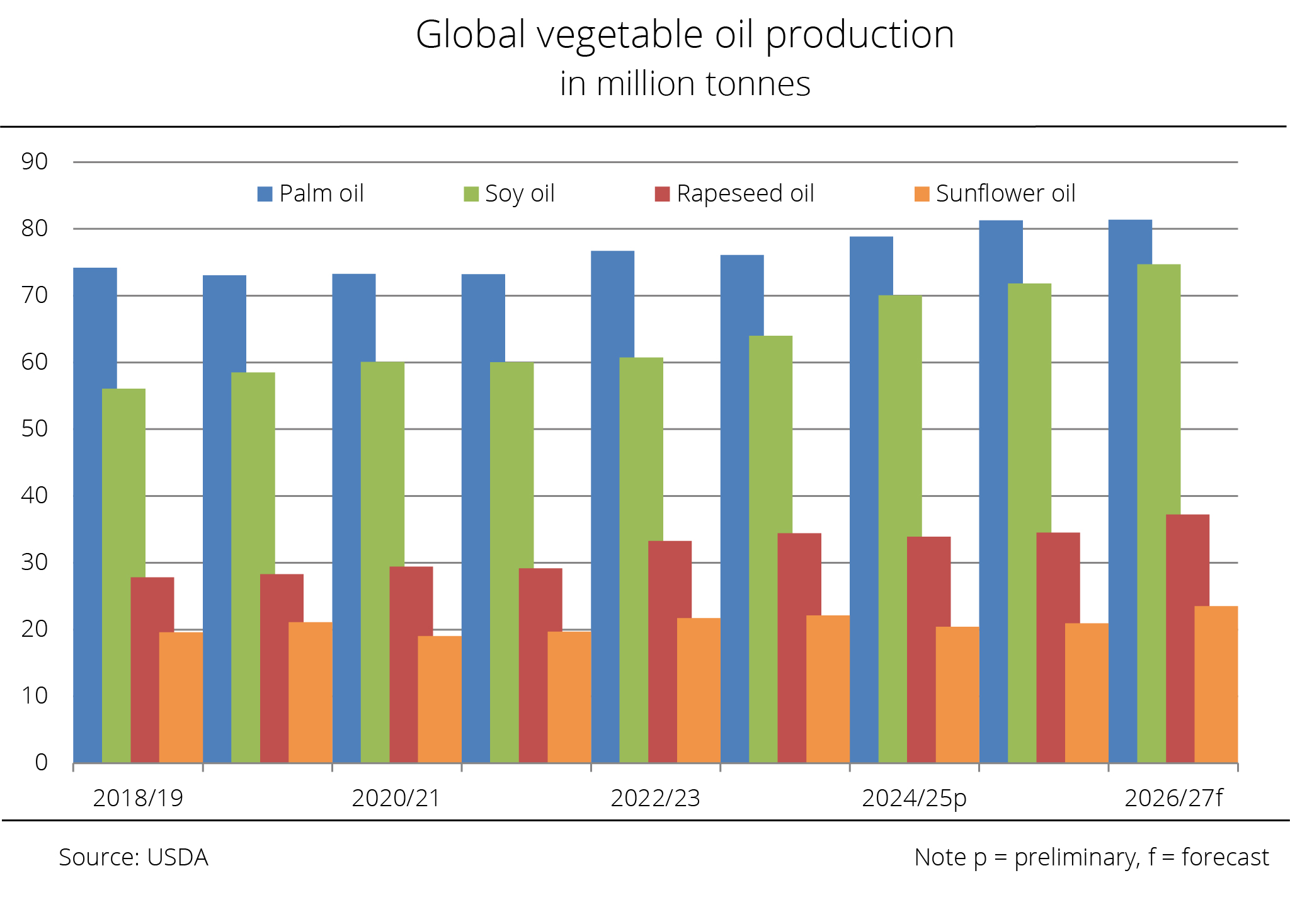

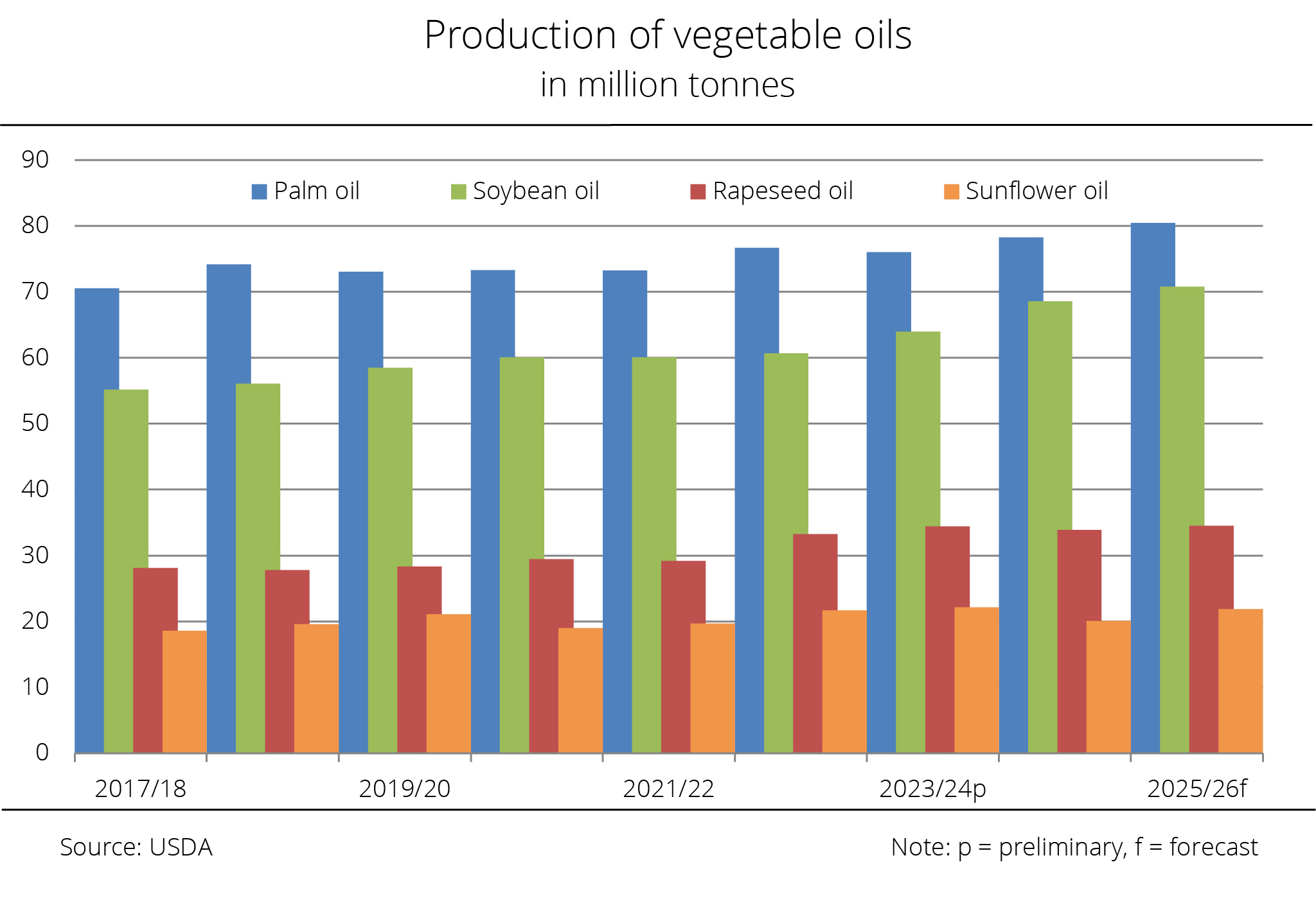

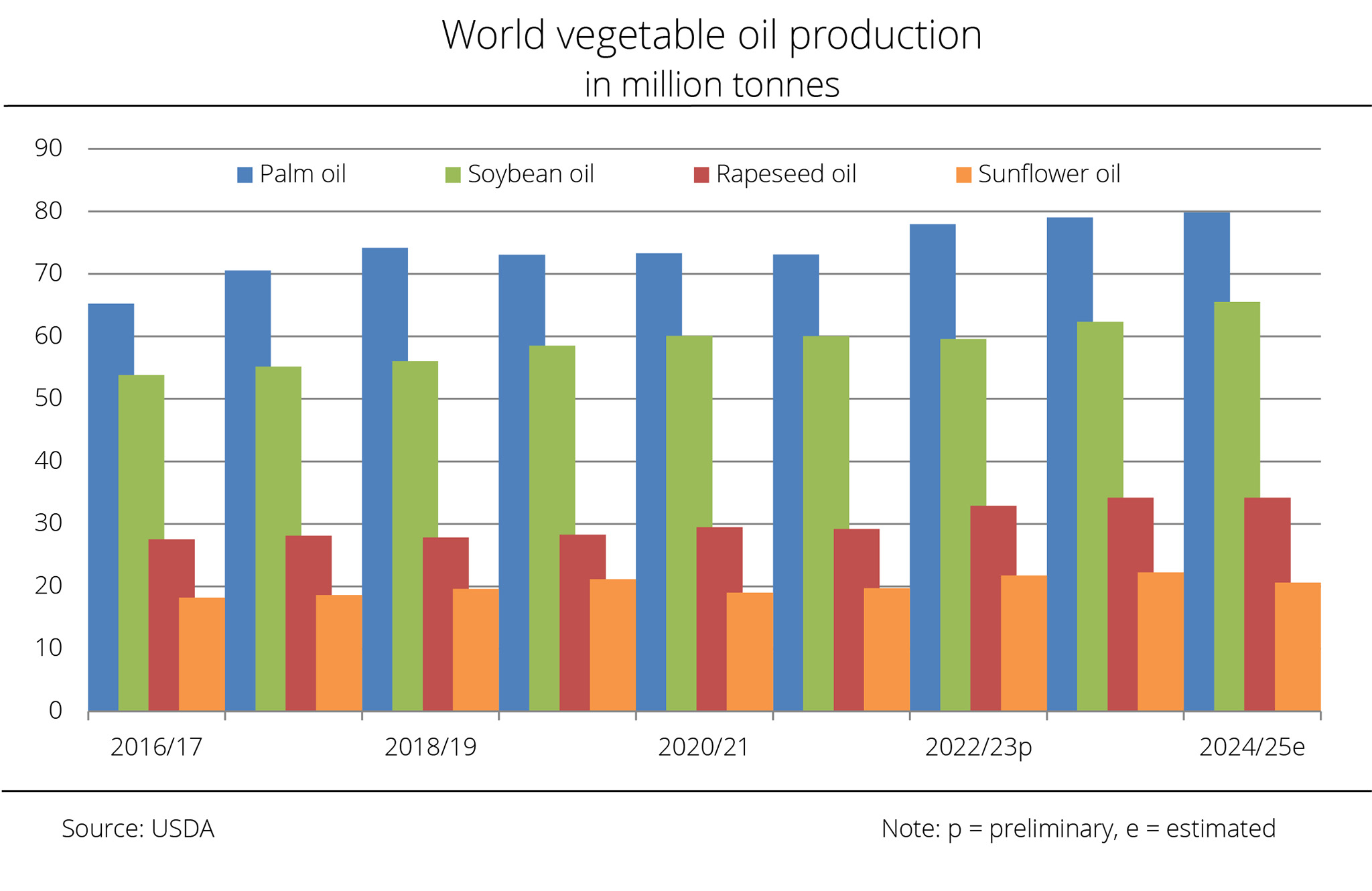

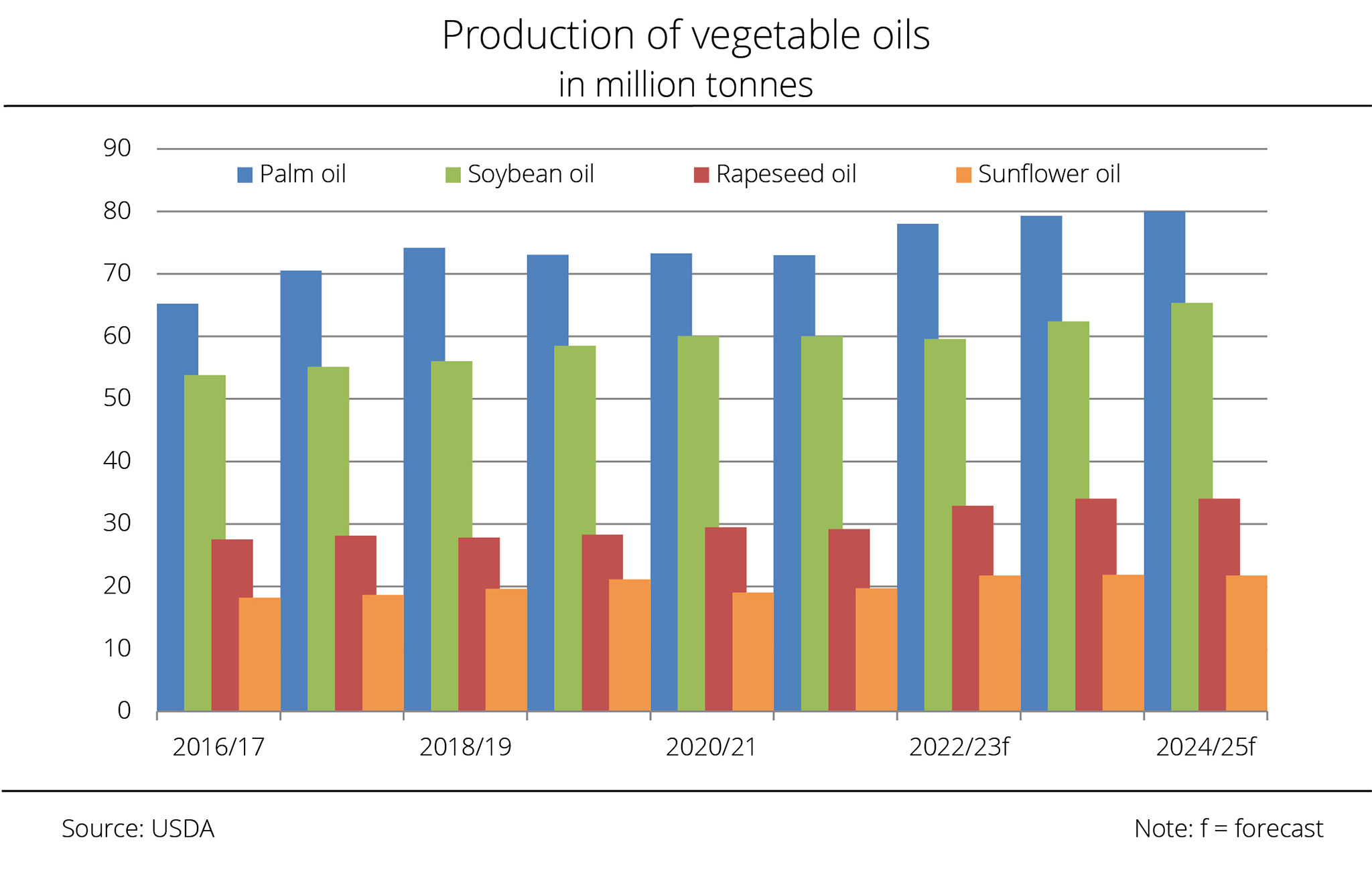

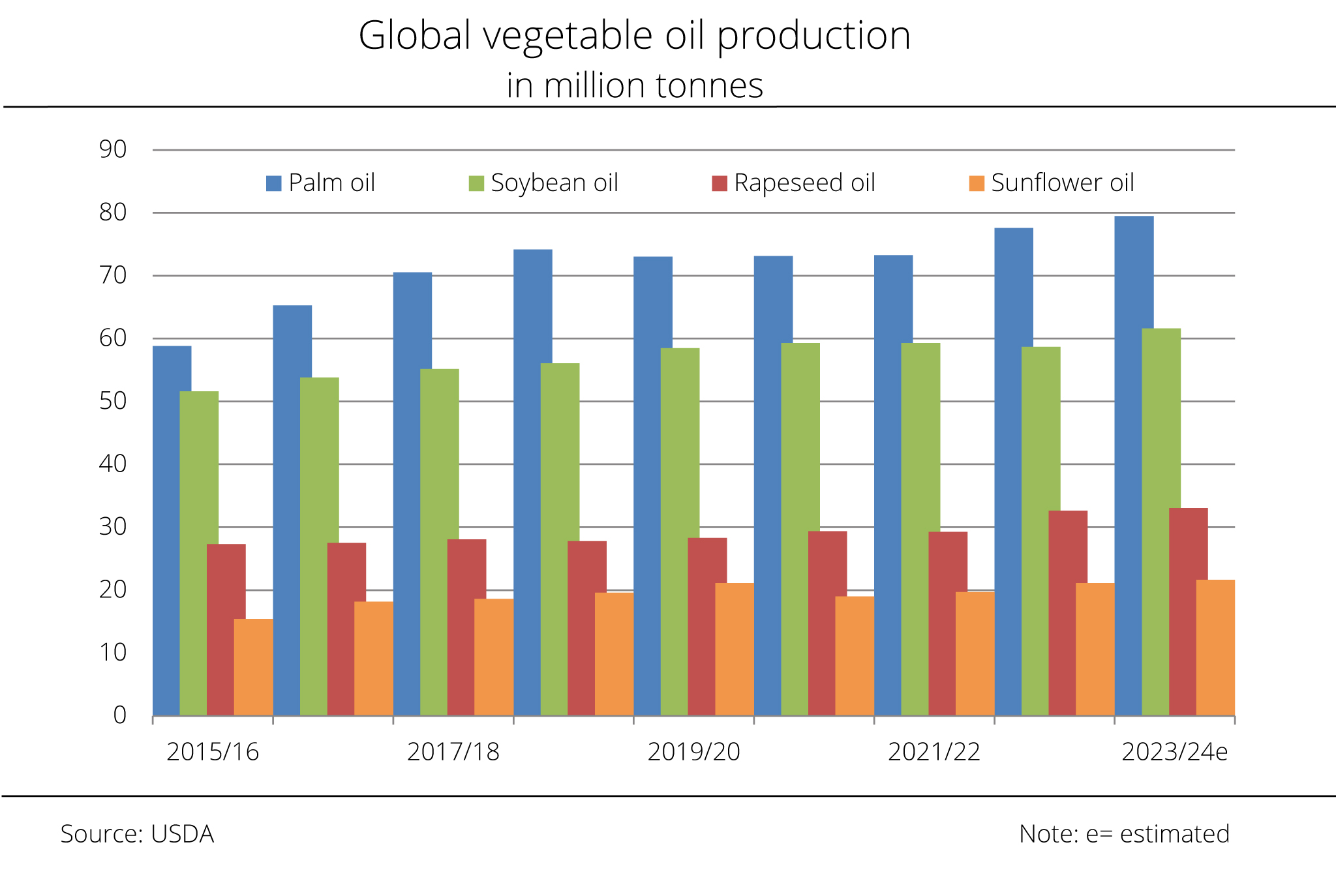

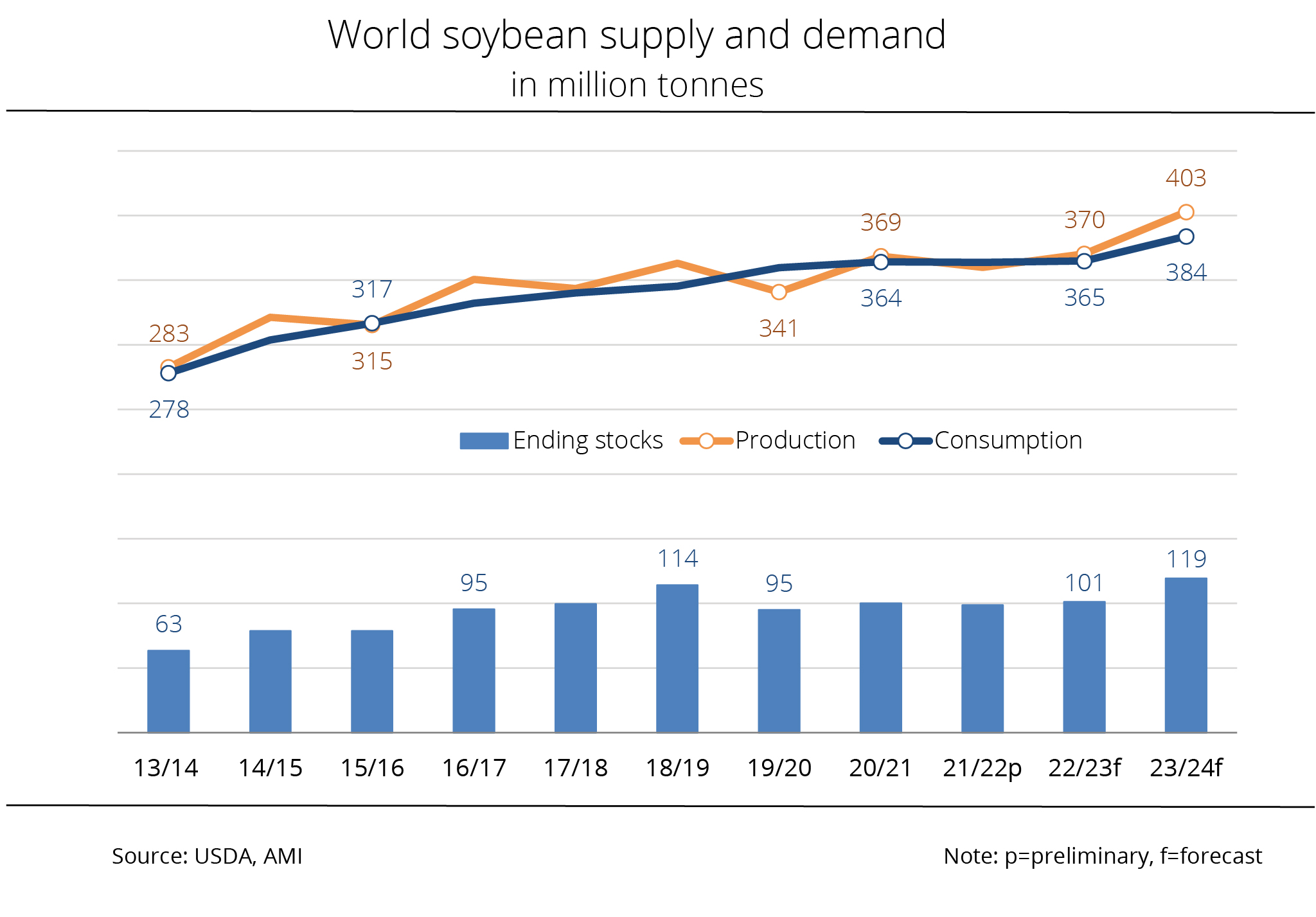

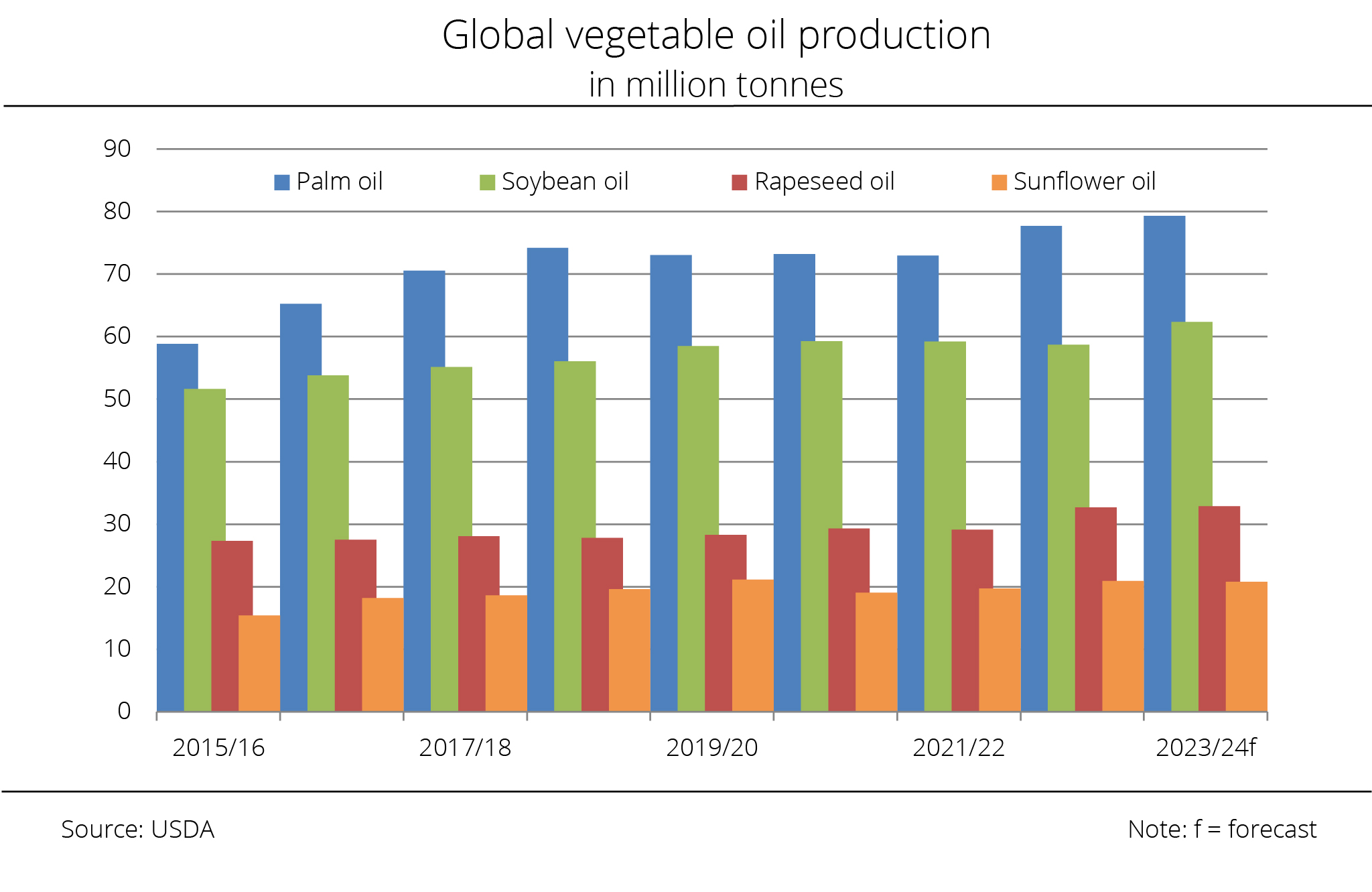

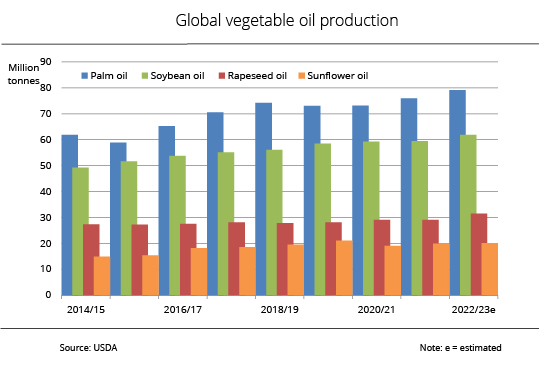

Global vegetable oil production set to hit another record high

A preliminary estimate by the US Department of Agriculture (USDA) of global vegetable oil supply and demand in 2026/27 marketing year indicates that global production is likely to reach 244.1 million tonnes, representing an increase of approximately 6.8 million tonnes compared with the current season. Supply is expected to fully cover demand, which is forecast at 237.6 million tonnes. Against this backdrop, the Union zur Förderung von Oel- und Proteinpflanzen (UFOP) sees an urgent need to reassess and adjust the cap on biofuels derived from cultivated biomass because sufficient feedstock availability serves as a buffer and strengthens security of supply.

According to research conducted by Agrarmarkt Informations-Gesellschaft (mbH) (AMI), palm oil is set to remain the world's most important vegetable oil in terms of production and consumption, with global output estimated at a record 81.4 million tonnes. This would represent an increase of 90,000 tonnes compared with 2025/26. Indonesia is expected to remain the largest producer with an output of 47.5 million tonnes, followed by Malaysia at 19.6 million tonnes and Thailand at 3.7 million tonnes.

Production of soybean oil is expected to see the most pronounced rise in the coming crop year, with the increase projected at 2.9 million tonnes, bringing total output to 74.7 million tonnes. China, by far the largest processor of soybeans, is anticipated to remain the leading producer of soybean oil with 21.4 million tonnes, followed by the United States with just over 14.8 million tonnes.

Production of rapeseed oil in 2026/27 is expected to increase 2.7 million tonnes compared with the current season, reaching 37.2 million tonnes. Sunflower seed oil output is projected to grow by around 2.6 million tonnes to 23.5 million tonnes, primarily due to higher production in Ukraine, Russia and the EU-27.

The Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) has underlined the growing demand for waste oils and fats for biodiesel and HVO production associated with the implementation of RED III in EU member states and ambitious quota policies in North and South America. In the case of waste oils, UFOP estimates that between 5 per cent and 10 per cent of global vegetable oil production can be collected as waste oil. The global volume of waste oil suitable for collection is therefore only around 12 to 24 million tonnes. According to UFOP, shipping and aviation have also become competitors for this feedstock, because under EU legislation biofuels counted towards targets in these sectors must be produced from waste or residual materials.

UFOP has stressed that this feedstock displacement effect is undermining the decarbonisation of road transport. Consequently, in view of the forthcoming revision of the Renewable Energy Directive (RED IV), UFOP has raised the question of whether the caps on biofuels from cultivated biomass and their contribution to security of supply need to be reviewed. The reason given is that adjusting the caps would create a supply buffer that would help meet statutory blending and climate change mitigation targets. UFOP has also noted critically that, in its latest report, the Expert Council on Climate Issues concluded that the German government’s Climate Action Programme for the transport sector is inadequate and based on little more than hope.

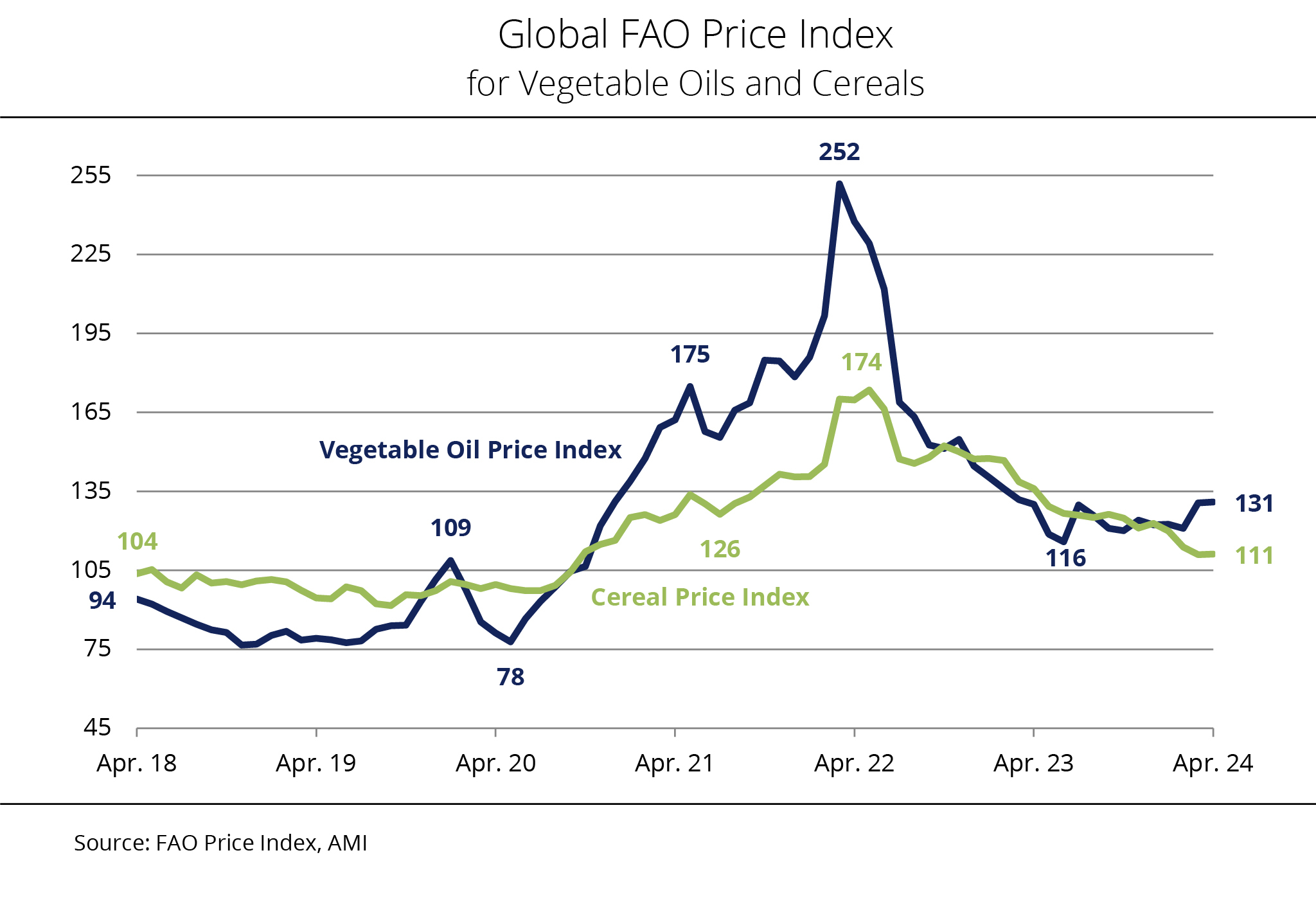

Chart of the week (20 2026)

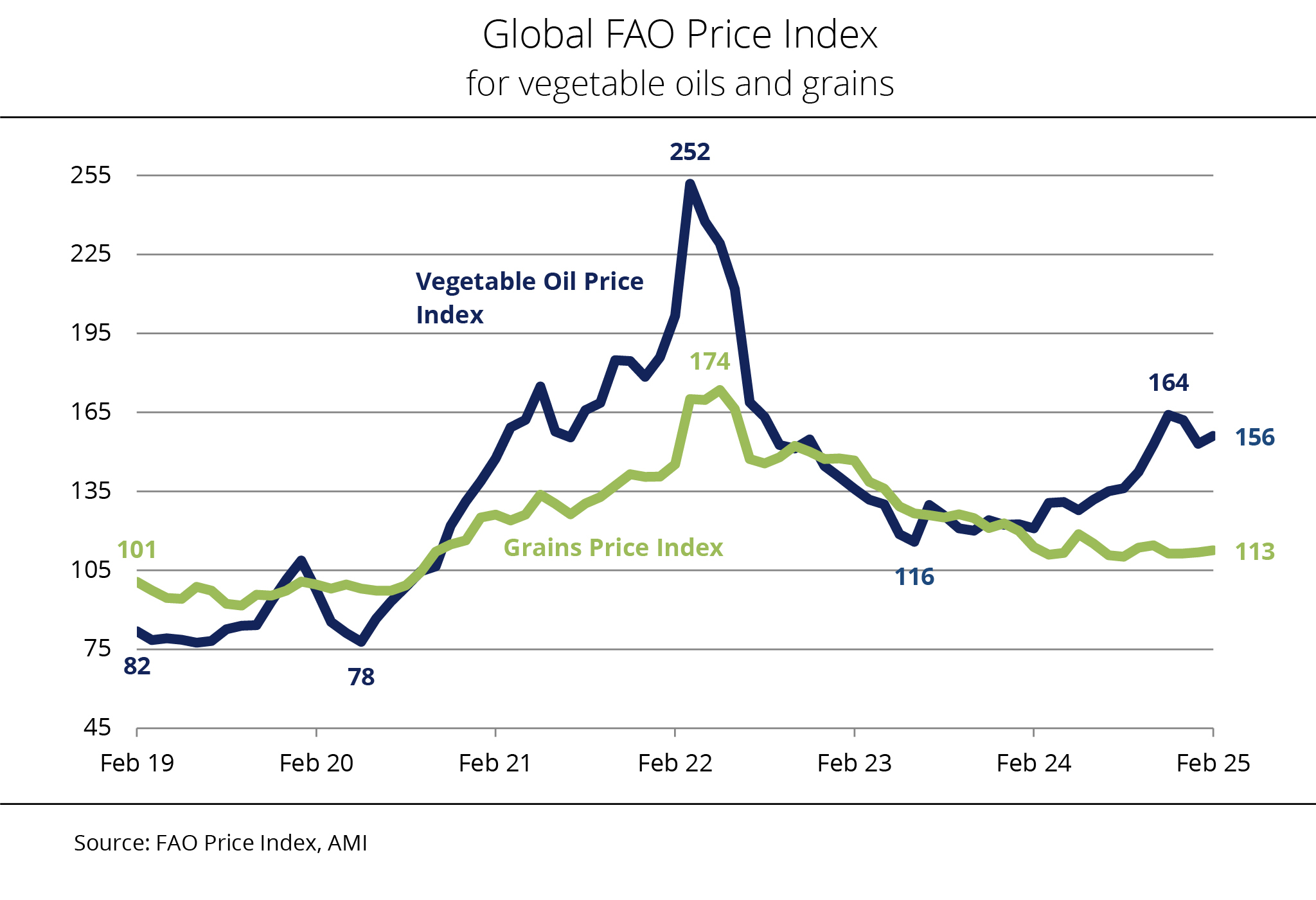

Vegetable oil prices at a multi-year high, grain prices showed a slight increase

For the 2025 calendar and quota year, biodiesel Download

For the 2025 calendar and quota year, biodiesel Download

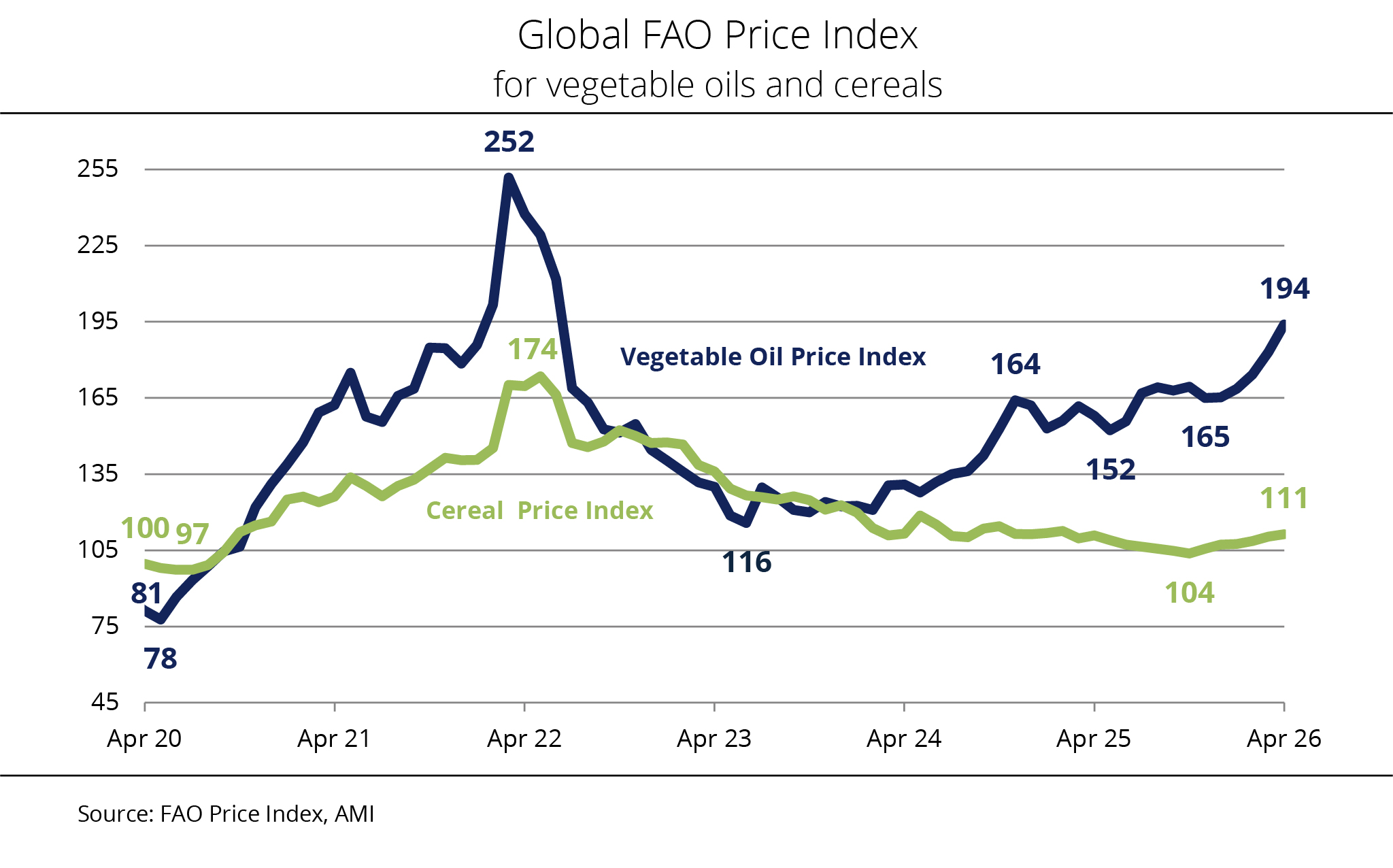

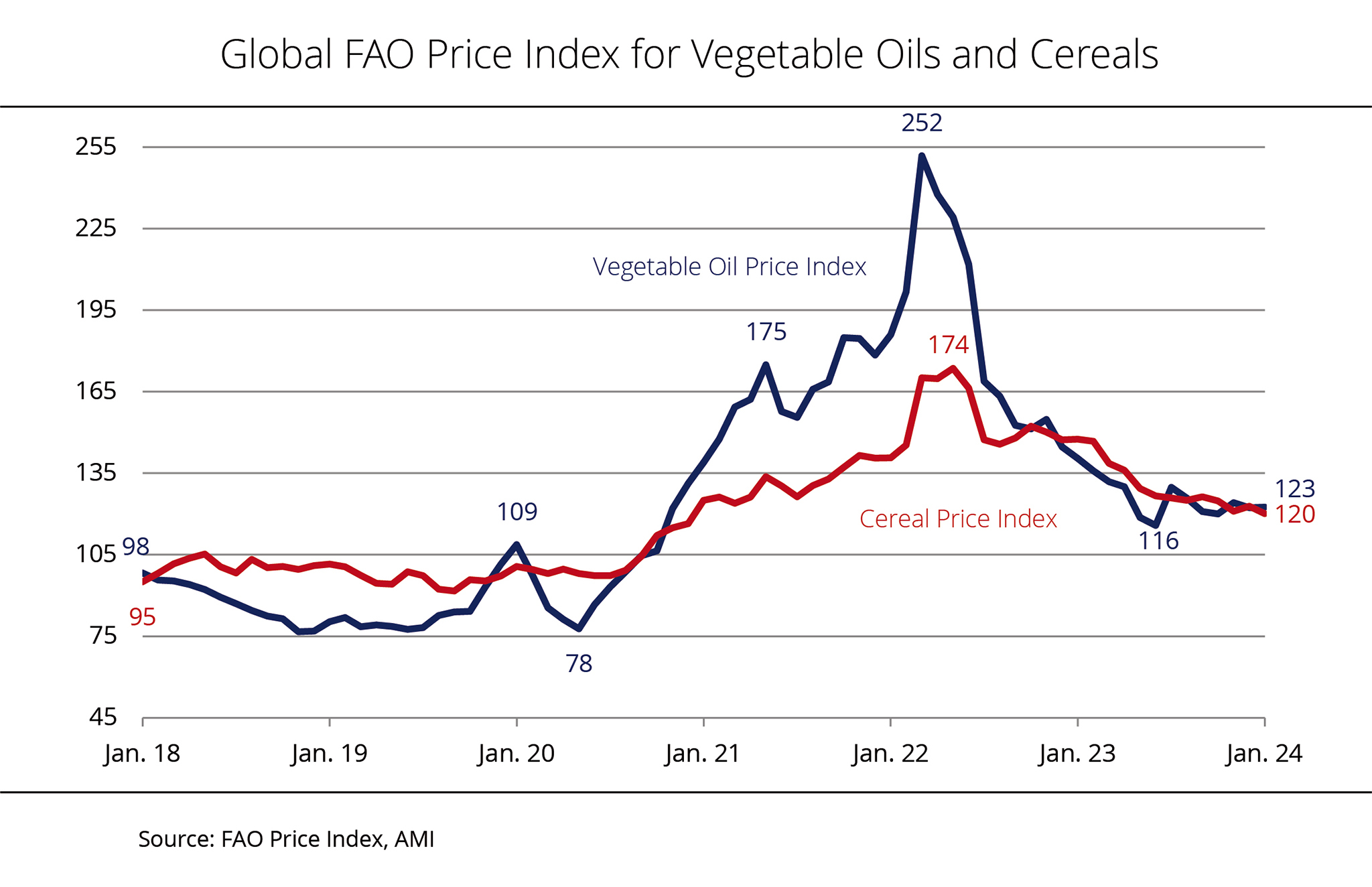

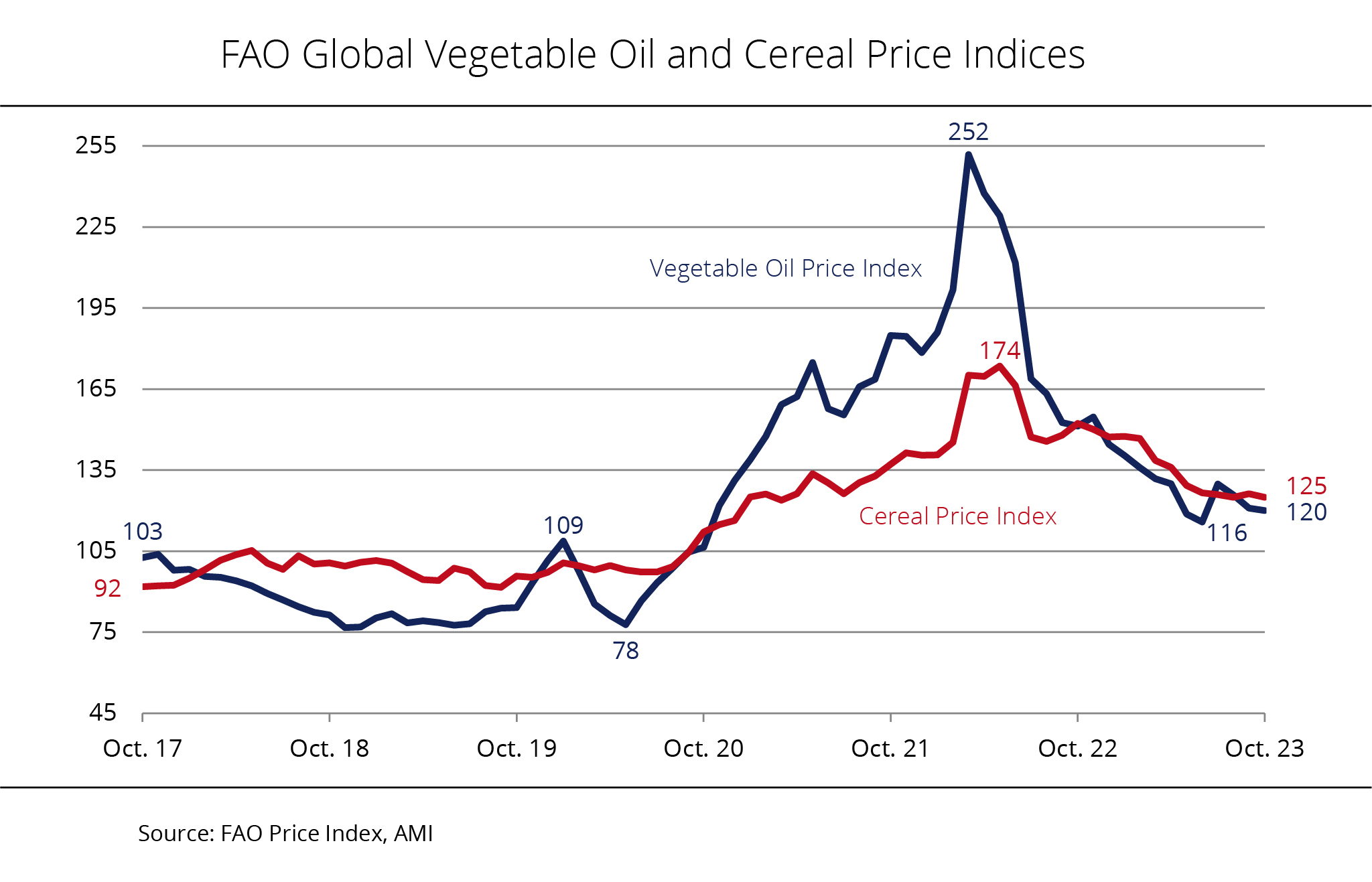

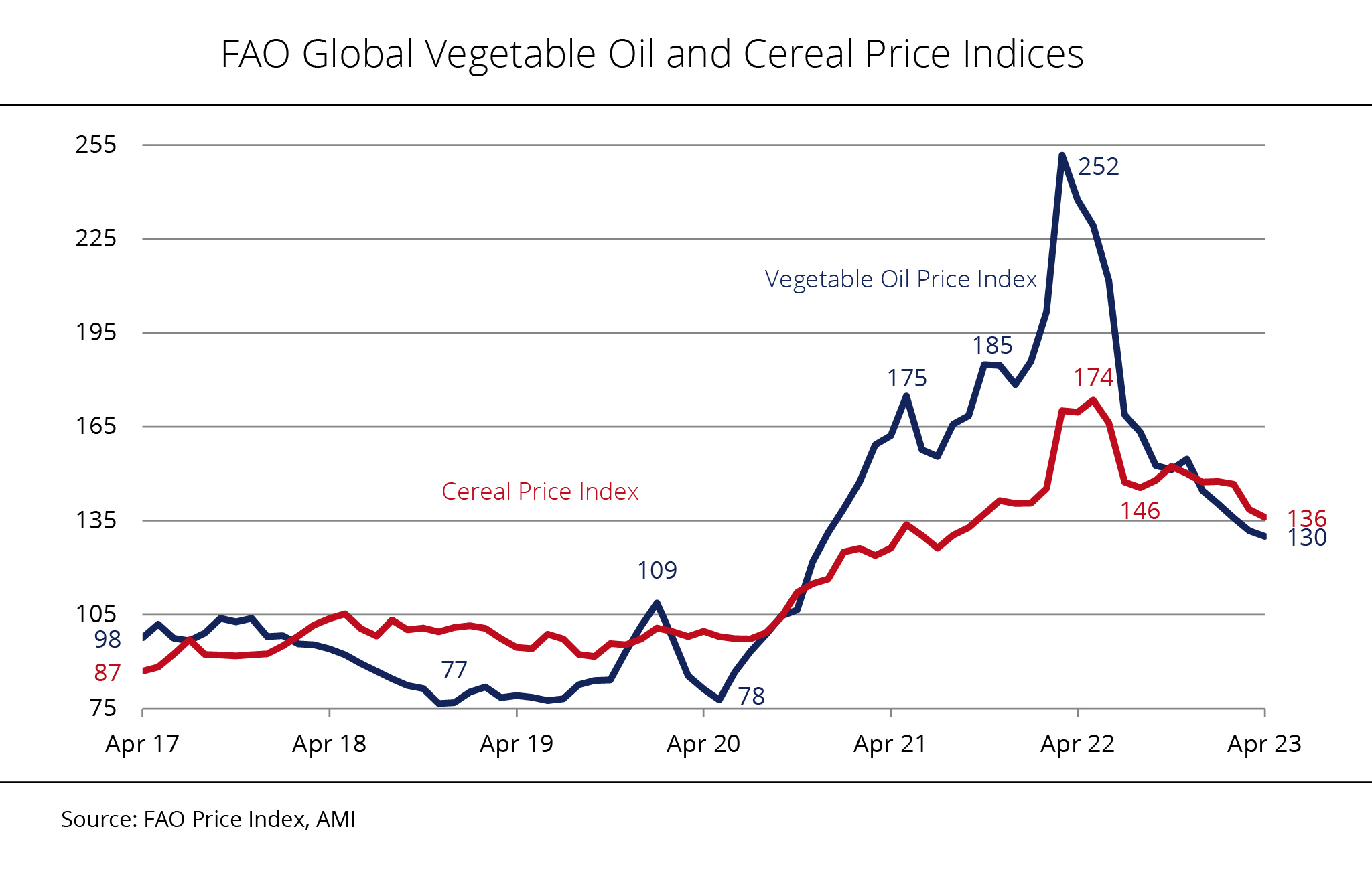

The FAO vegetable oil price index climbed to a four-year high in April. International grain prices also increased. Prices were driven by drought risks, weather-related uncertainty, and strong demand.

The FAO cereal price index rose to an average of 111.3 points in April, up 0.8 per cent from the previous month and 0.4 per cent compared with the previous year's level. Wheat prices increased around 0.8 per cent, driven by drought risks in the US, growing uncertainty of rainfall in Australia and expectations of a reduction in wheat plantings and yields per hectare due to high fertiliser and energy costs. Maize prices picked up 0.7 per cent on support from seasonally tight availability, weather-related concerns in Brazil and the US, and buoyant demand from the ethanol sector.

The FAO price index for vegetable oils also went up in April, reaching an average of 193.9 points (+5.9 per cent month-on-month), its highest level since July 2022. More specifically, palm oil prices increased for the fifth successive month, underpinned by expectations of rising demand for biofuels, political incentives in major palm oil-producing countries, and higher crude oil prices. Soybean and rapeseed oil prices also strengthened. Sunflower seed oil prices remained supported by tight supply in the Black Sea region, whereas prices in Argentina saw a slight decline due to a seasonal increase in processing and greater export availability.

The FAO vegetable oil price index tracks monthly changes in international export prices for vegetable oils and grains, calculated as a trade-weighted average.

Chart of the week (19 2026)

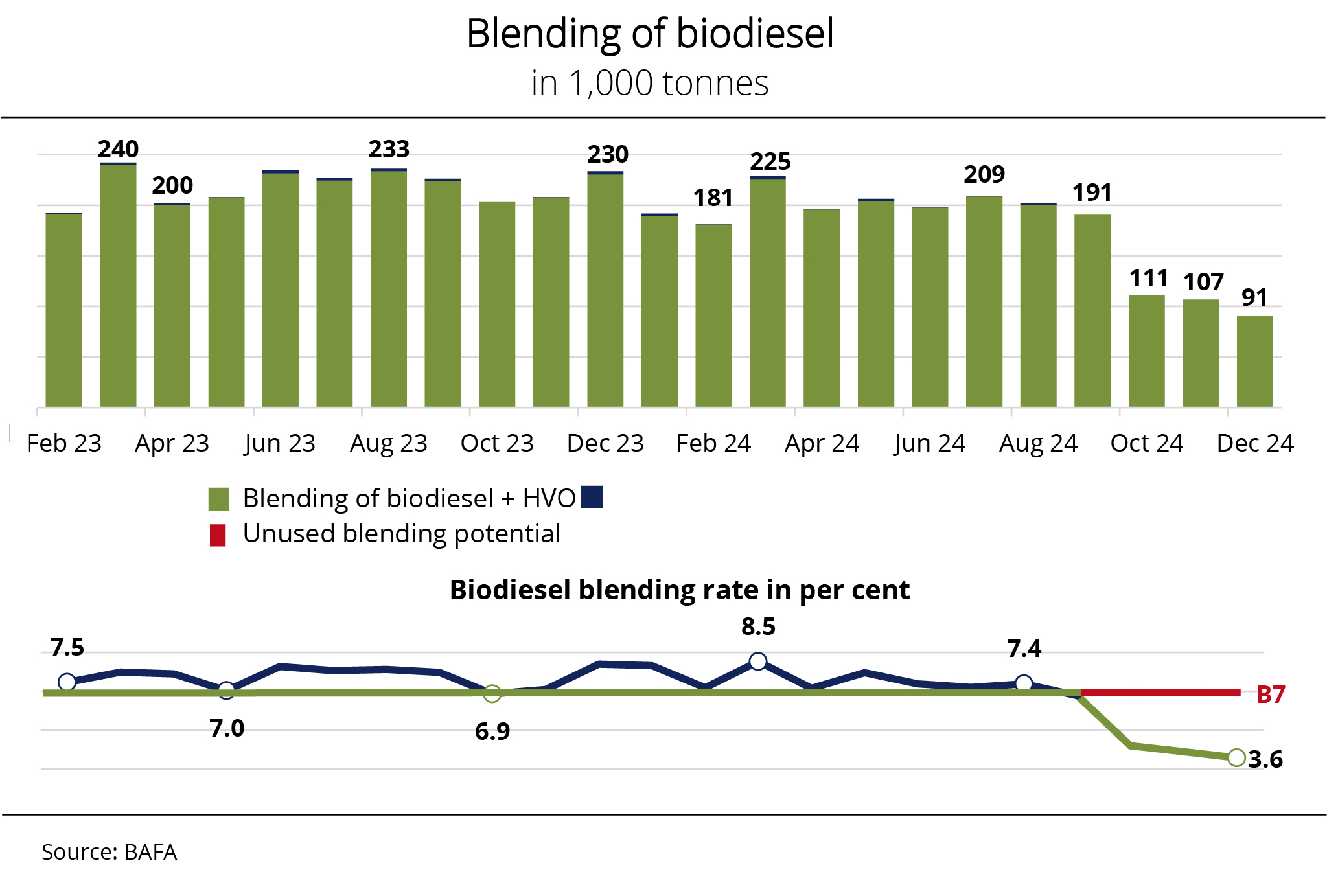

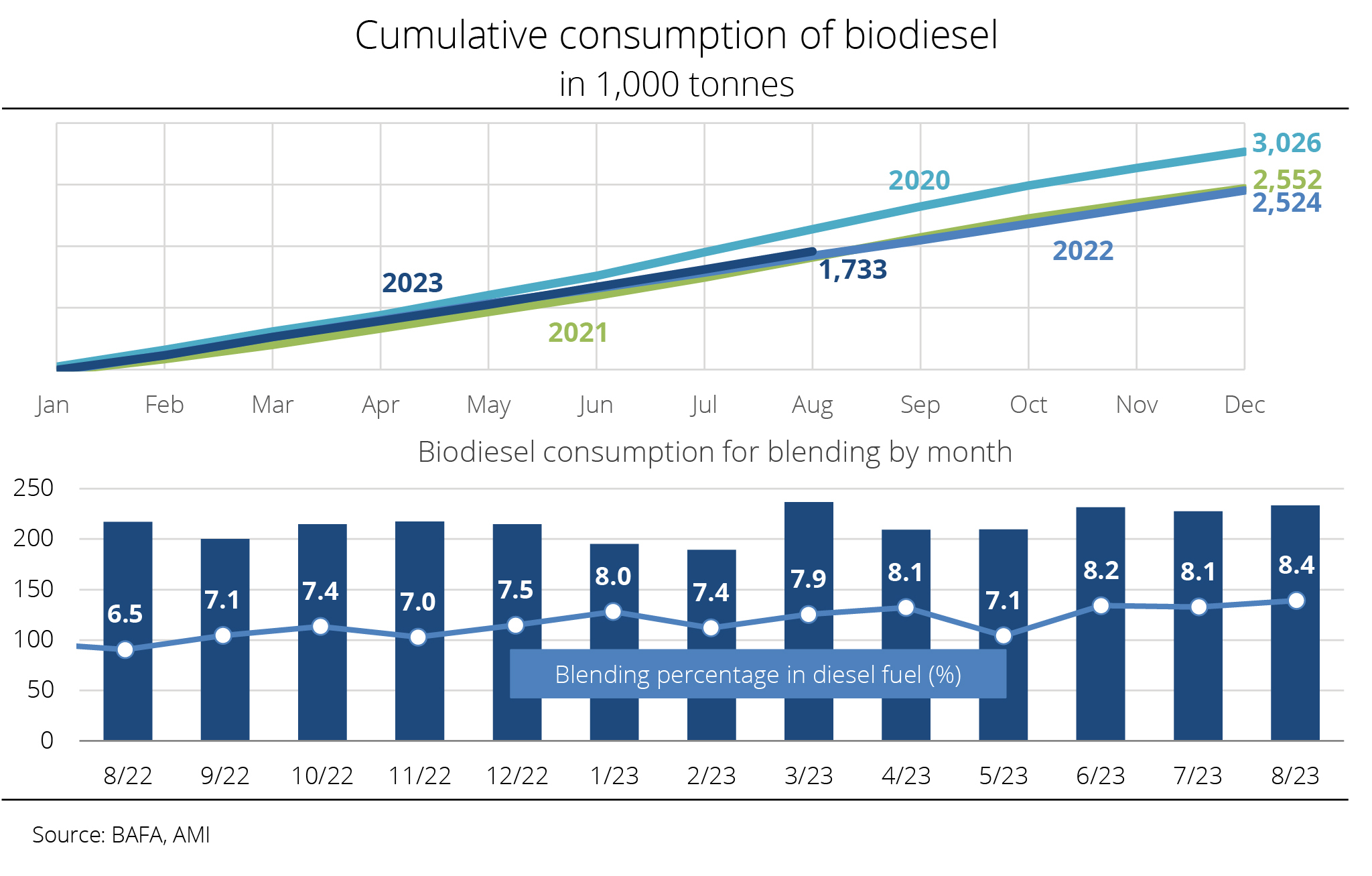

More biodiesel than HVO in blends in the 2025 quota year

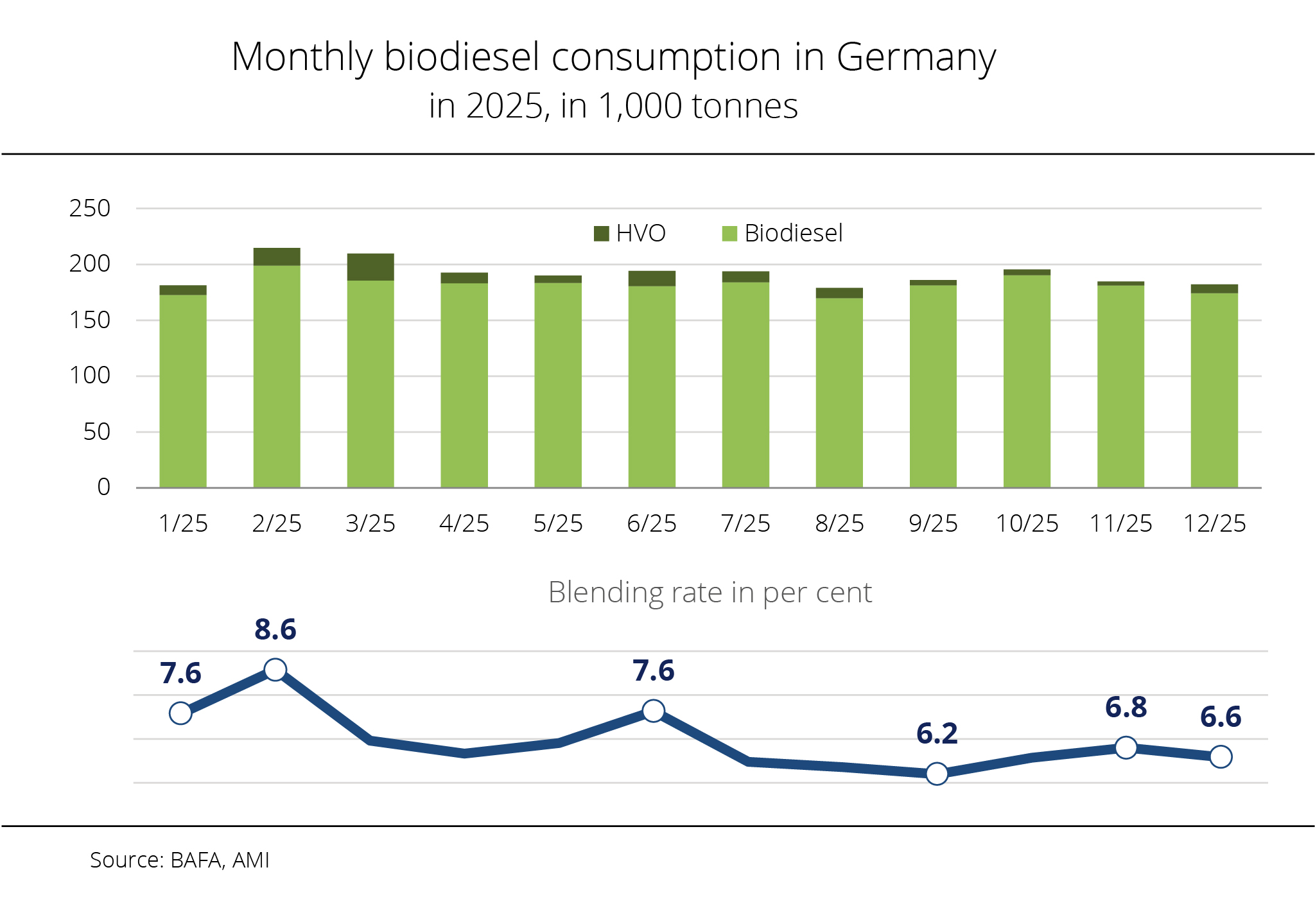

For the 2025 calendar and quota year, biodiesel consumption shows a clear upward trend compared to the historically weak previous year. HVO volumes fell short of the previous year's level because quota obligations could be met more cost-effectively using biodiesel within the technical cap – the fuel standard for diesel (B7). It is noticeable that, at the same time, sales of the pure HVO fuel (HVO100) increased.

In 2025, biodiesel incorporation in blends was generally at a stable level with monthly fluctuations. After 181,400 tonnes in January, consumption reached a preliminary record high of 214,868 tonnes in February. In the months that followed, consumption fluctuated between approximately 180,000 tonnes and 200,000 tonnes and declined slightly towards the end of the year, falling to 182,230 tonnes in December. The largest volume of HVO was used in March 2025, totalling 24,300 tonnes. Over the remainder of the year, monthly volumes slipped below 10,000 tonnes, with one exception in June. The lowest value, 3,600 tonnes, was recorded in November.

According to information published by Agrarmarkt Informations-Gesellschaft (mbH), the use of biodiesel for blending in the 2025 calendar year totalled just under 2.2 million tonnes, which was up around 12 per cent year on year. The HVO volume amounted to approximately 118,900 tonnes, representing a 17 per cent decline compared with 2024. At 31.2 million tonnes, the use of diesel fuel exceeded the previous year's level by just over 2 per cent. It should be noted that, according to figures from the Federal Office for Economic Affairs and Export Control (BAFA), the marketing of pure HVO fuel (HVO100) has grown significantly to approximately 132,700 tonnes, whereas biodiesel as a pure fuel (B100) plays a minor role at approximately 6,015 tonnes. The Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) has noted that the success of the mineral oil trade’s HVO100 sales campaign is clearly evident, even though the fuel is more expensive than biodiesel.

From UFOP's perspective, the 2025 quota year once again confirms the compensation effect resulting from double counting biofuels derived from certain waste-based feedstock coupled with efficiency in reducing greenhouse gas emissions. This is because these feedstocks are accounted for in the GHG balance calculation with a GHG value of zero grams of CO2. Although the Bundesanstalt für Landwirtschaft (Federal Office for Agriculture and Food/BLE) will not publish its Evaluation Report for 2025 until the end of the year, UFOP expects the feedstock composition to be similar to that of the previous year.

For the 2026 quota year, according to UFOP, physical demand is expected to rise as a result of the GHG quota obligation being raised from 10.6 per cent to 12.1 per cent and the retroactive elimination of double counting as of January 2026. UFOP has noted that it is currently impossible to assess whether and to what extent GHG emissions trading will nevertheless reduce physical demand. The association has therefore strongly criticised BAFA, as the competent authority, for having failed for months to fulfil its obligation to publish monthly consumption figures for fossil fuels and biofuels in a timely manner.

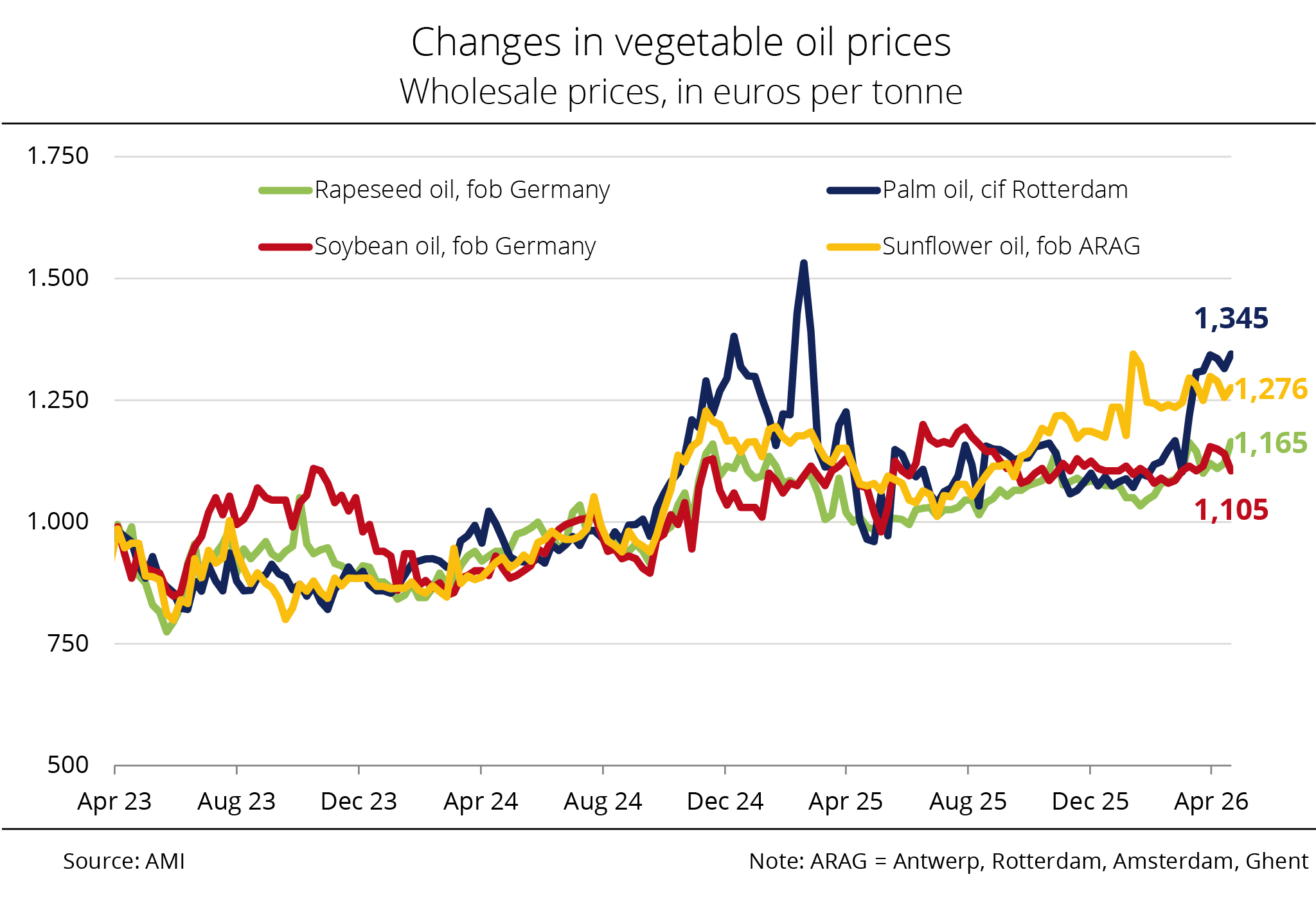

Chart of the week (18 2026)

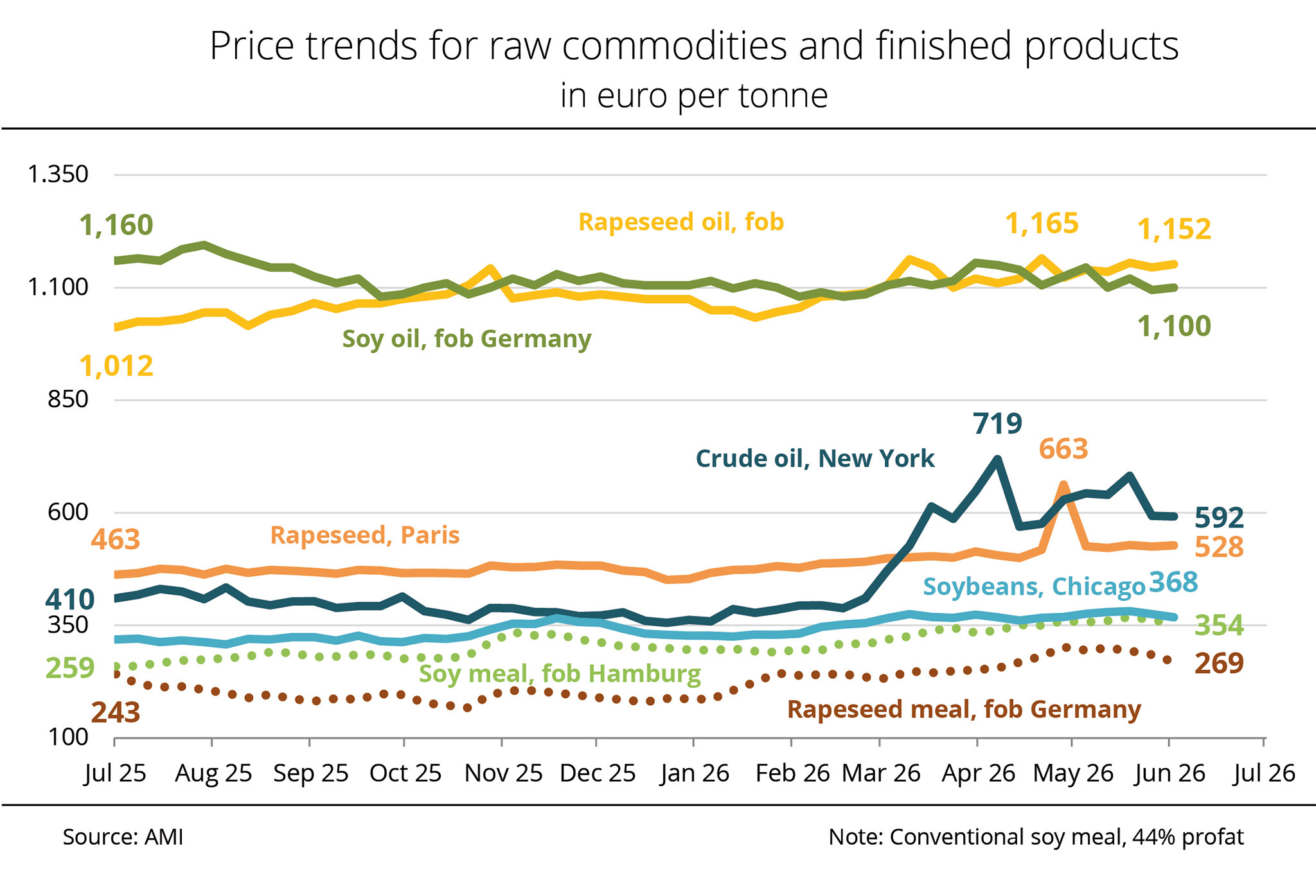

Crude oil sets the pace – vegetable oils pick up momentum

Geopolitical risks and higher crude oil prices are supporting vegetable oil markets. Palm oil is also benefiting from biodiesel policy developments in Southeast Asia.

Vegetable oil prices edged up at the beginning of March. After the escalation in the Middle East, crude oil surged, incorporating a considerable risk premium. Since then, the oil price shock has been affecting agricultural markets primarily via the energy and biofuel markets, providing particular support for vegetable oil prices. Higher crude oil prices tend to improve the competitive advantage of biodiesel and, consequently, also the demand outlook for soybean oil and rapeseed oil. At the end of March, asking prices for soybean oil were at EUR 1,155 per tonne fob German mill, up approximately 6 per cent from the end of February. The US biofuels policy provided additionalsupport. However, this price level could not be maintained as the situation developed, with prices recently falling to around EUR 1,105 per tonne.

Rapeseed oil prices were at roughly EUR 1,165 per tonne on 21 April 2026, representing a nearly 18 per cent increase compared with the same time a year ago. Demand remained generally muted. Market participants acted with restraint, observing further developments. The increasingly tight supply of rapeseed oil raffinate has so far failed to stimulate further purchases.

From the perspective of the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP), the extent to which the resolution adopted by the German Bundestag on the future development of the greenhouse gas quota will affect the national market remains to be seen. Other EU member states are also required to transpose the RED III requirements into national law. The higher RED III targets give reason to expect that quota obligations for biofuels will have to be raised in all member states. UFOP expects EU rapeseed production to benefit from the more ambitious quota requirements. In view of the 2026 harvest and sowing, the association anticipates a sustained supportive effect on oilseed prices.

UFOP has also pointed out that the amount of biofuels derived from rapeseed oil and other crops used is limited due to national caps. Against this backdrop, the association sees no reason to revive the'food versus fuel' debate.

Palm oil prices have also increased since the beginning of March and recently climbed to the top of the vegetable oil price ranking, reaching the equivalent of EUR 1,345 per tonne. Particular support comes from expectations of rising demand for biodiesel in the two largest palm oil-producing countries, Indonesia and Malaysia. These expectations could limit the export potential of the leading palm oil suppliers and tighten global supply. On the other hand, prospects of record global palm oil production and a simultaneous slowdown in demand could counteract these price supportive factors.

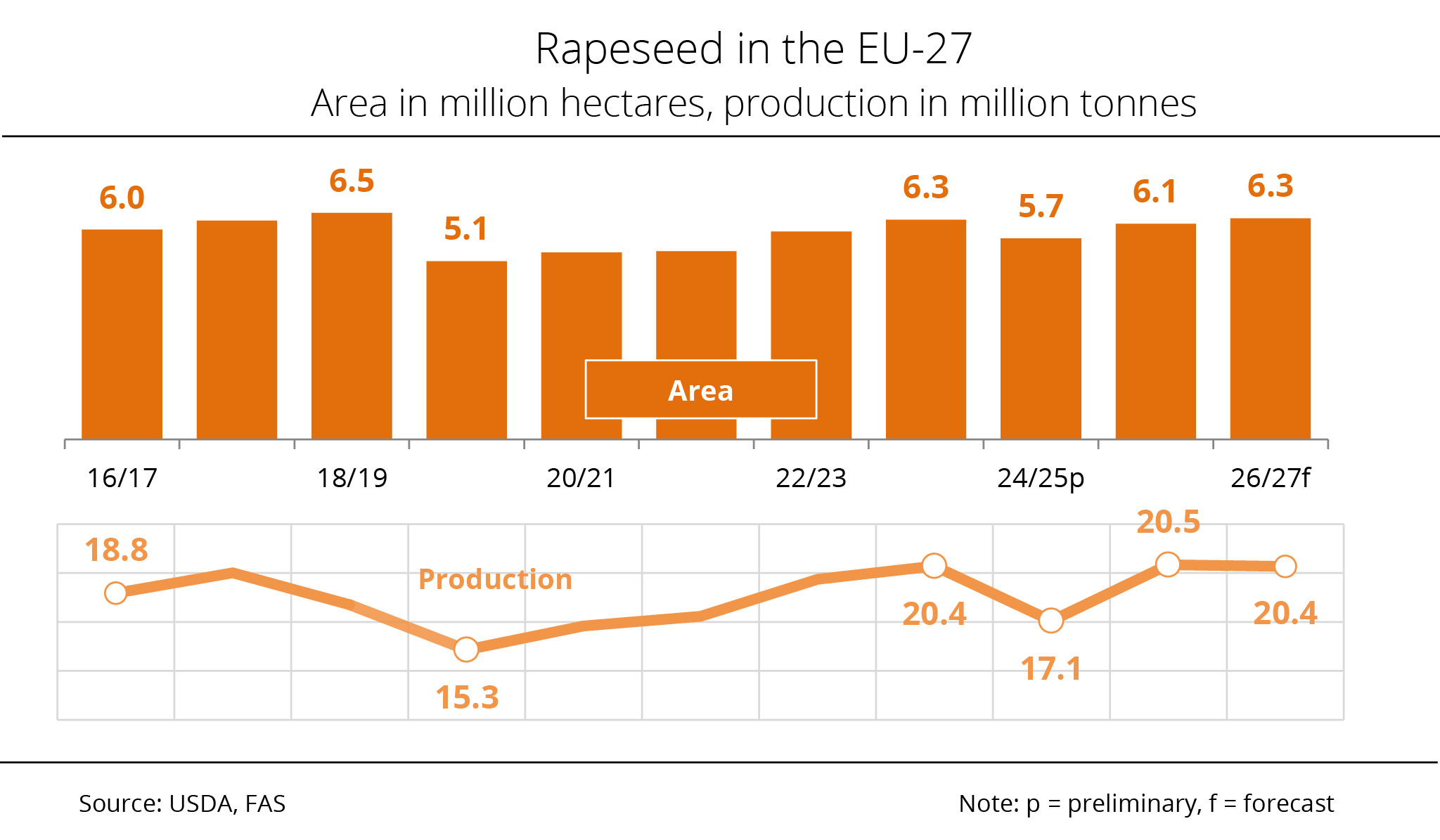

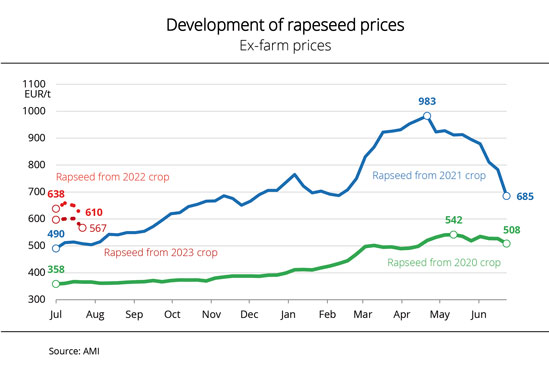

Chart of the week (17 2026)

EU rapeseed area expected to rise in 2026

USDA experts expect an expansion in the rapeseed area in the European Union for the 2026 harvest. Attractive producer prices for rapeseed in the autumn of 2025 encouraged farmers to expand the area under cultivation.

In its recently published initial outlook, the USDA Foreign Agricultural Service (FAS), based in Vienna, estimated the EU rapeseed area for the 2026 harvest at an anticipated 6.3 million hectares. This represents an expansion of approximately 2.7 per cent compared with the previous year. Alongside attractive contract prices at the time of sowing, another factor driving this development is the agronomic significance of rapeseed as a leaf crop that is essential in cereal-dominated crop rotations and that promotes biodiversity. In some regions in Germany, flowering rapeseed fields are currently a typical sight in the countryside, reflecting the importance of this crop in a particularly striking way. These yellow areas are not only a defining feature of the landscape but also reflect a versatile form of land use that combines food production, energy generation and agriculture. Based on expected average yields, the FAS projects the 2026 EU harvest at 20.4 million tonnes, slightly below the previous year's figure of 20.5 million tonnes.

France, Germany, Poland and Romania together account for around three quarters of total EU production. The FAS expects the rapeseed area to increase in all these countries. The International Grains Council (IGC) recently published a slightly more cautious outlook, expecting the rapeseed area to remain stable at around 6.1 million hectares.

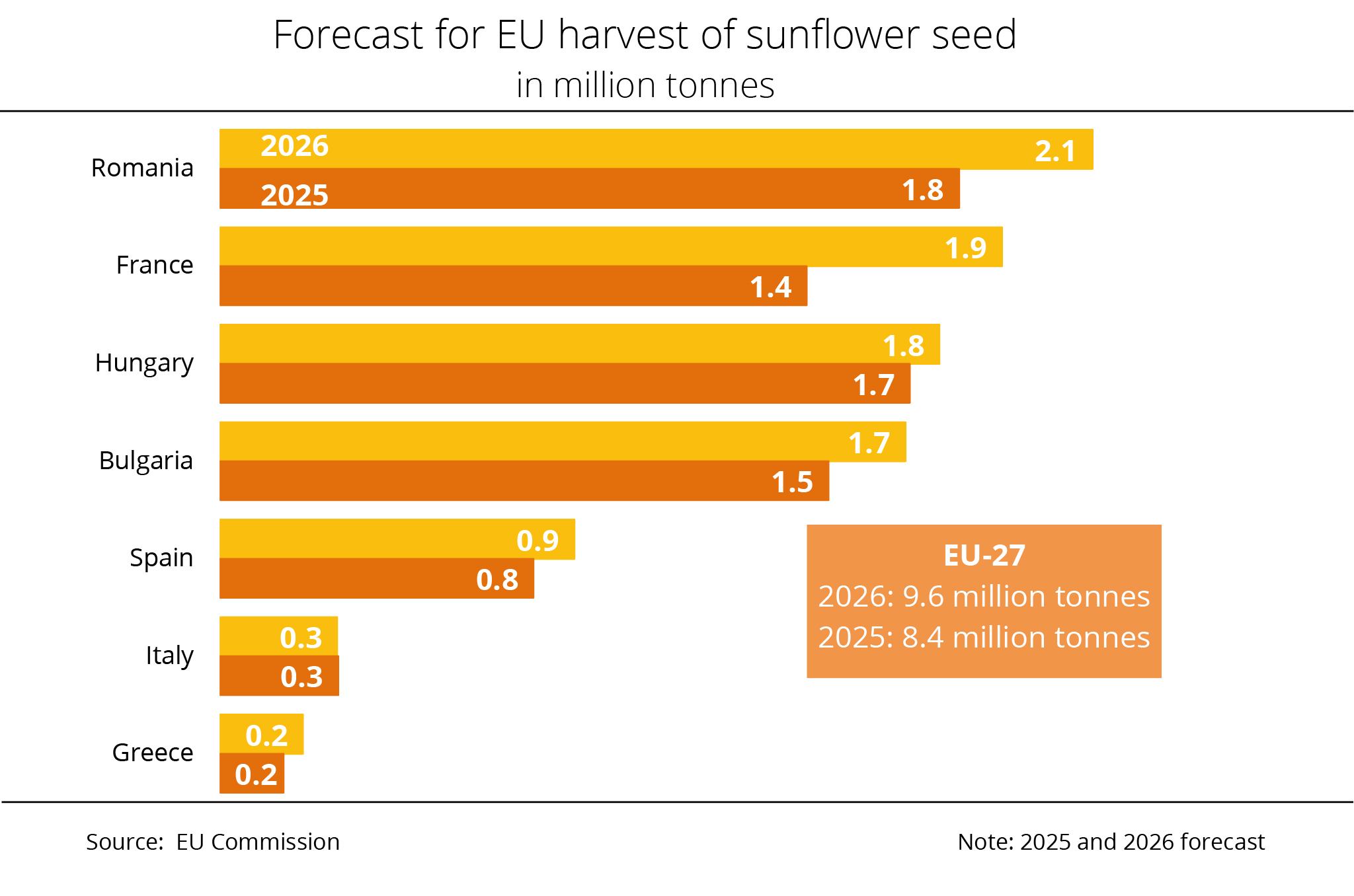

Chart of the week (16 2026)

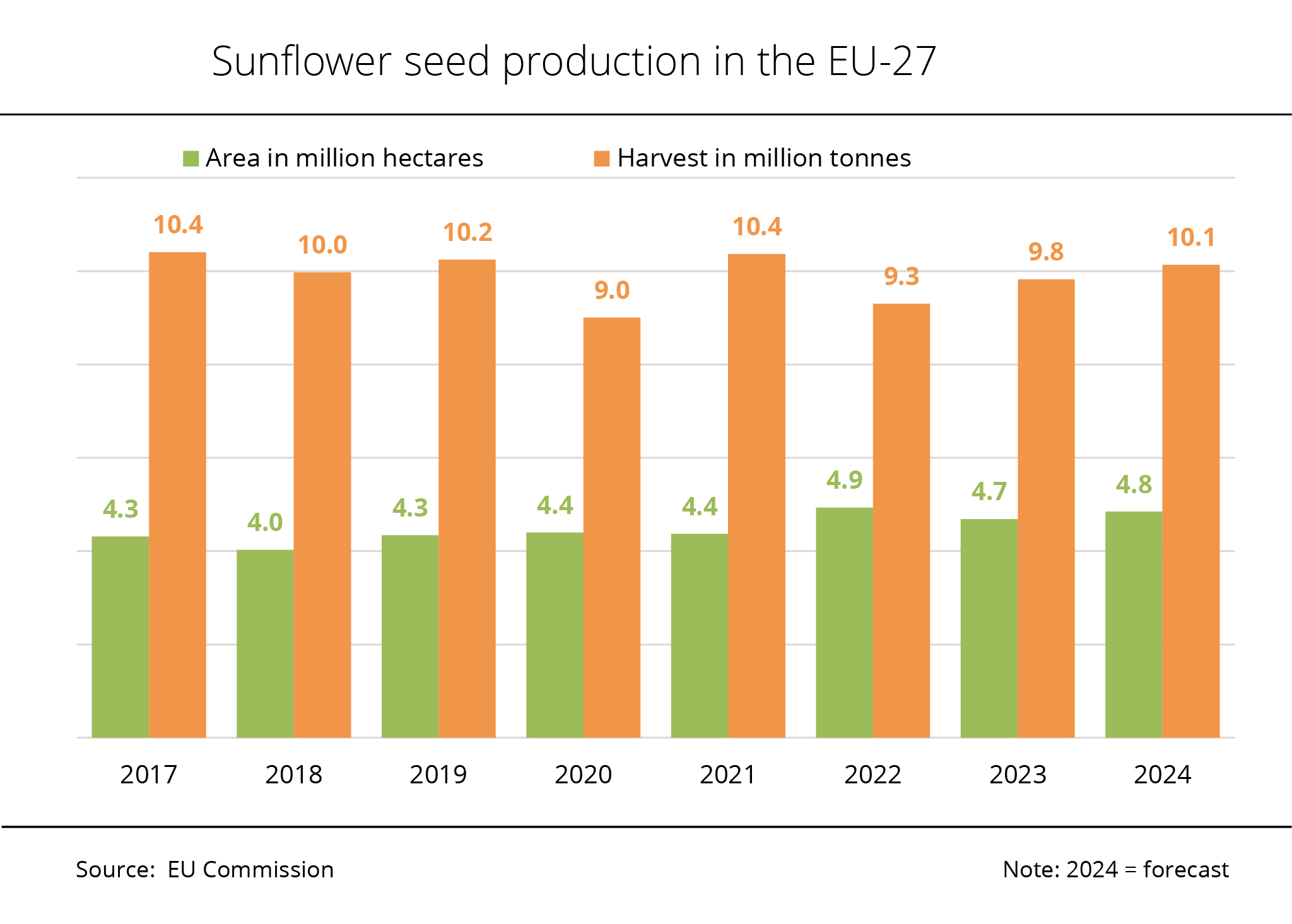

EU Commission forecasts a three-year high for sunflower seed

According to the EU Commission's latest forecast, the EU-27 is expecting a sunflower seed harvest of 9.6 million tonnes in 2026. This would be up approximately 1.2 million tonnes year-on-year and represent the largest harvest in three years. The expectation is mainly based on an approximately 5 per cent expansion in EU sunflower area. In particular, in Romania, France and Bulgaria, sunflower seed output is expected to increase significantly.

Romania is seen to strengthen its position as the largest EU producer. The country's harvest is expected to reach 2.1 million tonnes in 2026, representing an 18 per cent rise over 2025. The main factor driving the increase is a slight expansion in production area to 1.2 million hectares. Climbing to second place among the EU’s largest producers, France is expected to harvest 1.9 million tonnes, roughly 33 per cent more year-on-year.

According to research by Agrarmarkt Informations-Gesellschaft (mbH), other EU member states are also likely to see significant harvest increases, including Hungary, Bulgaria, Spain, and Greece. For Germany, the EU Commission projects an increase in output of approximately 32,000 tonnes to 175,000 tonnes. This would set a new record high. The crop area is estimated at 77,000 hectares, up from 62,000 hectares in the past year.

Compared with the major producers of sunflower seed, Germany continues to play a relatively minor role in the EU. However, the upward revision of the crop forecast reflects farmers' growing interest in diversifying crop rotation, especially by including an additional summer crop.

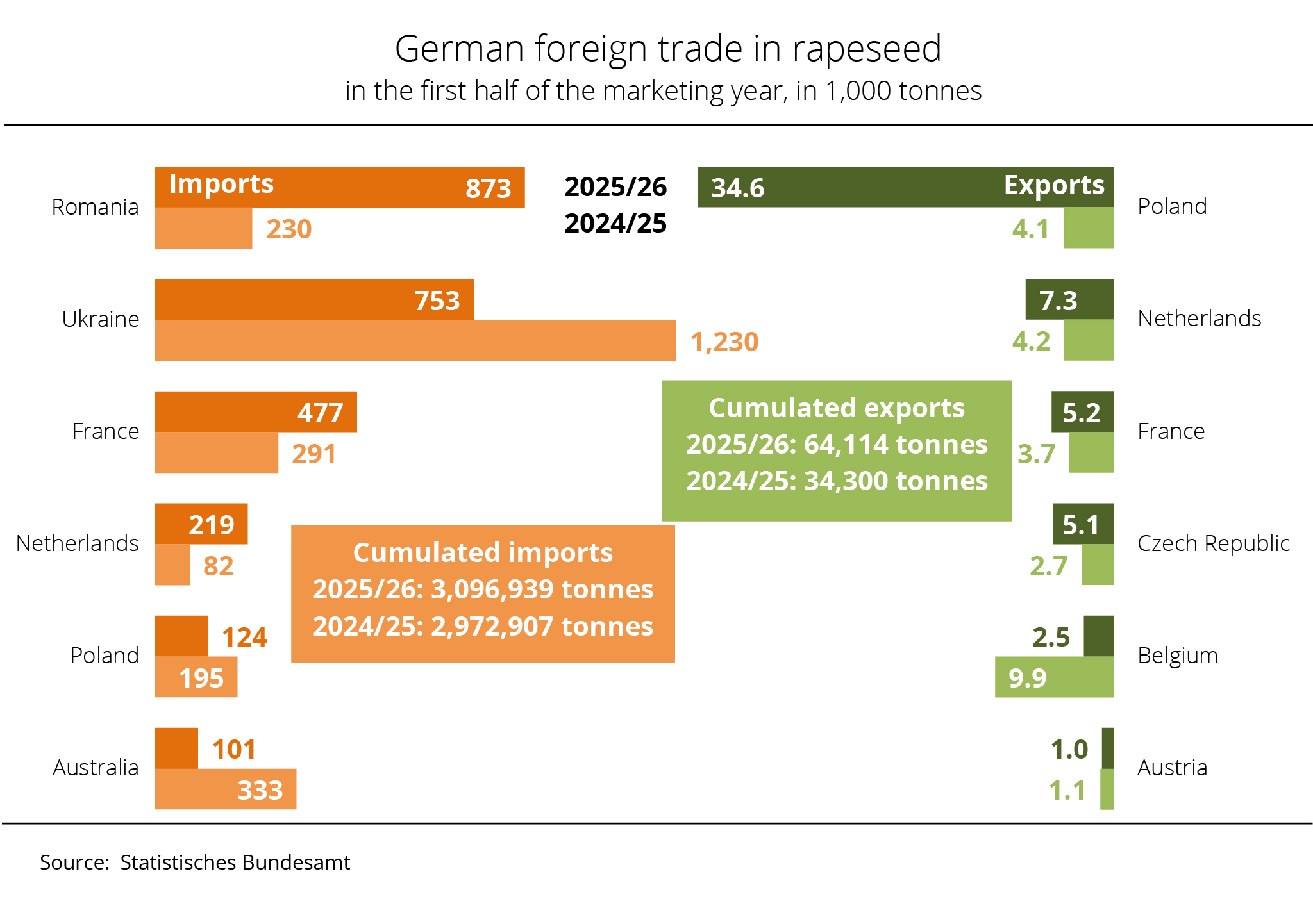

Chart of the week (15 2026)

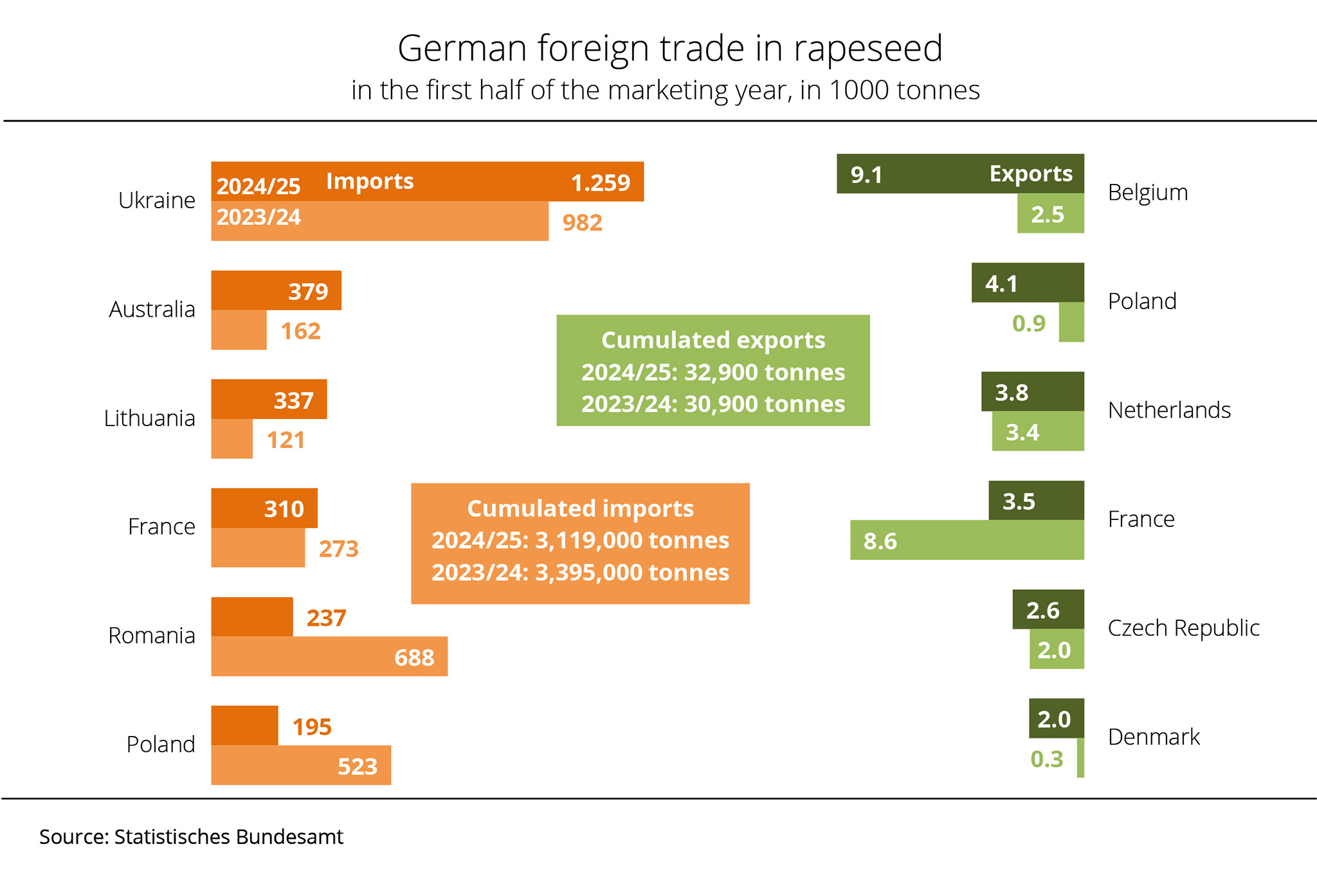

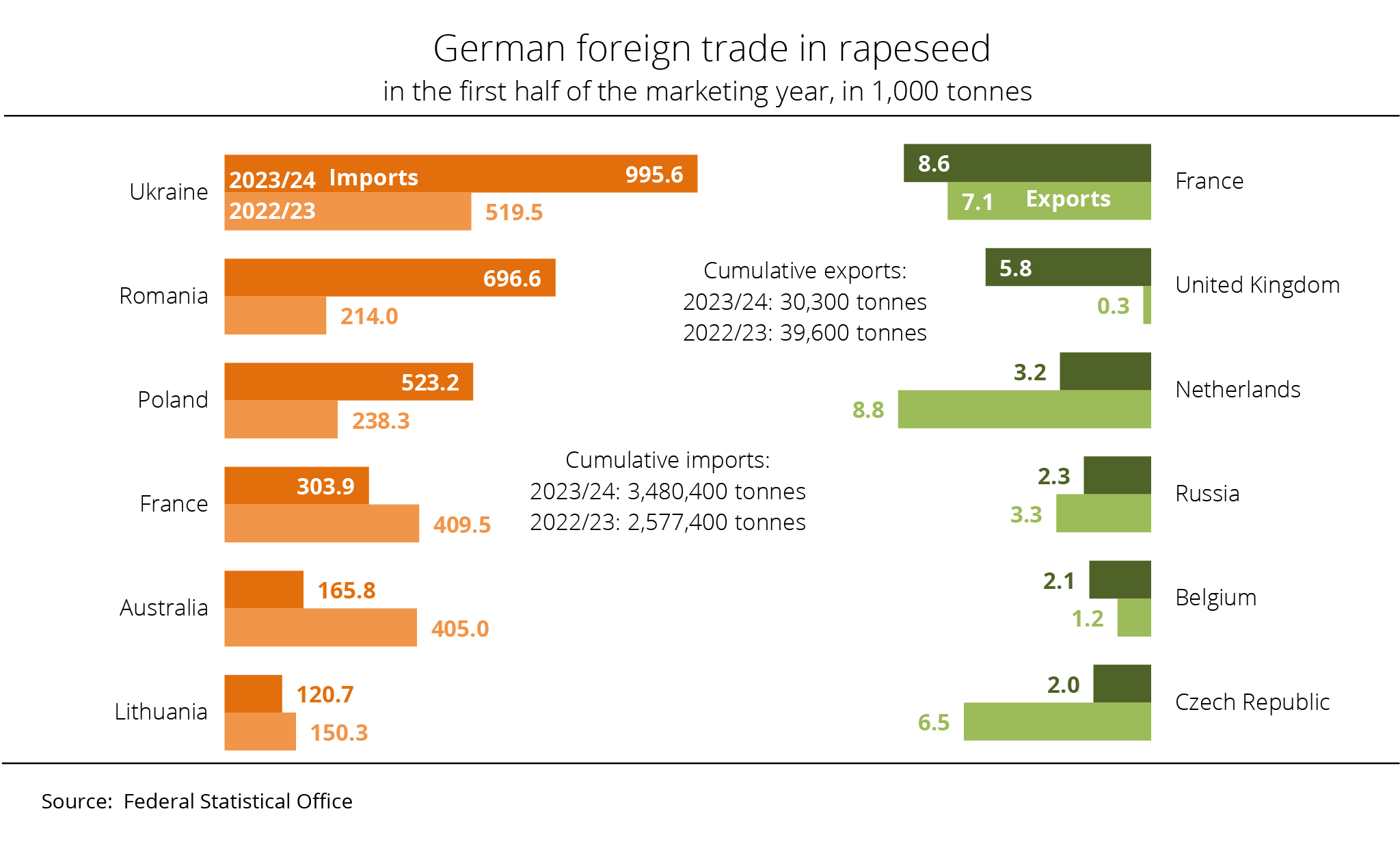

Brisk foreign trade in German rapeseed

German farmers harvested more rapeseed in 2025 than in 2024. Despite the larger domestic supply, rapeseed imports remained plentiful in the first half of the 2025/26 season. Exports also exceeded the previous year's volume.

According to data from the German Federal Statistical Office, Germany imported approximately 3.1 million tonnes of rapeseed in the first half of the 2025/26 crop year, representing a 4 per cent increase compared to the previous year. Delivering 873,400 tonnes, Romania replaced Ukraine as the leading supplier to Germany. By comparison, between July and December 2024, Romania delivered only 229,600 tonnes to the German market. The increase in imports was likely due to the significantly larger harvest, as Romania more than doubled its production compared to the previous year, reaching a new record high. However, it remains open to debate to what extent the country acted as transit route for Ukrainian rapeseed. According to data from the German Federal Statistical Office, Ukraine delivered roughly 752,500 tonnes, 39 per cent less than in the same period of the previous year. A possible reason for the decline in rapeseed imports could be Ukraine's export duties on rapeseed, soybean and sunflowers. These duties recently caused disruptions in European trade in these commodities.

France, Europe's third most important supplier, supplied 477,100 tonnes to the German market, according to research by Agrarmarkt Informations-Gesellschaft (mbH). This translates to an increase of roughly 64 per cent. The Netherlands, a central hub in world trade, more than doubled its volume. Whereas Canada did not deliver any significant volumes over the past two years, imports of Canadian rapeseed rose to 99,800 tonnes in the first half of the 2025/26 season (July to December 2025). By contrast, Germany's rapeseed imports from Poland, Australia, Lithuania, the Czech Republic and Belgium declined.

Germany is the largest net importer within the EU so that exports were relatively small despite the larger harvest. In the first six months of the current season, Germany exported only around 64,100 tonnes of rapeseed, which was up 87 per cent on the same period last year. Most German rapeseed exports go to other EU member states, with Poland (around 34,600 tonnes), the Netherlands (7,300 tonnes) and France (5,200 tonnes) as the primary destinations.

Chart of the week (14 2026)

EU legume harvest seen slightly lower

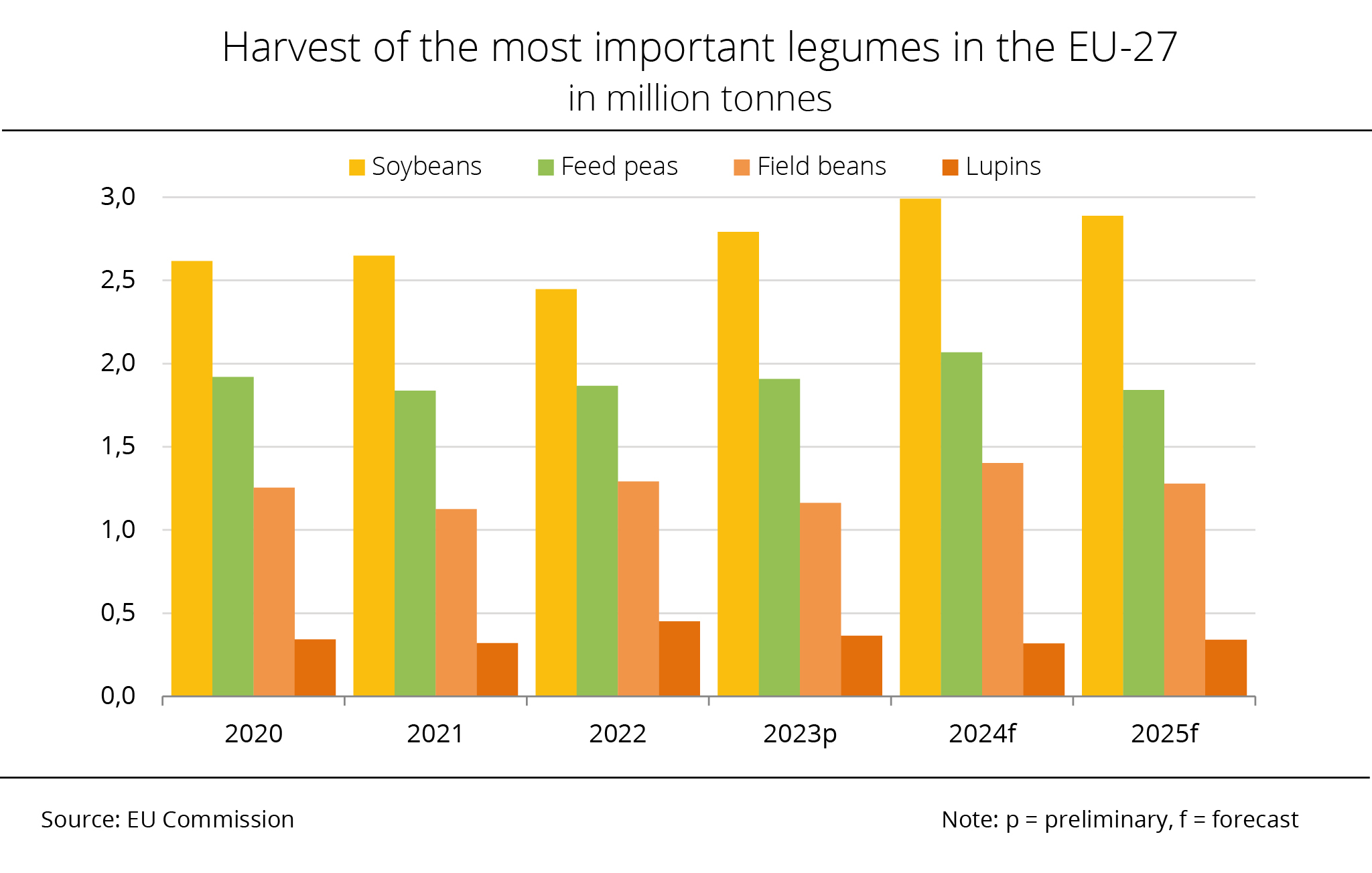

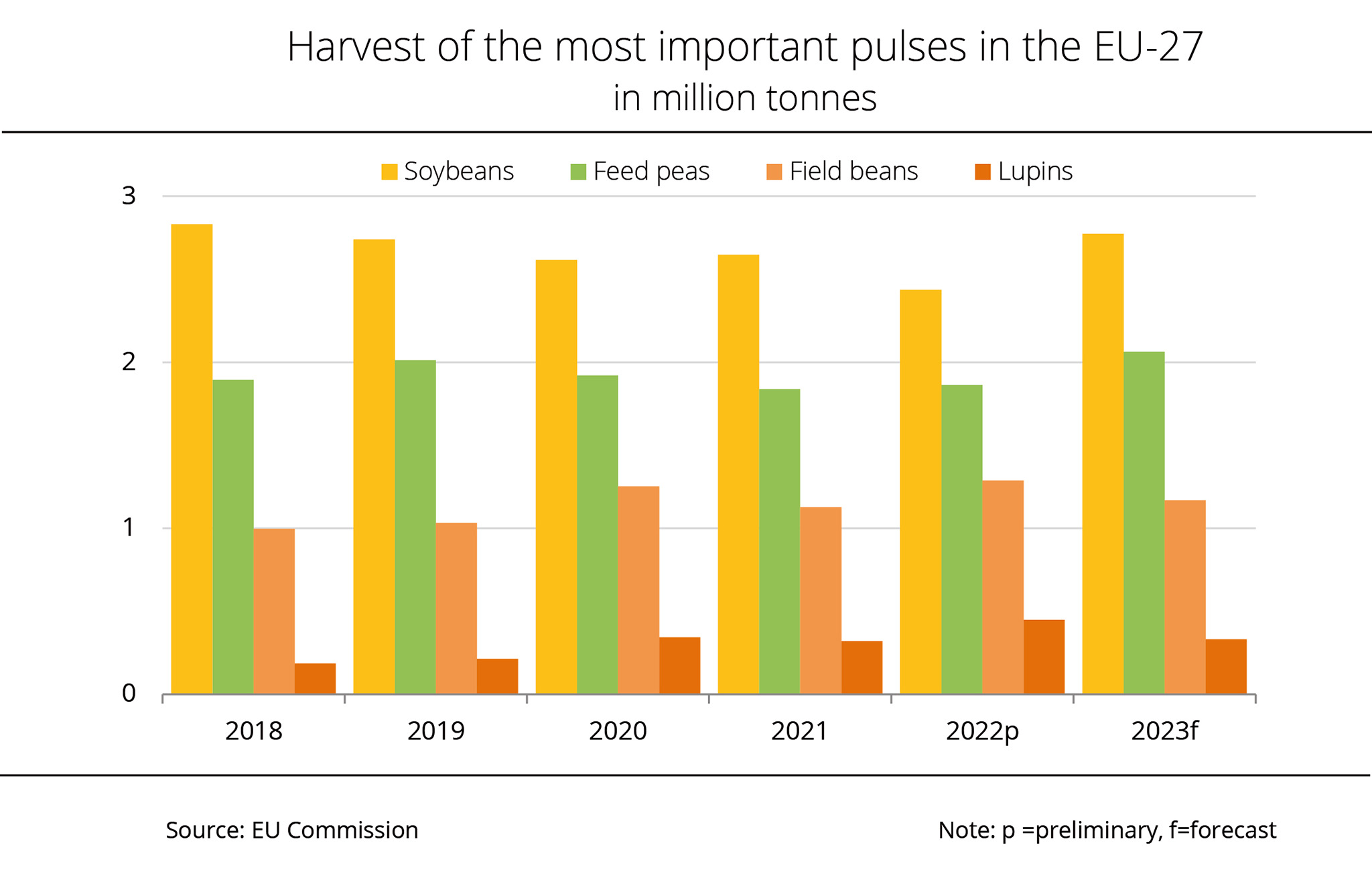

According to estimates by the European Commission, EU production of legumes for the 2026 harvest will fall by 1 per cent below the previous year's level. The harvest will nevertheless remain higher than average. Feed peas are expected to record the strongest decline.

In its estimate published at the end of March, the EU Commission expects the legume harvest in the EU to reach just over 7.0 million tonnes in 2026. This would translate to a 1 per cent decline year-on-year. According to Agrarmarkt Informations-Gesellschaft (mbH), the decline is primarily attributed to a slight reduction in legume area, while average yields have so far been projected at just above the previous year's level.

Feed peas are likely to record the sharpest decrease, with production expected to fall 6 per cent compared to the previous year, reaching 2.3 million tonnes. The broad bean harvest is expected to decrease around 3 per cent to 1.4 million tonnes. Soybean remains the most important legume in the EU, accounting for 40 per cent of the total legume crop. The harvest is projected at 2.8 million tonnes, representing a 2 per cent rise on the previous year due to an expansion in soybean area. Production of sweet lupins is expected to reach 486,000 tonnes, exceeding last year’s 417,000 tonnes and setting a new record.

The Union zur Förderung von Oel- und Proteinpflanzen e.V. (UFOP) regards the European Commission’s latest forecast as evidence that political support and the sustainable promotion of legume production should continue. The association has emphasised that, in individual farm planning, legumes, like any other crop, must compete with other market crops. This means that, farmers ultimately need to achieve not only good crop yields but also adequate economic returns. This requires reliable and transparent supply chains and contractual relationships. According to UFOP, the result should be added value that benefits all members of the supply chain and forms the basis for business continuity.

The association therefore welcomes the European Commission's announced intention to submit a European protein plan by the summer, aiming to reduce the EU’s dependence on protein imports. The plan will focus on plant-based protein sources, including legumes and oilseed crops. Significant impetus for the plan could also come from extending the Common Market Organisation (CMO) Regulation to include the protein crop sector. Such step would require Member States to recognise producer organisations in this sector and implement Operational Programmes (OPs). UFOP has emphasised the importance of introducing marketing and quality standards for protein crops to improve price transparency for producers.

1 and 2023, which was followed by a moderate recovery to 227 million slaughterings in 2025.

Chart of the week (13 2026)

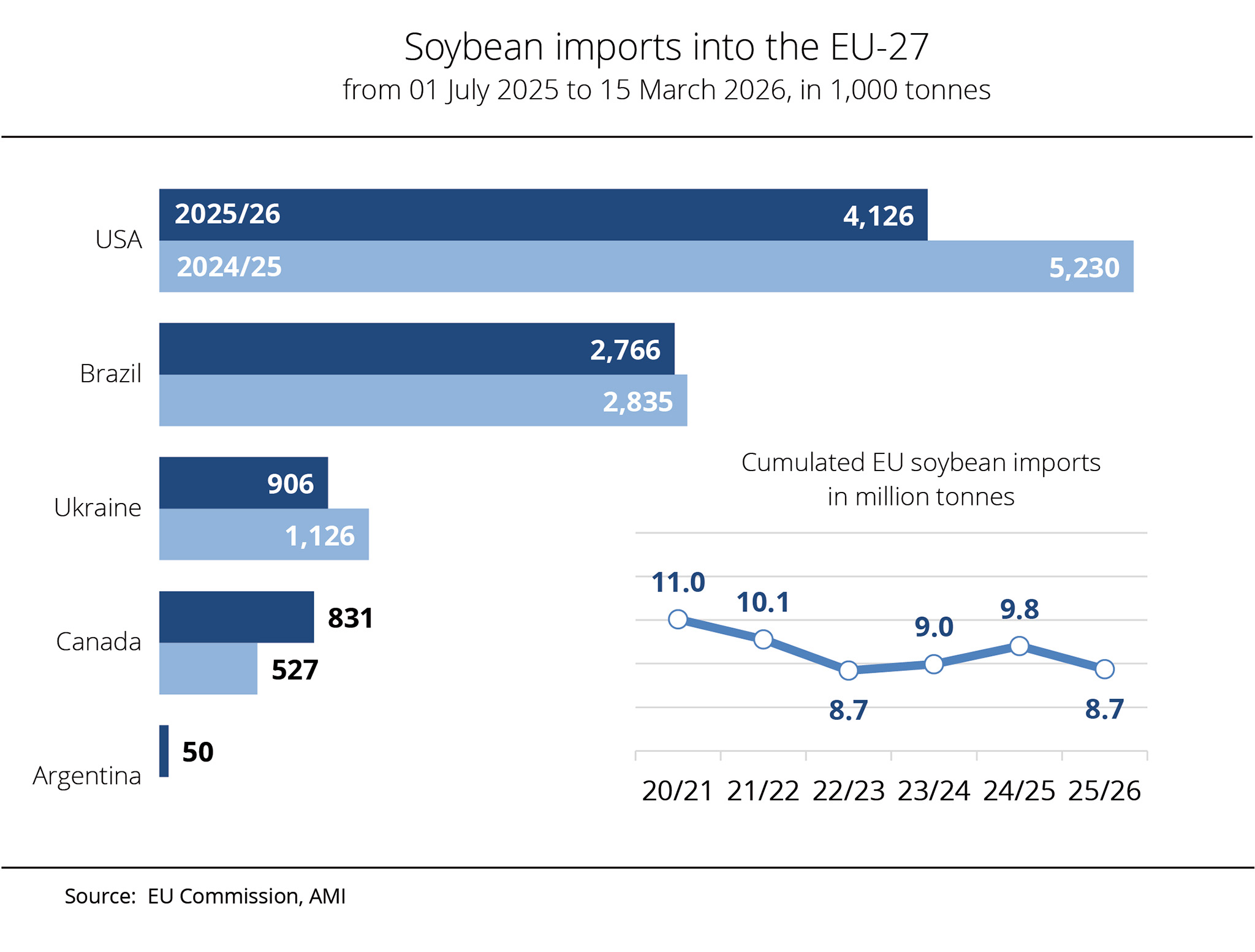

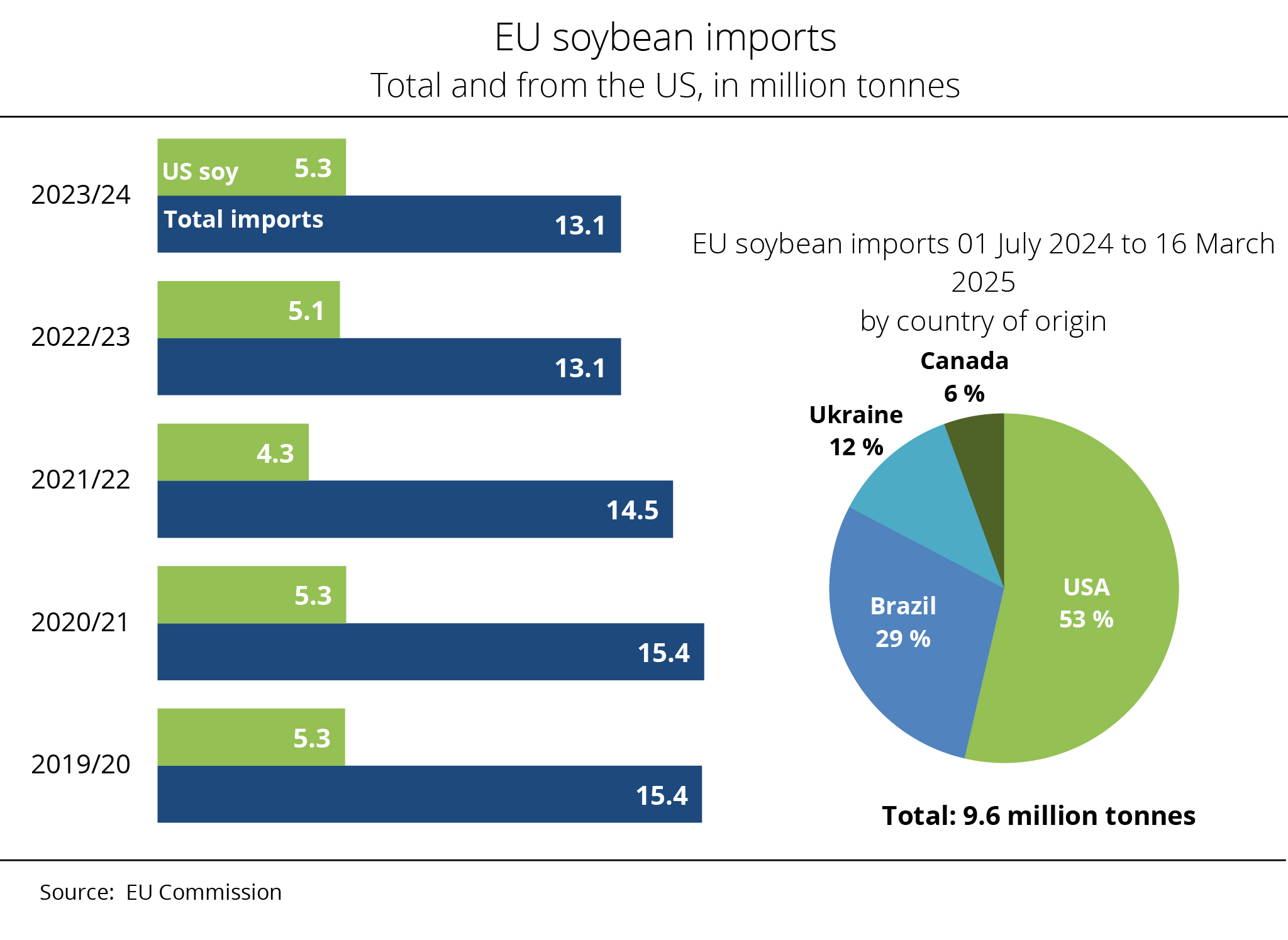

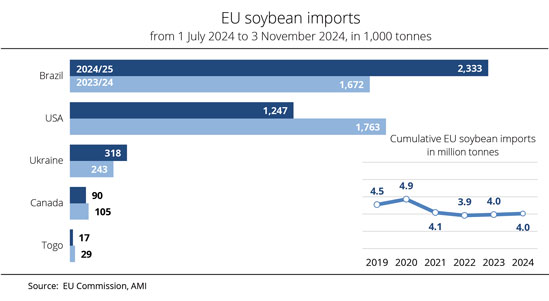

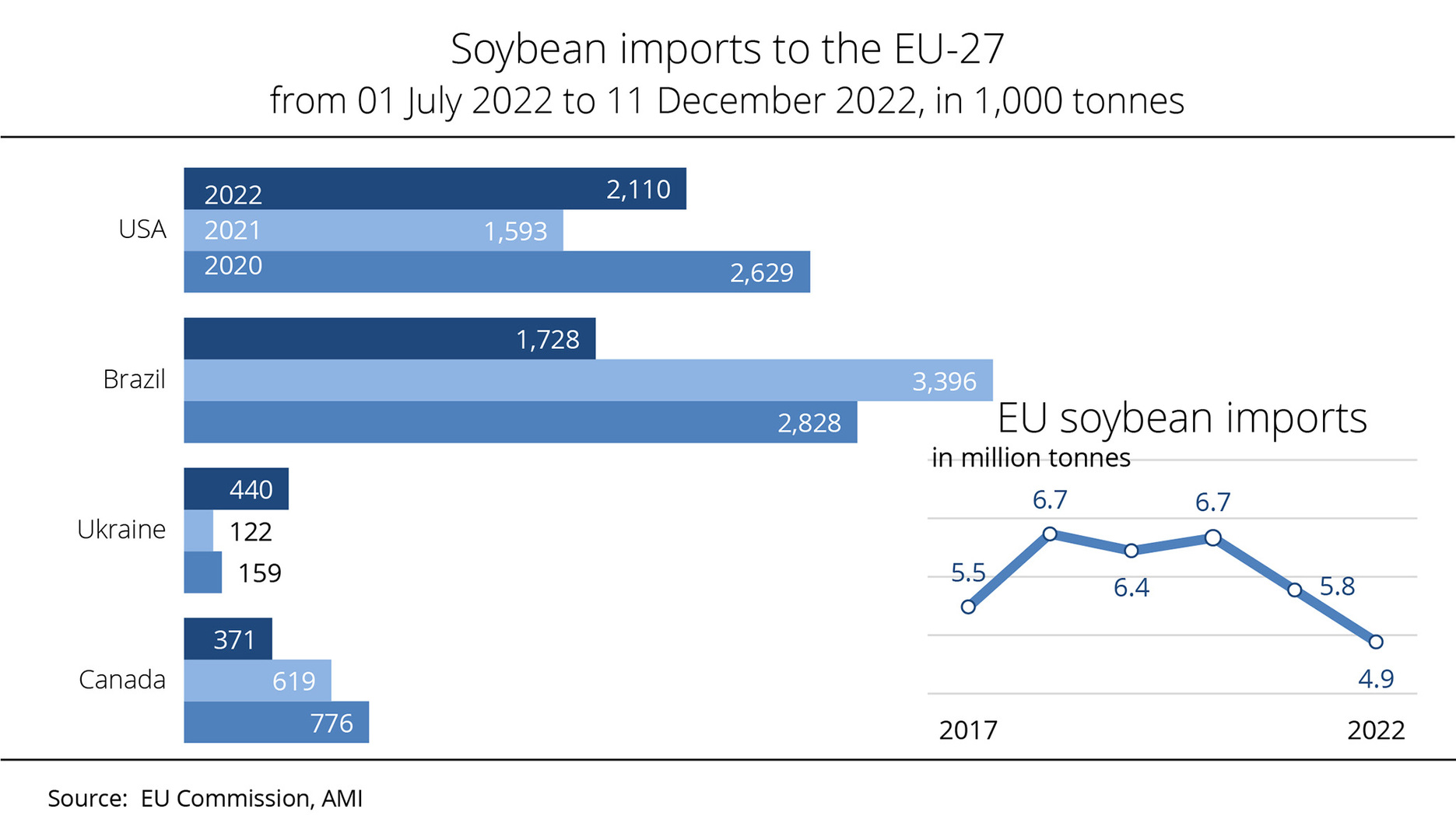

EU soybean imports declined – US remains main supplier

Soybeans are the most important oilseed crop imported into the European Union, ahead of rapeseed. Between July 2025 and mid-March 2026, the EU imported the lowest soybean volume in three years.

According to data from the European Commission, the European Union purchased just over 8.7 million tonnes of soybeans between 1 July 2025 and 15 March 2026, representing a drop of around 1.1 million tonnes compared to the same period in the 2024/25 season. The US and Brazil remain the most important supplier countries, although neither matched the previous year’s volumes. At 4.1 million tonnes, the EU received a significantly lower volume of soybeans from the US in the first eight and a half months of the current season compared to the year-earlier period (5.2 million tonnes). Consequently, the US share of total imports fell to approximately 47 per cent. Soybean shipments from Brazil, the second-largest supplier to the European market, dropped 2 per cent to approximately 2.7 million tonnes, accounting for just over 32 per cent of total imports.

During the same period, soybean imports from Ukraine into the EU declined roughly 19 per cent, falling to 905,900 tonnes. In contrast, deliveries from Canada increased notably, reaching 831,000 tonnes. This translates to a rise of roughly 58 per cent compared to the reference period of 2024/25. Argentina did not deliver any significant tonnages the previous year but, according to analysis by Agrarmarkt Informations‑Gesellschaft mbH (AMI), supplied around 50,100 tonnes to the EU market this year.

According to the Union zur Förderung von Oel- und Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP), the decline in soybean imports primarily reflects the drop in pig slaughterings in the EU from 250 million to 220 million between 2021 and 2023, which was followed by a moderate recovery to 227 million slaughterings in 2025.

Chart of the week (12 2026)

Argentina expects its biggest sunflower seed harvest in almost three decades

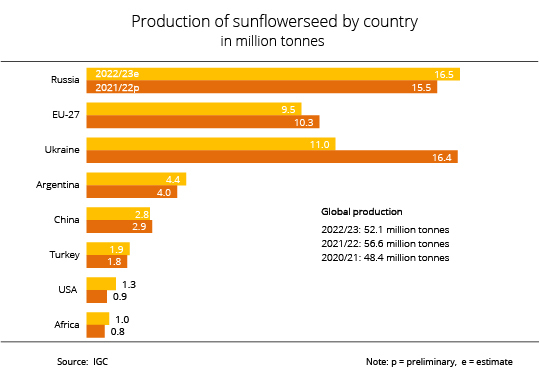

According to recent data from the US Department of Agriculture (USDA), global sunflower seed production will likely reach 54.1 million tonnes in the current marketing season. This figure is not only 2.1 million tonnes higher than previously expected but also far exceeds the previous year's level of nearly 52.1 million tonnes.

According to USDA data, the ongoing harvest in Argentina is projected to be around 1.5 million tonnes larger than had been expected in February, reaching 7.0 million tonnes. This would be the largest harvest in 28 years, mainly due to an expansion in the production area for the 2026 harvest at the expense of cotton, especially in northern Argentina. Harvest operations are currently in full swing and are expected to continue until April. Yields obtained so far have been encouraging. The USDA therefore revised its forecast upward by 0.3 decitonnes per hectare to 23.3 decitonnes per hectare, matching the previous year's result.

The USDA also revised its forecast for the Ukrainian harvest. According to research by Agrarmarkt Informations-Gesellschaft (mbH), the country's harvest is projected at 11.0 million tonnes, around 500,000 tonnes more than expected in February. This would nevertheless represent the smallest harvest in 12 years. The USDA further raised the crop outlook for Kazakhstan by 64,000 tonnes to 2.5 million tonnes, representing an increase of approximately 700,000 tonnes compared to 2024/25.

Chart of the week (11 2026)

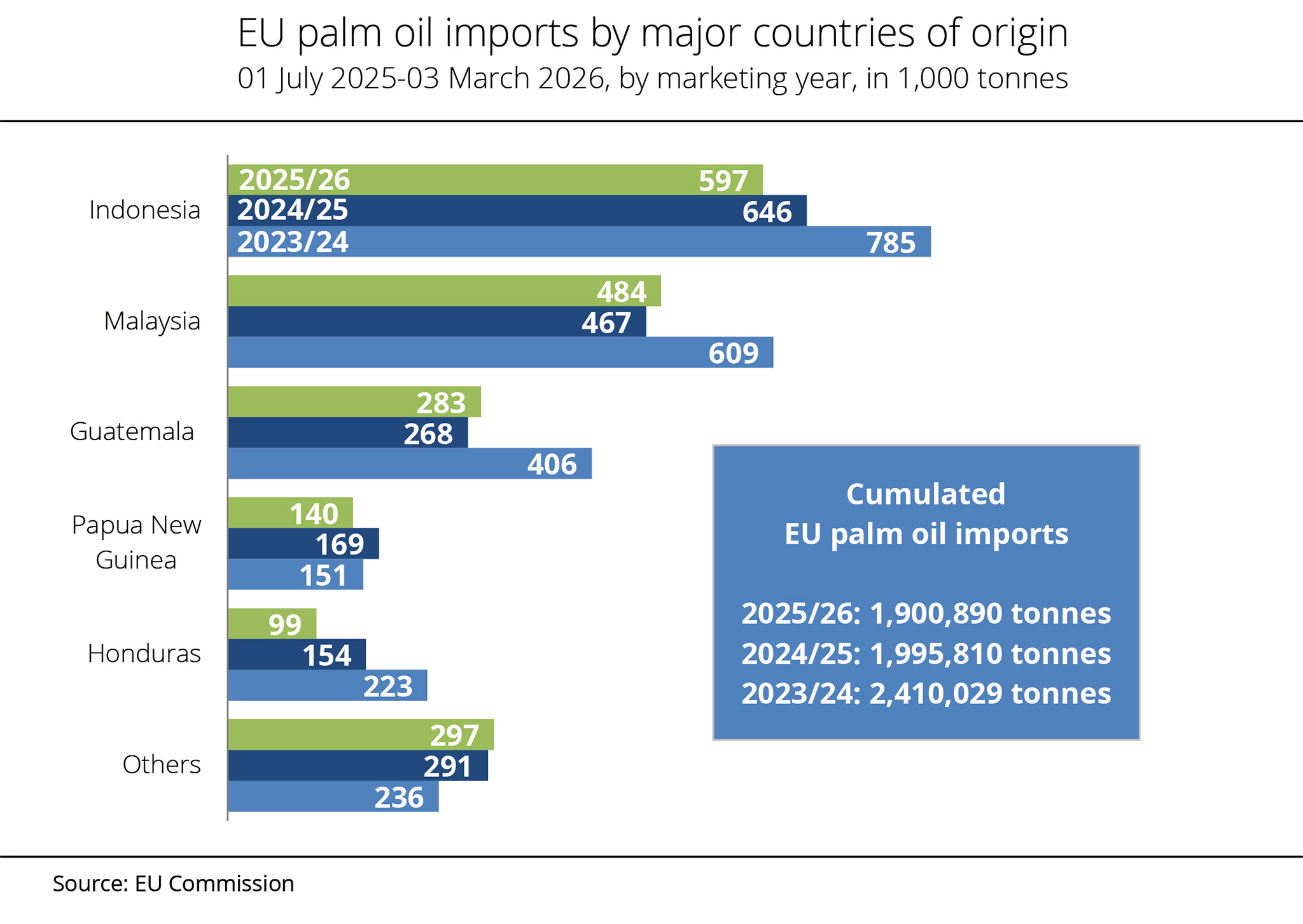

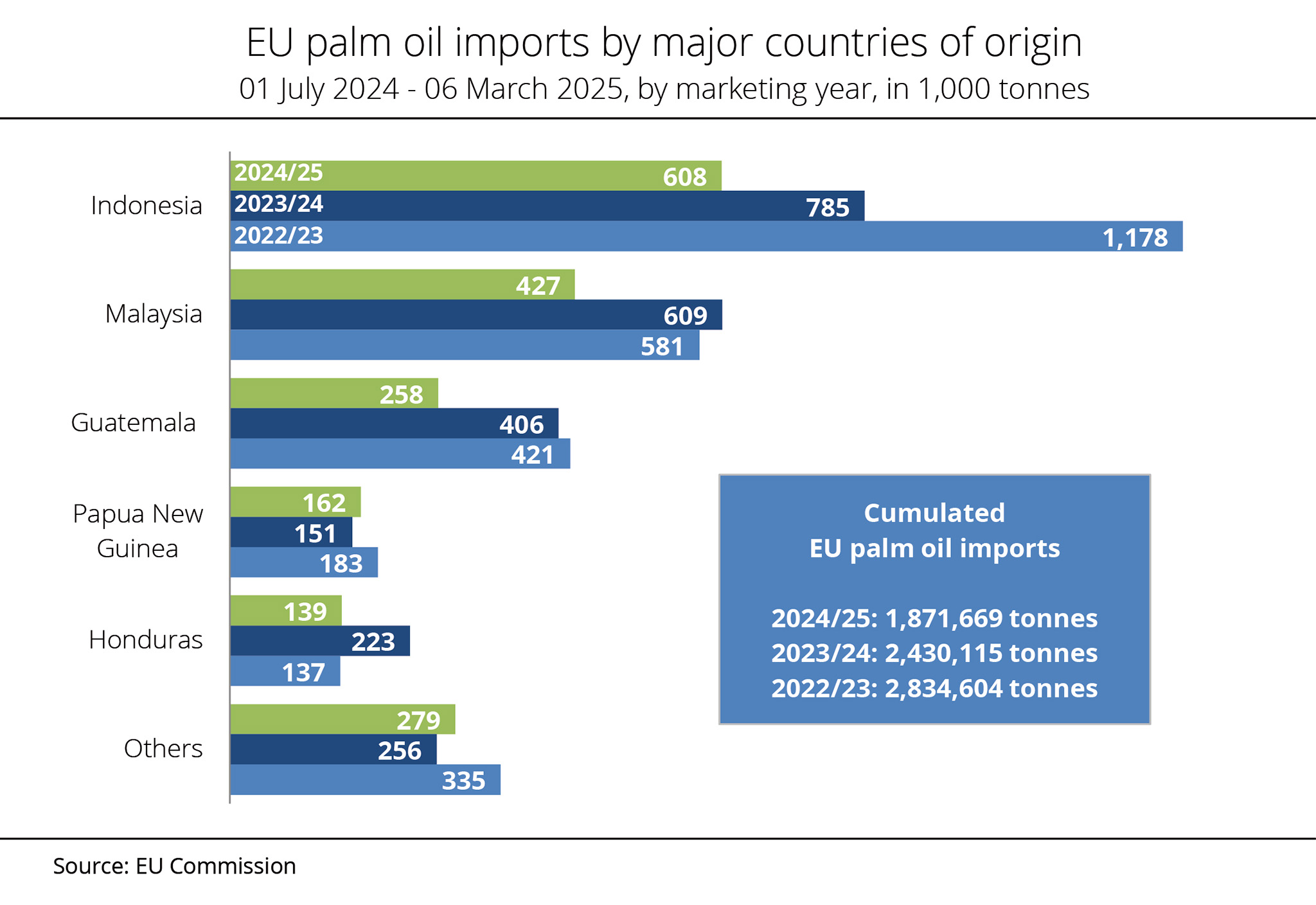

EU demand for palm oil continues to dwindle

The EU imported significantly less palm oil between July 2025 and early March 2026 than in the same period a year earlier, reflecting an overall decline in intra-Community consumption. The Union zur Förderung von Oel- und Proteinpflanzen (UFOP) attributes this to the exclusion of palm oil-based biofuels from being credited towards national quota obligations, which is planned for 2030 and has already been implemented by some member states. However, UFOP has warned that such regulation could be undermined by imports of POME (Palm Oil Mill Effluent).

The decline in palm oil imports into the EU continues the past years' trend that was triggered by the decision to exclude palm oil-based biofuels from being credited towards national quota obligations from 2030 onwards. Some EU member states have already ended the crediting ahead of time, reinforcing the trend. UFOP has warned that this trend should not be undermined by imports of palm oil effluent (POME). POME is obtained as a by-product of palm oil production. UFOP therefore welcomes the EU Commission's current draft of an implementing regulation with clearly specified testing requirements for POME as part of comprehensive on-site inspections. According to the association, this is an essential step towards fraud prevention.

According to the latest data from the EU Commission, the European Union received a total of 1.9 million tonnes of palm oil from abroad between 1 July 2025 and 3 March 2026, which represents a slight decrease from the nearly 2.0 million tonnes received in the same period the previous year.

Between July 2023 and March 2024, EU palm oil imports had still totalled around 2.4 million tonnes.

Indonesia remains the leading supplier, with 597,400 tonnes. However, the country's deliveries between July and early March dropped 8 per cent year-on-year. In contrast, imports from Malaysia, the second largest supplier, rose around 4 per cent to 484,000 tonnes. Guatemala's deliveries to the EU market also increased roughly 5 per cent, reaching 282,800 tonnes. According to research by Agrarmarkt Informations-Gesellschaft (mbH), Papua New Guinea supplied almost 17 per cent less, amounting to 140,100 tonnes. The drop in shipments from Honduras was even sharper, with a reduction of around 36 per cent year-on-year.

Chart of the week (10 2026)

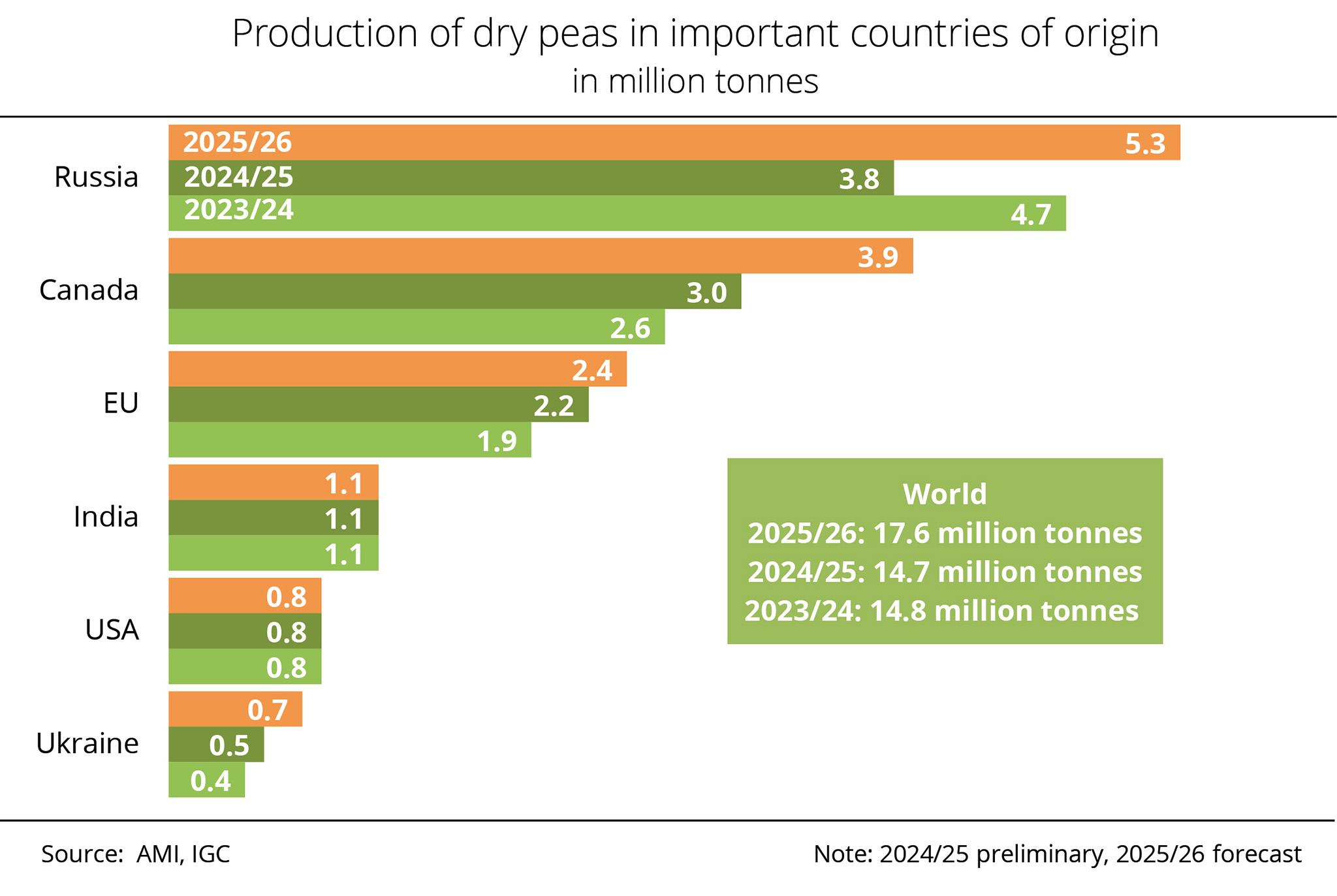

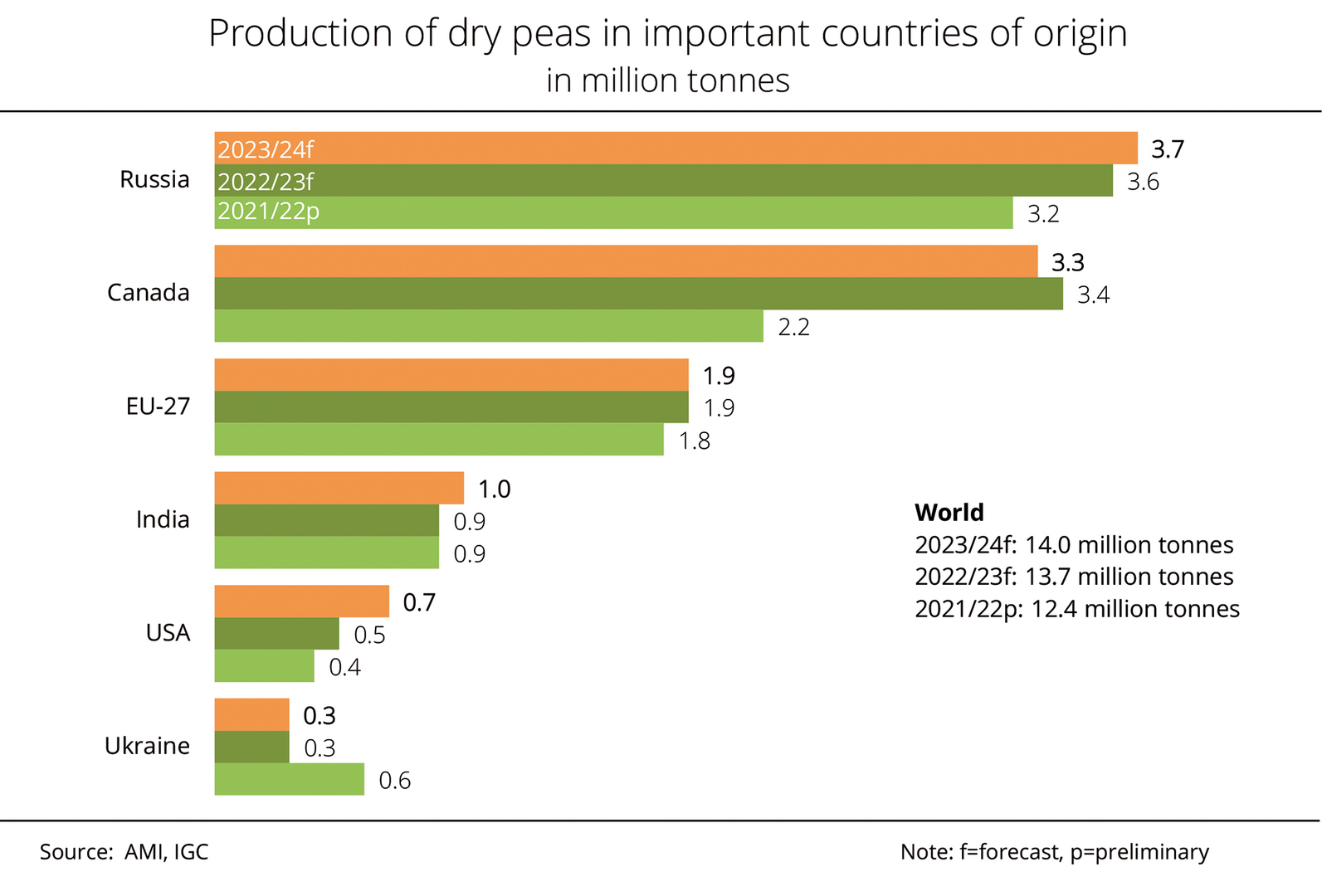

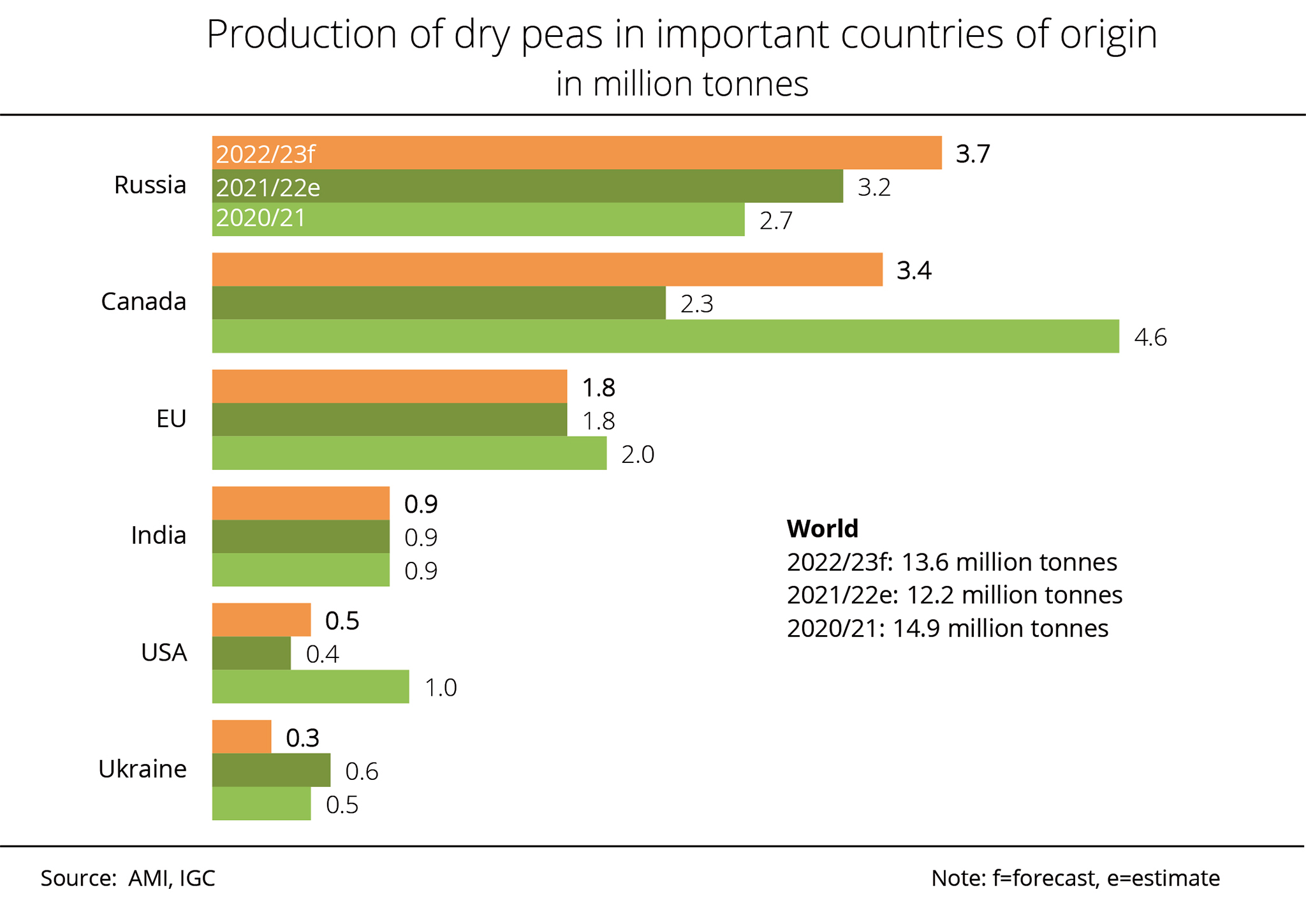

International Grains Council (IGC) forecasts record year for dry peas in 2025/26

Based on an expansion of the crop area and yield increases, global dry pea production is expected to reach a new record level of 17.6 million tonnes in the current season. This translates to a year-on-year increase of just under 20 per cent. Against this background, the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) has renewed its call for the German government to finally present the comprehensive and ambitious national protein strategy it has announced. The association has stated that human and animal nutrition are key drivers for promoting and advancing the sustainability and resilience of crop rotation systems through the cultivation of pulse crops, warning that yet another sowing year must not be missed.

According to estimates by the International Grains Council (IGC), dry pea production in Russia, the world's largest producer of this crop, jumped almost 40 per cent to a record 5.3 million tonnes in 2025, despite a reduction in area planted. According to investigations conducted by Agrarmarkt Informations-Gesellschaft mbH, the increase is mainly due to very high yields. The IGC projects Canada's marketable crop at 3.9 million tonnes, which is up one third compared to 2024/25. The rise is due to an 8 per cent expansion in production area, especially in the province of Alberta. In addition, favourable weather conditions in Saskatchewan and Alberta helped boost yields.

The 2025 harvest in the EU, the third most important global dry pea producer, is estimated at 2.4 million tonnes, with yield increases offsetting the decline in production area. In Germany, France and Lithuania in particular, farms recorded more than satisfactory results.

The UFOP is convinced that the yield potential for improving the competitive position of pulses in crop rotations is far from being fully exploited. The association has stressed the need for a holistic strategy that not only aims to expand cultivation as a fundamental goal but also provides stronger and more reliable support for product development and sales promotion. The UFOP has explained that, in economic terms, sustainability means that rising demand "pulls" the crop area. In view of the expected strategy of the Federal Ministry of Agriculture, the UFOP has emphasised the significant need to take into account research and innovation across the entire supply chain, starting with breeding, adding that it expects the Ministry to address this need.

Chart of the week (09 2026)

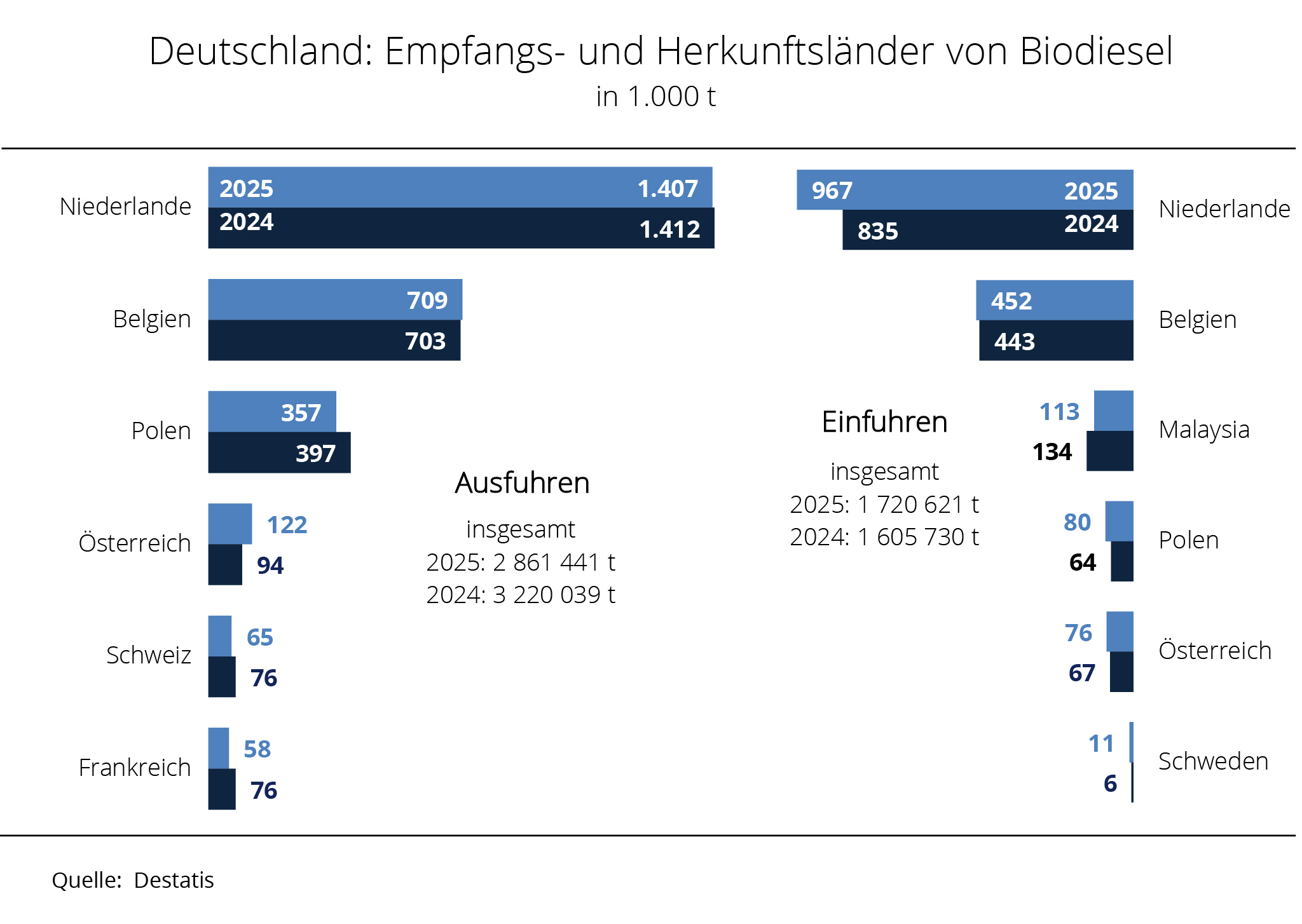

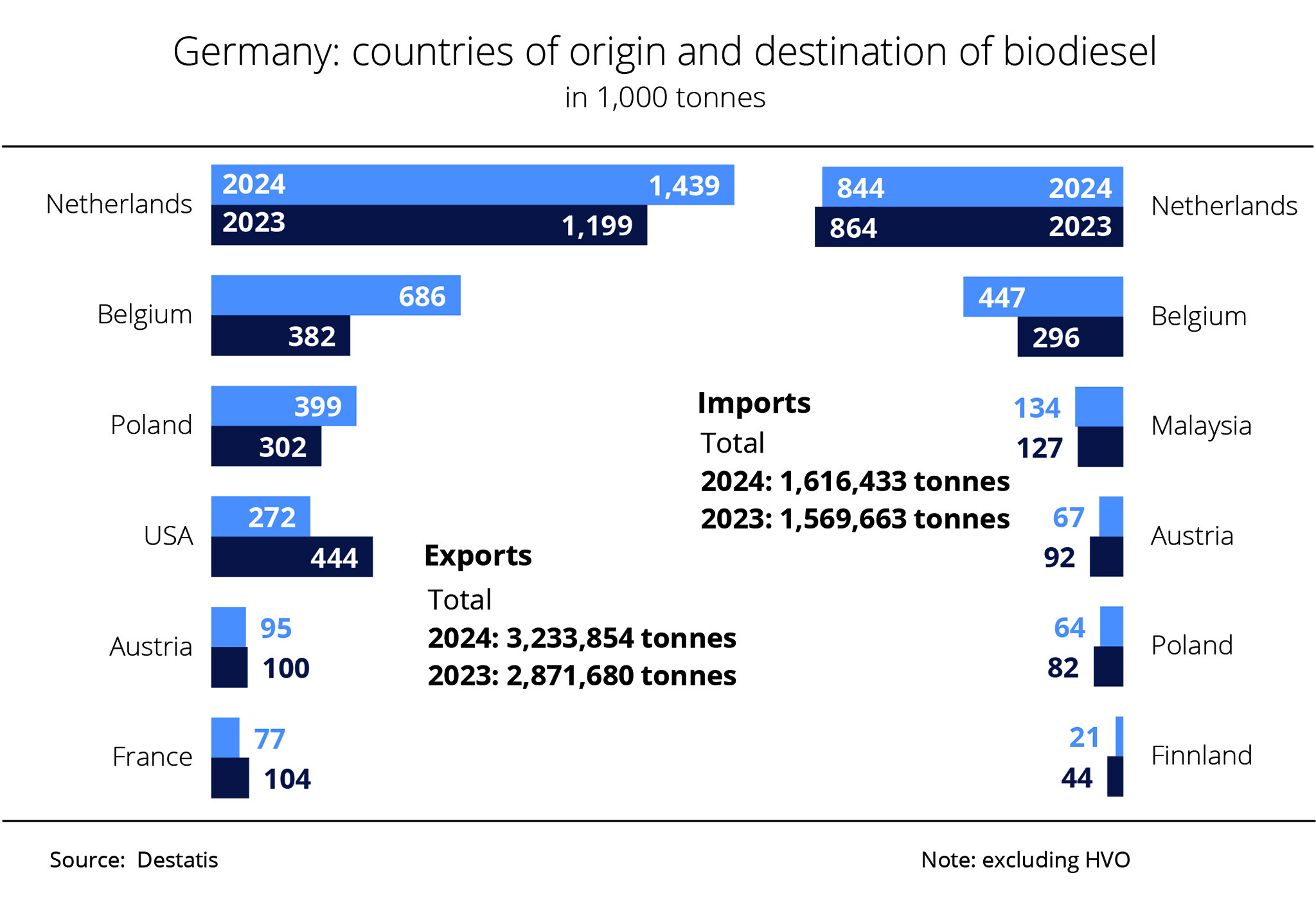

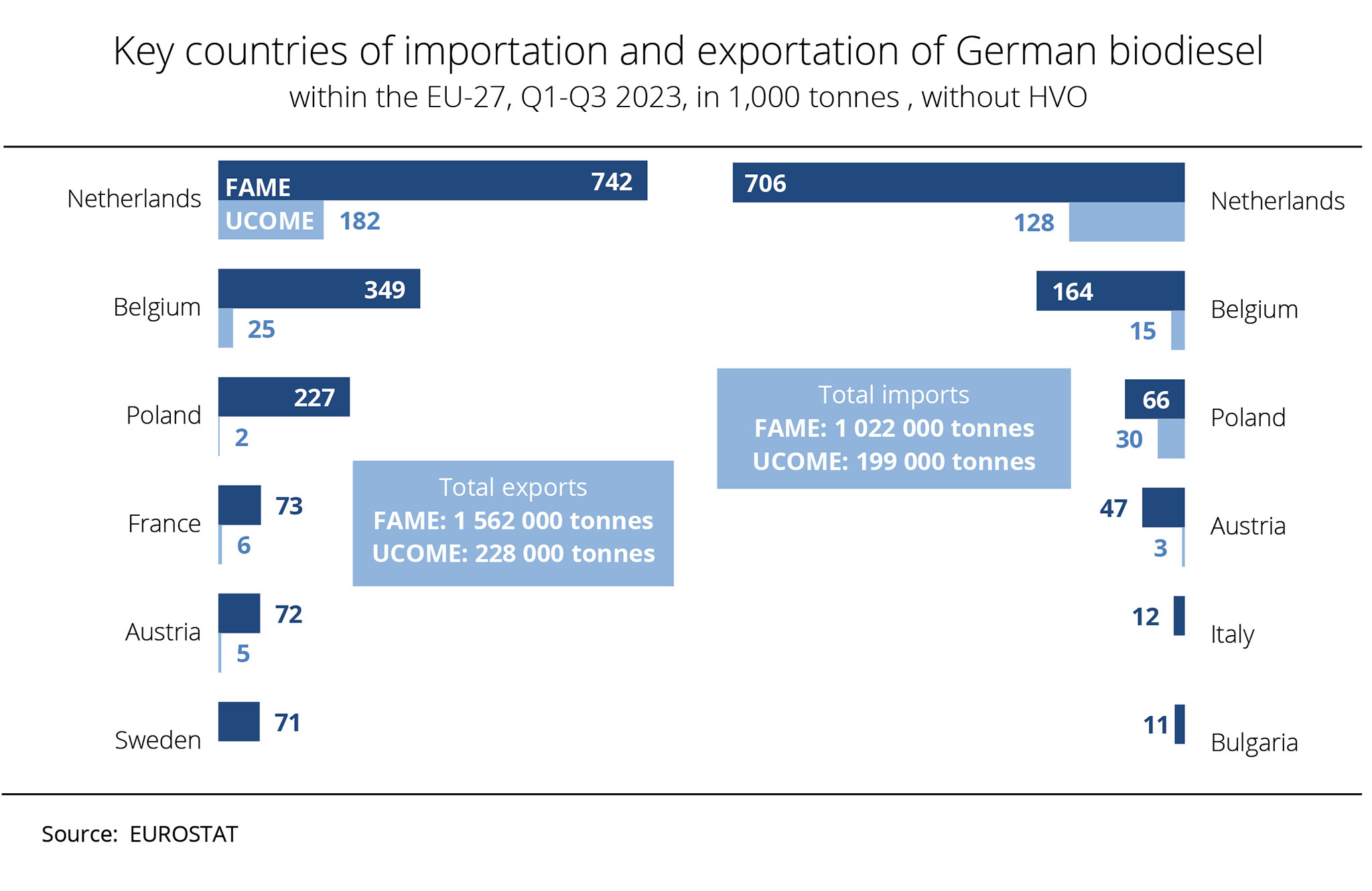

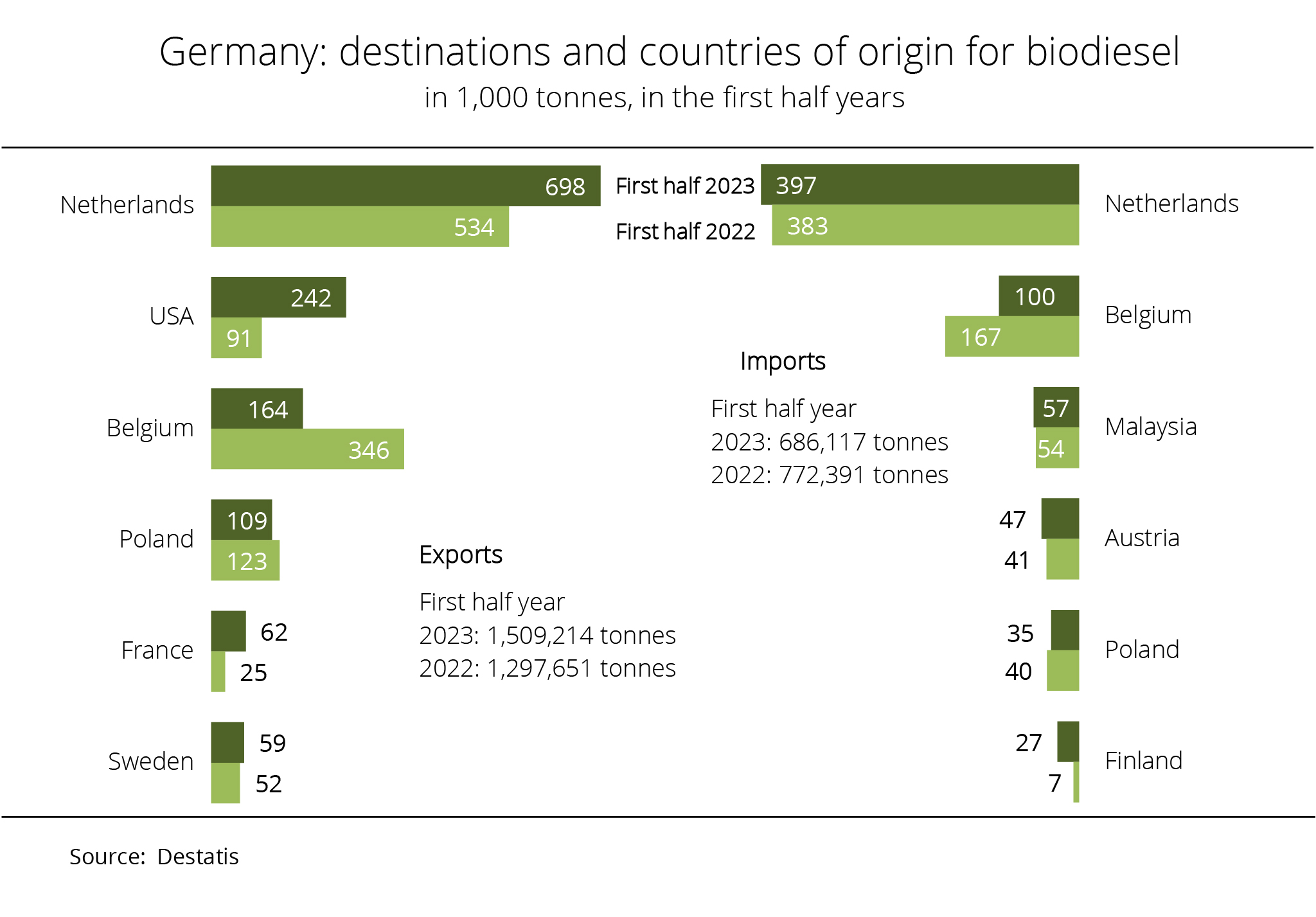

Germany's biodiesel exports in decline

According to data from the German Federal Statistical Office, exports of biodiesel from Germany declined around 11 per cent from the previous year's record volume of 3.22 million tonnes, reaching 2.90 million tonnes in 2025. Net exports decreased 0.47 million tonnes to 1.14 million tonnes. The Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) has contended that these exports mean that potential for climate change mitigation in the transport sector is also exported, and has called for adjustments to be made during the ongoing parliamentary process on greenhouse gas reduction quota legislation.

The Netherlands remained by far Germany's most important trading partner, with Rotterdam serving as the central hub in the international trade of biofuels. Delivery volumes remained largely unchanged at 1.4 million tonnes. The same applies to deliveries to Belgium. At 708,700 tonnes and with a 1 per cent year-on-year increase, Belgium ranks second among the most important markets for biodiesel from Germany. Austria received 121,700 tonnes of German biodiesel, representing an increase of roughly 29 per cent. In contrast, exports to Poland dropped 10 per cent to 356,700 tonnes. Exports to Switzerland, France, Latvia, Sweden and other EU countries also declined.

The picture is slightly different for imports. According to investigations by Agrarmarkt Informations-Gesellschaft mbH, Germany sourced approximately 1.7 million tonnes of biodiesel from abroad, which was up nearly 7 per cent compared to 2024. The largest volumes came from the Netherlands, Belgium, Malaysia and Poland. Notably, imports from Poland rose approximately 25 per cent to 80,100 tonnes. By contrast, imports from Malaysia decreased just less than 16 per cent.

In view of the deliberations on the further increase of the GHG reduction quota in the German Bundestag, the UFOP has called for raising the cap on biofuels from cultivated biomass from 4.4 per cent to 5.8 per cent, the level permitted under EU law. According to the UFOP, export volumes, which are fluctuating at a high level in absolute terms, constitute a reserve to meet the greenhouse gas quota obligation provided for in the draft bill. The quota is due to rise to 59 per cent by 2040. The association has emphasised that this potential could also be utilised for the mitigation of national climate change instead of selling this biodiesel on the EU market through pricing.

The UFOP has also called for the 17.5 per cent GHG quota obligation that is scheduled for 2028 to be brought forward to 2027 and for it to be raised to 19.5 per cent in 2028 to stabilise GHG quota prices, as this measure would prevent the sharp jump to 21 per cent in 2029 currently proposed in the draft bill.

Chart of the week (08 2026)

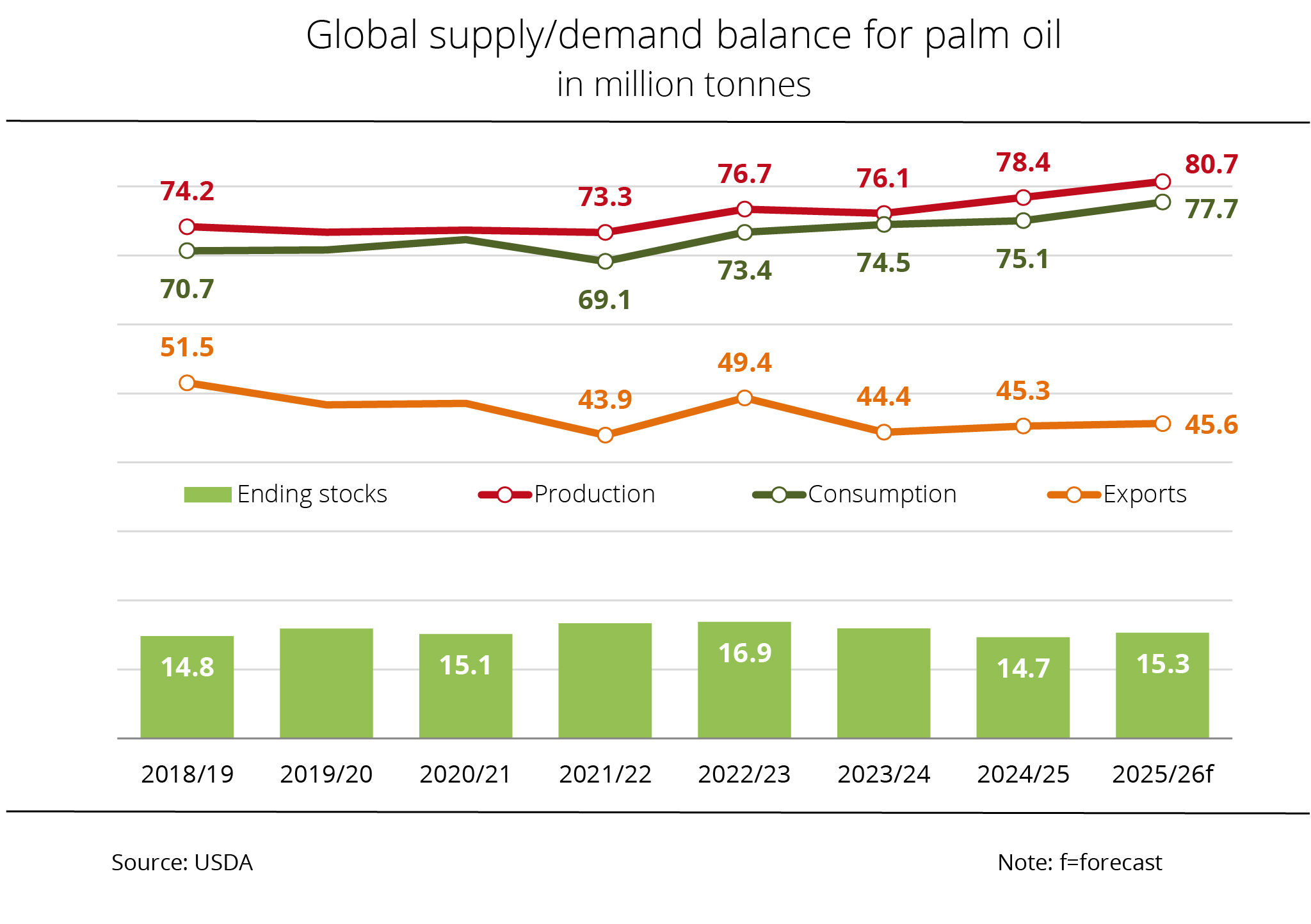

Palm oil production set to hit record levels

According to recent information from the US Department of Agriculture (USDA), global palm oil production in 2025/26 is set to rise to a record high of 80.7 million tonnes, exceeding the previous year's level by 3 per cent.

The primary reason for this forecast is anticipated production increases in Malaysia and Indonesia. Although Malaysian production is seasonally strongly curbed, the USDA currently projects output at 20.2 million tonnes, which would be up 820,000 tonnes year on year. Indonesia is expected to increase its production by 1.2 million tonnes to 46.7 million tonnes compared to the previous year.

Trade in palm oil has also increased over recent years. Around 45.6 million tonnes will likely be shipped across the world's oceans in 2025/26. According to Agrarmarkt Informations-Gesellschaft (mbH), this quantity exceeds the previous year's volume of 45.3 million tonnes by just under 1 per cent.

Global consumption is expected to rise around 4 per cent compared to the past season, reaching 77.7 million tonnes, and is likely to be fully met by global production this season. Against this background, an increase in ending stocks is to be expected. By the end of the marketing season, stocks are likely to grow just over 4 per cent to approximately 15.3 million tonnes.

Chart of the week (07 2026)

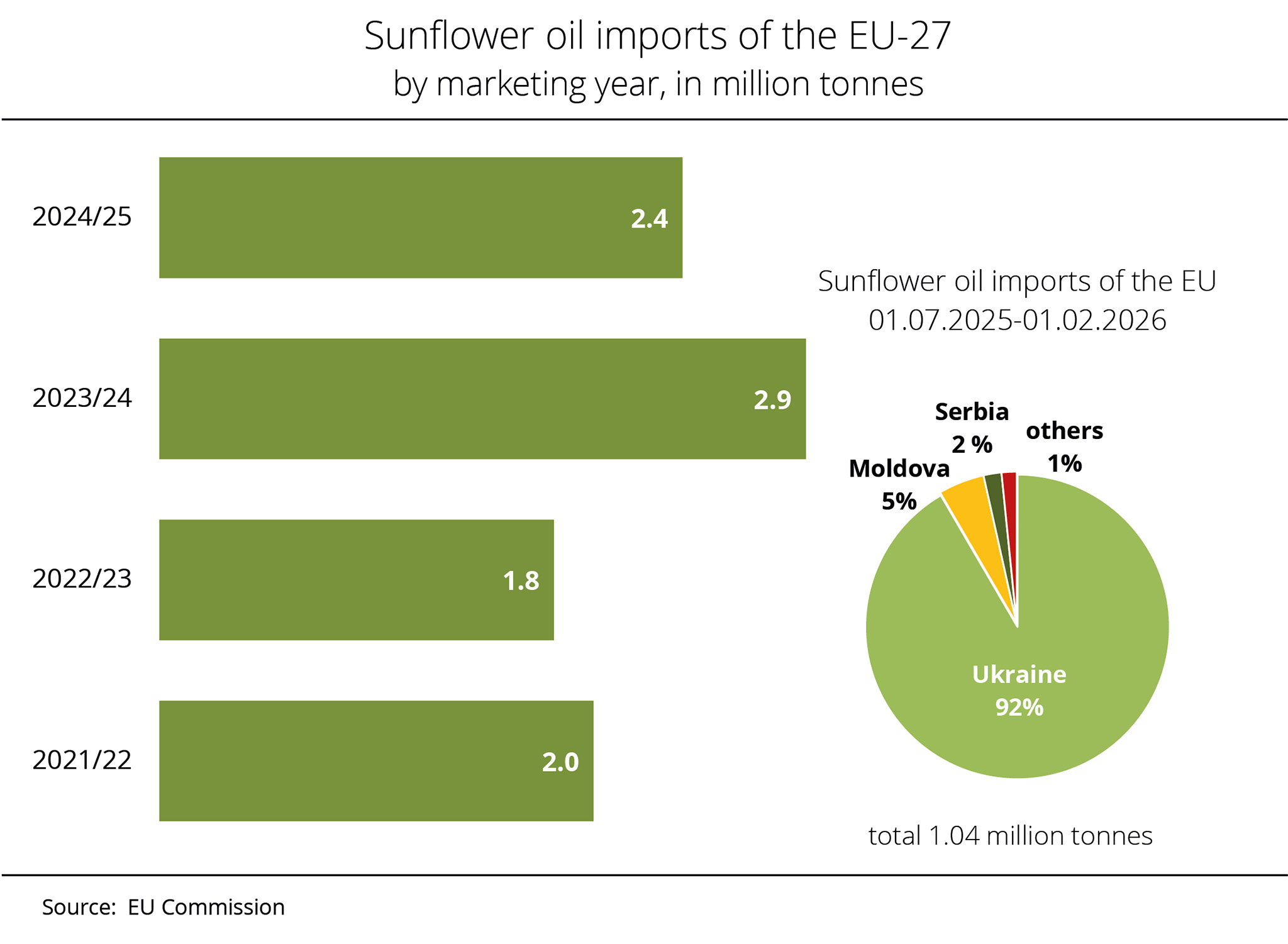

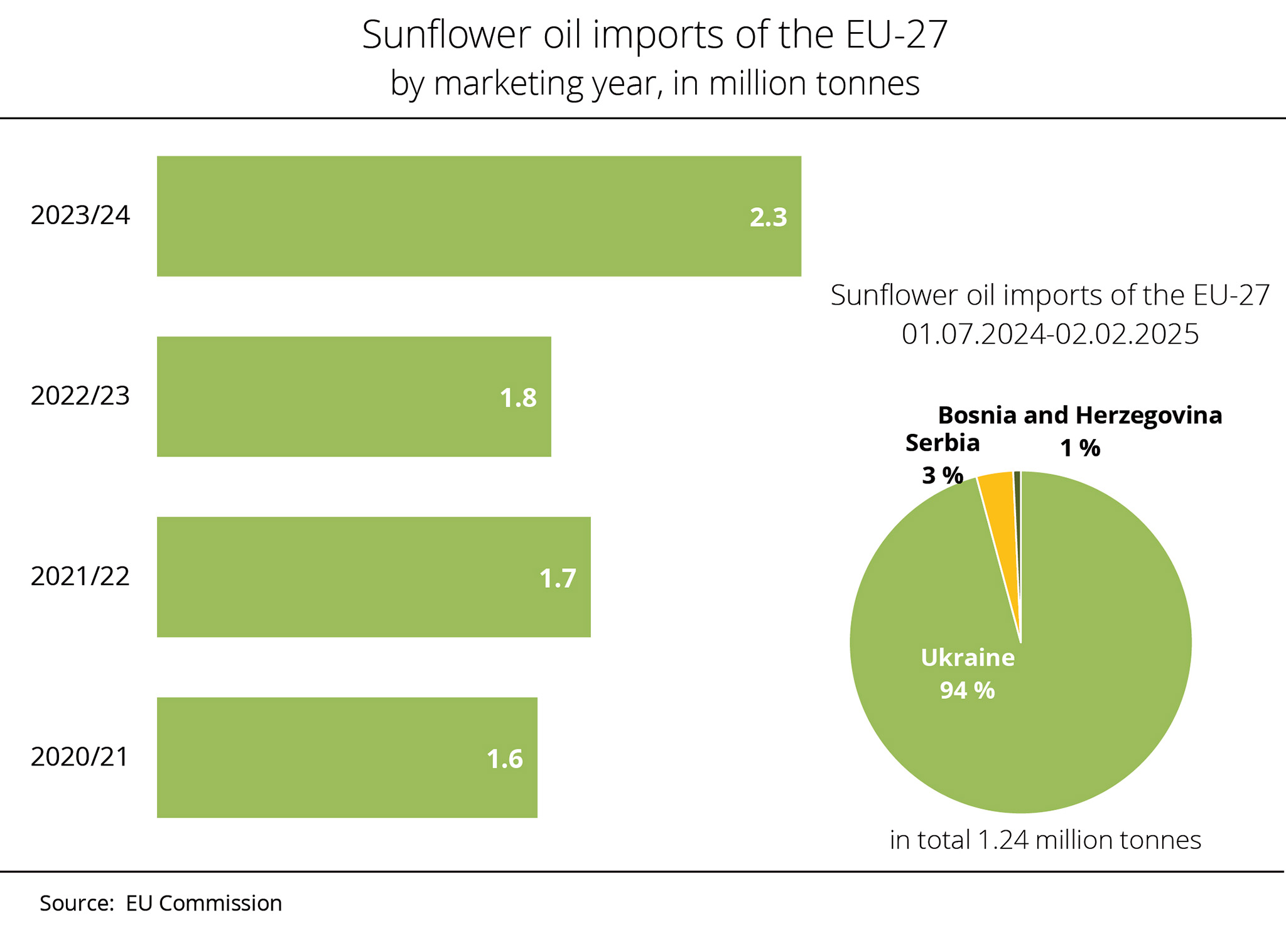

Ukraine supplies most of the EU's sunflower oil imports

According to the European Commission, Ukraine remains by far the most important supplier of sunflower oil to the EU-27. At the same time, feedstock supply in Ukraine is below last year's level.

From 1 July 2025 to 1 February 2026, the EU-27 imported just under 1.04 million tonnes of sunflower oil, representing a decline from 1.28 million tonnes during the same period in the previous year. Ukraine is by far the leading country of origin, delivering 0.95 million tonnes of sunflower oil to the EU so far this season. According to research by Agrarmarkt Informations-Gesellschaft (mbH), this translates to a market share of almost 92 per cent. However, the volume is significantly below the previous year’s level of 1.2 million tonnes, due to tighter domestic feedstock supply.

Ukraine’s sunflower seed harvest is estimated to have fallen year on year, from 13.0 million tonnes in 2024 to 10.5 million tonnes in 2025. This smaller crop has reduced processing volumes and limited the country's export potential for sunflower oil. In addition, Russia's attacks on infrastructure and port facilities have put pressure on logistics. Market reports indicate that export flows have recently stabilised. Moldova and Serbia are the second and third most important suppliers of sunflower oil, accounting for market shares of 5 per cent and just under 2 per cent, respectively. Moldova expanded deliveries year on year, whereas Serbia remained well below the previous year's level.

With spring sowing approaching and the grain market under pressure, the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) recommends that farms assess individually whether sunflower cultivation represents an economically viable option within diversified crop rotations. It is common knowledge that sunflowers are a robust crop, thriving even when water resources are scarce and requiring little fertiliser input.

Chart of the week (06 2026)

UFOP dismisses classification of soybeans as high-iLUC feedstock

The UFOP has dismissed the European Commission's initiative to classify soybeans as feedstock involving a high risk of indirect land use change (high-iLUC) in the future. This classification is proposed in the draft amendment to the Delegated Regulation (EU)2019/807. The EU Commission has initiated a public consultation process on this matter. The UFOP has specifically criticised the fact that, as a result of calculations relating to the expansion of agricultural cropland into areas with a high carbon stock, soybeans are classified across the board as “high-iLUC feedstock”. The UFOP has dismissed this approach, making reference to the applicable polluter-pays principle.

The association fears that an across-the-board classification would affect soybean farming in general, i.e. including production in the US or in Europe. According to the UFOP, the EU Commission would undermine the increasingly strict requirements for obtaining sustainability certifications, in particular the obligation to provide dated proof of land use. According to EU legislation, biofuels from cultivated biomass can only be counted towards climate objectives if it can be proven that the area in question was used as agricultural cropland prior to January 2008. The postponed EU Deforestation Regulation (EUDR) provides for a similar verification requirement. The UFOP has pointed out that these arrangements would no longer make sense in the case of soybeans.

The implications of classifying soybeans – rather than soybean oil, as is the case with palm oil – as a high-risk feedstock have not been adequately considered. According to the UFOP, the expansion of soybean farming is primarily driven by soybean meal, the soybean component that plays a decisive role in price formation. The association fears that an across-the-board classification would eliminate a major sales outlet in the biofuel sector, including for German and European soybean producers. At the same time, classifying soybeans as a high-risk feedstock does little to enhance the image of national and European protein strategies, which are also currently being developed, particularly with regard to greenhouse gas balance assessment. The UFOP has therefore called on the EU Commission to withdraw the draft and to discuss an impact evaluation with the trade associations.

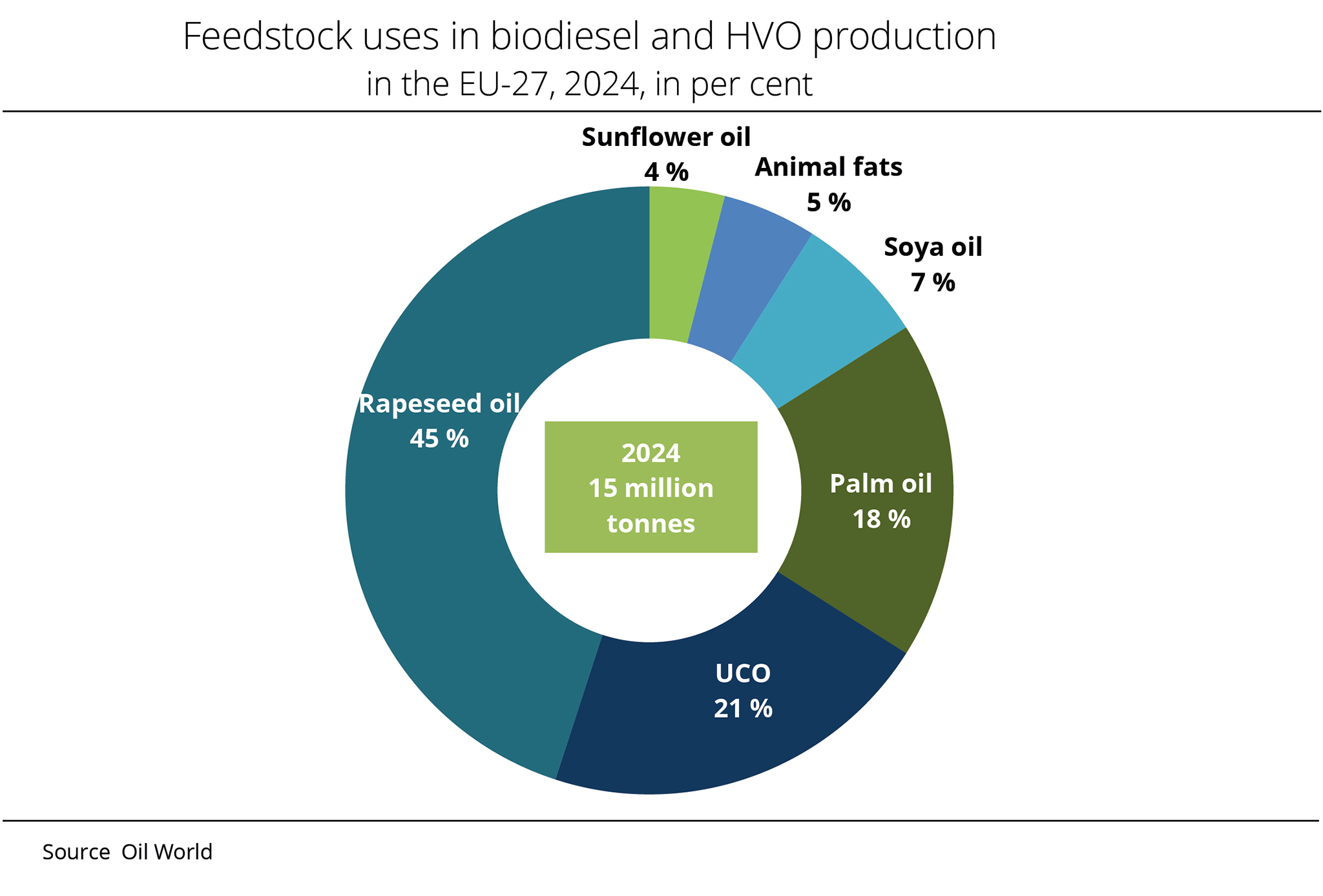

Regarding the significance of soybean oil as a biofuel feedstock in the EU, the UFOP has emphasised the substantial importance of rapeseed oil. Accounting for 45 per cent, this source is significantly more important than soybean oil, which accounts for only 7 per cent.

With an average oil share of 42 per cent, the biofuel market is a key factor in rapeseed pricing and, consequently, in European farmers' crop-choice decisions. The UFOP has pointed out that rapeseed cultivation is subject to crop rotation restrictions, meaning that rapeseed can only be grown on the same land every three to four years. As a rotation crop and Europe's most important source of protein, rapeseed makes a significant contribution to ensuring protein supply, enhancing soil quality and improving biodiversity. Plans exist to increase the importance of soybean cultivation in the future. However, at 7 per cent in 2024, the significance of soybeans in terms of biofuel consumption remains relatively low. Against this background, the UFOP has called for appropriate measures to tackle the root causes of deforestation to prevent further forest loss as far as possible and has urged for the application of the polluter-pays principle.

The association has drawn attention to the fact that the statistical basis for commodity shares varies significantly depending on the source used. This highlights the need for the EU Commission to improve official statistics. An EU database that also supports substantiated reporting would provide the required information.

Chart of the week (04 2026)

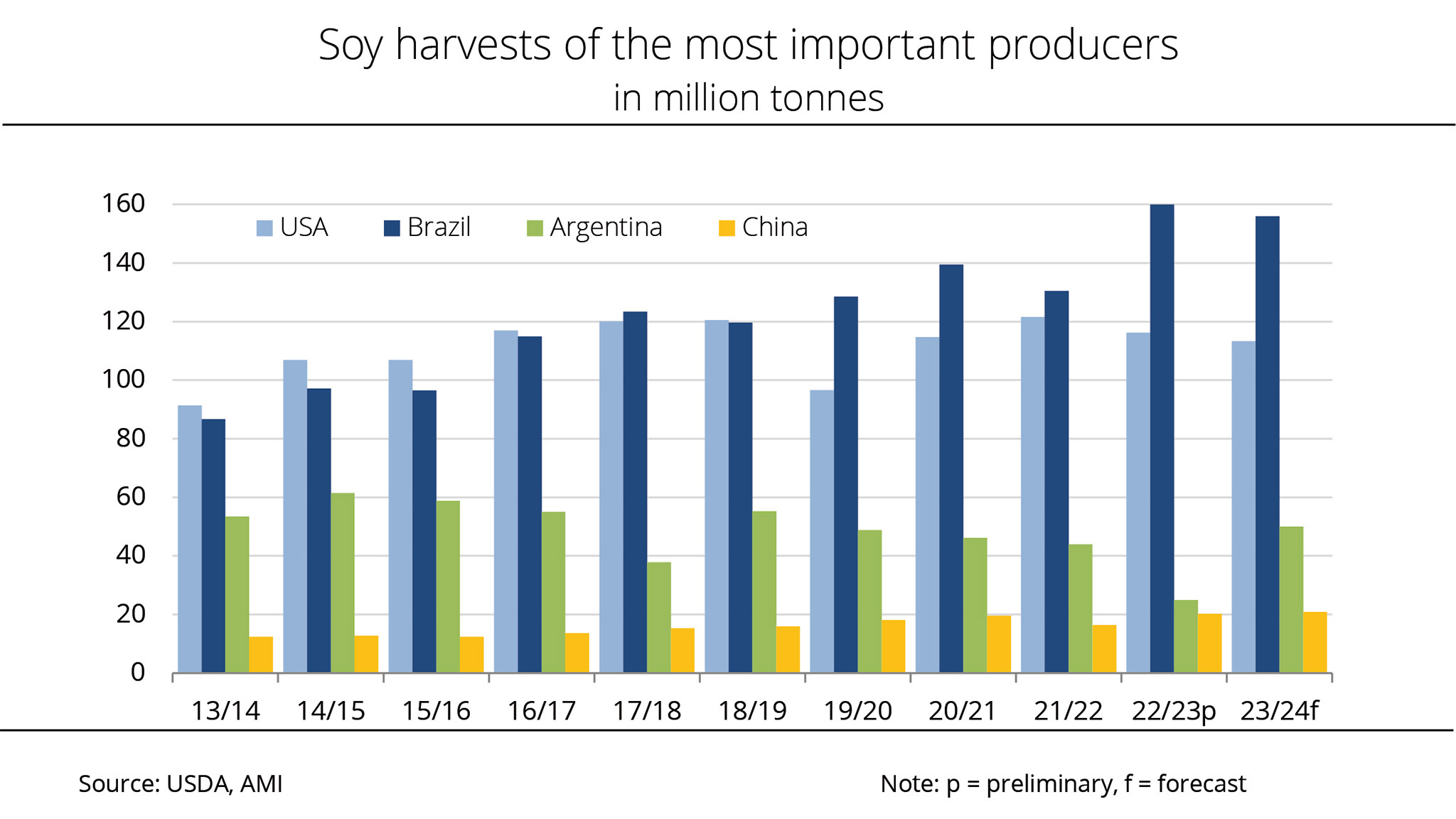

Brazilian soybean harvest set to hit another record high

South America is further consolidating its share of the global soybean market in this crop year. Brazil is expected to record another bumper crop, whereas the Argentine crop is projected to fall short of the previous year's output.

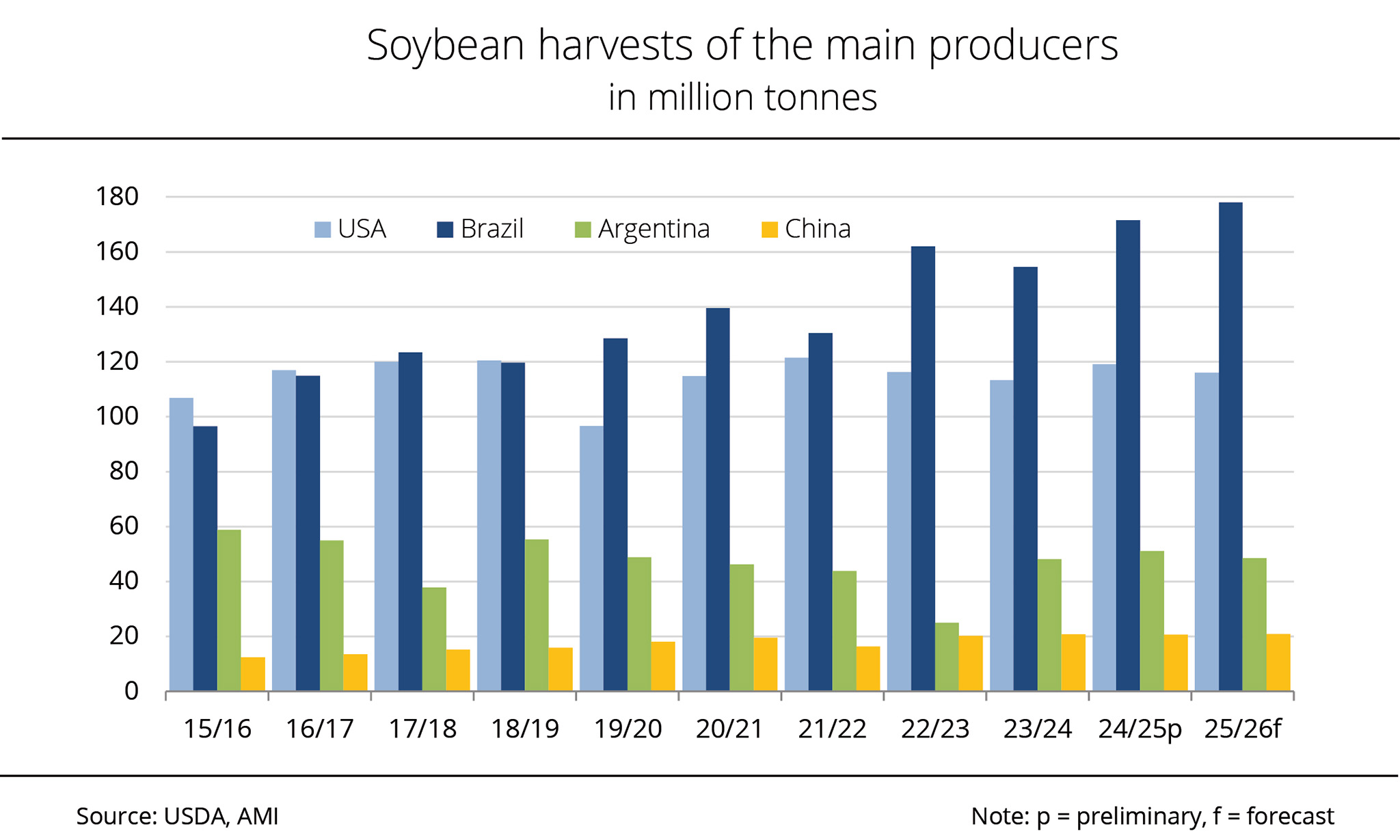

Brazil, the US and Argentina are the world's main producers of soybeans, collectively accounting for 80 per cent of global production. China follows a long way behind with a market share of 5 per cent. According to a USDA estimate, Brazil is expected to harvest an all-time record of 178 million tonnes of soybeans in the current crop year, which compares around 171.5 million tonnes in the previous year. Based on a 1.7 million hectare expansion of soybean area to 49.1 million hectares, Brazil is consolidating its position as the world's number one soybean producer ahead of the US. In the US, the soybean harvest was already complete by the end of 2025, totalling around 116.0 million tonnes. This translates to a year-on-year decline of roughly 3.1 million tonnes.

Argentina, which ranks third among the world's most important producers, is also projected to record a slightly smaller harvest than in the previous year. According to Agrarmarkt Informations-Gesellschaft (mbH), the country is expected to harvest 48.5 million tonnes, a decrease of around 2.6 million tonnes compared with the previous year. In contrast, the latest USDA estimates indicate that China's harvest will rise around 0.3 million tonnes from the previous year, reaching 20.9 million tonnes.

The Union zur Förderung von Oel- und Proteinpflanzen e.V. (UFOP) has voiced concerns about the continued expansion of cropland for soybean cultivation in Brazil, adding that even at this stage, it is clear that the European Regulation on deforestation-free products (EUDR) is ineffective, even though it has not yet formally entered into force. What is the use in proving crop area origin, if at the same time additional land is being cleared for soybean cultivation elsewhere? The UFOP interprets this situation as the reason behind the Brazilian Association of Vegetable Oil Industries' (ABIOVE) decision to end the soybean moratorium. The move was prompted by the adoption of a new law in the state of Mato Grosso which provides for the abolition of tax breaks for signatories to the moratorium. The UFOP hopes that the Supreme Federal Court will revoke the law in the ongoing judicial review.

In this context, the UFOP has drawn attention to the European Commission's report on changes in global production of relevant food and feed crops, submitted on 20 January 2021. Based on the evaluation of global land-use dynamics, the EU Commission concludes that soybean oil must be classified as an iLUC feedstock – as is already the case with palm oil. This means that from 2030 at the latest, biofuels derived from soybean oil, like palm oil fuels, can no longer be counted towards quota obligations in the EU. The UFOP has pointed out that Belgium and Denmark have already excluded soybean oil. However, from UFOP's perspective, this should be viewed critically, as soybeans are not grown to produce soybean oil as a feedstock for biofuels, but to produce animal feed. For this reason, biofuel legislation is not the right field of law.

Chart of the week (03 2026)

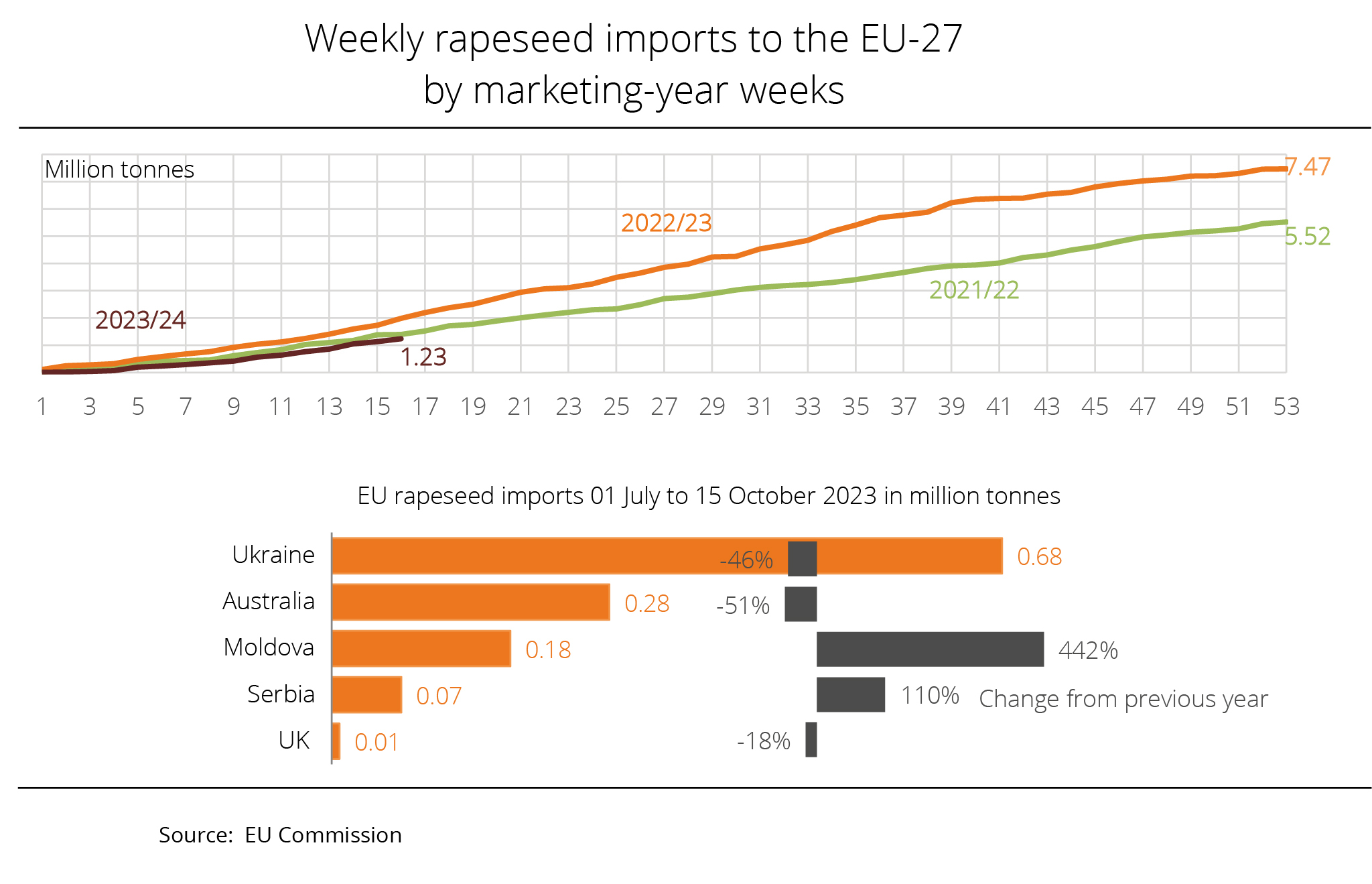

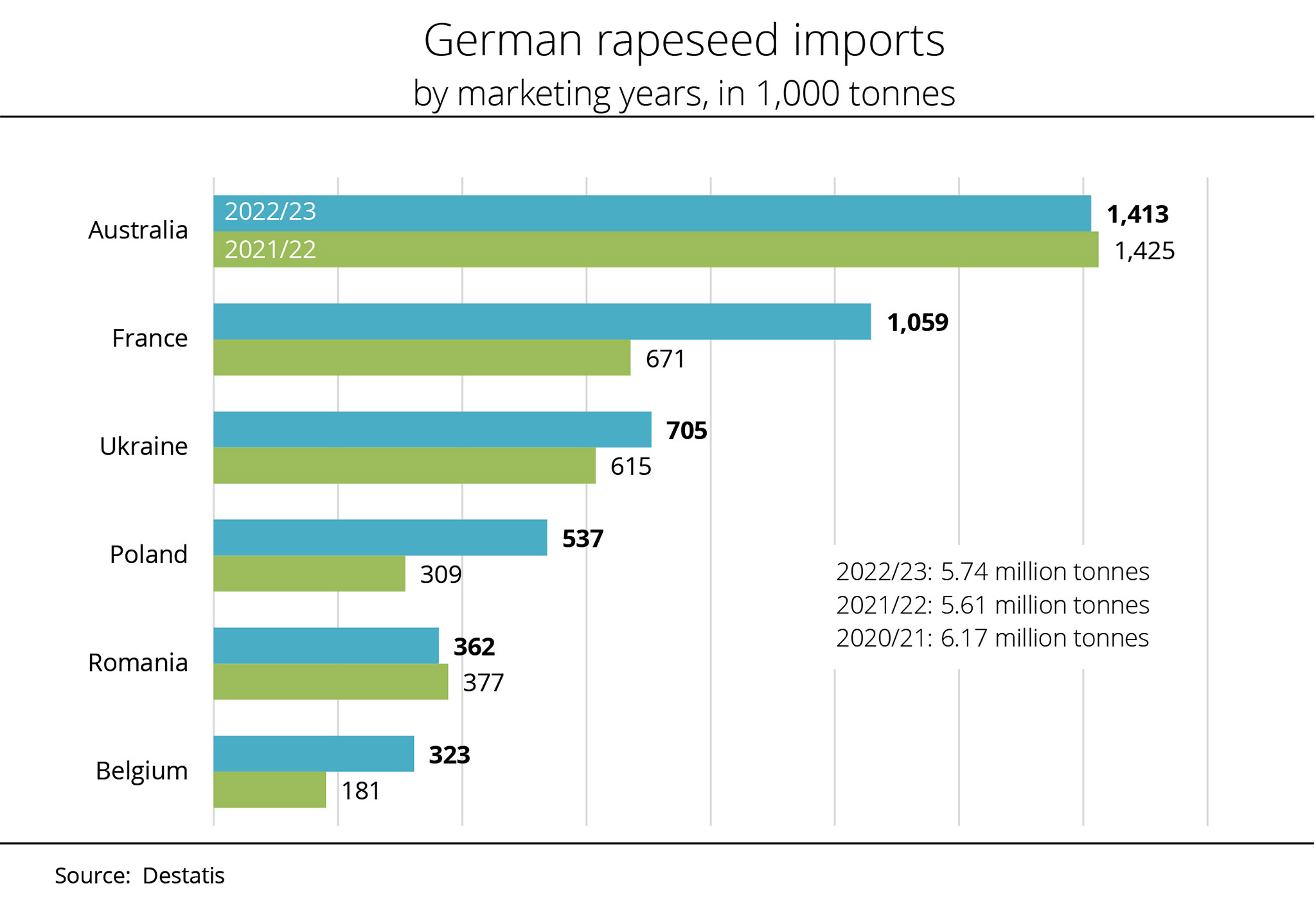

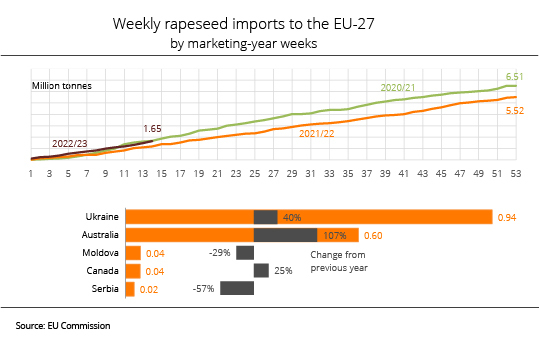

Demand for rapeseed imports declined due to an improved supply situation in the EU

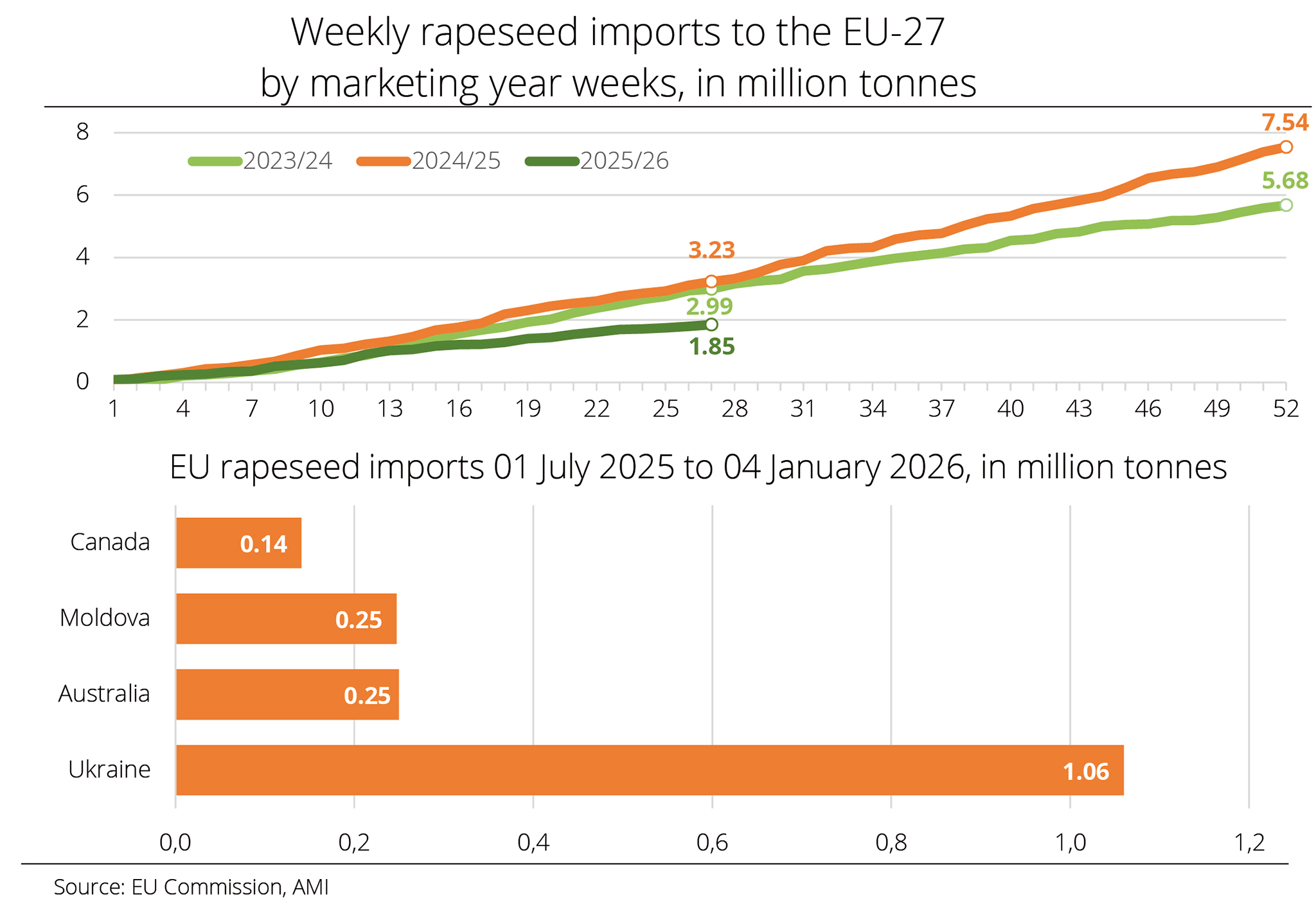

According to European Commission estimates, the rapeseed harvest in the EU-27 totalled around 20.16 million tonnes in 2025. This translates to a significant increase in supply compared to the previous year's substandard 16.77 million tonnes. With the rapeseed processing volume expected to reach around 24.68 million tonnes, it also makes the EU less dependent on imports.

Cumulative imports into the EU-27 in the first half of the crop year 2025/26 amounted to approximately 1.85 million tonnes, representing a nearly 43 per cent decline from the previous year's level of 3.23 million tonnes. Ukraine remains the leading supplier country with just over 1.06 million tonnes to date and a 57 per cent share of imports. Nevertheless, the country's shipments remain clearly below the previous year's volume of 2.02 million tonnes.

The second wave of imports from Australia will increasingly come into focus later on in the season. By January, Australia had placed 249,869 tonnes of rapeseed on the EU market, ranking second among the major countries of origin with a share of just under 14 per cent, but trailing well behind Ukraine. According to investigations conducted by Agrarmarkt Informations-Gesellschaft (mbH), deliveries remained approximately 71 per cent below the level recorded in the reference period.

Canada continued to lose market share. The country delivered 140,915 tonnes of rapeseed to date, which compares to 161,347 tonnes the previous year. Because Canadian farmers grow genetically modified varieties, the use of rapeseed oil derived from Canadian rapeseed is restricted in the EU. As a result, imports from Canada are primarily used for biofuel production.

By contrast, Moldova and Serbia ramped up their deliveries significantly compared to the first half of the crop year 2024/25, supplying 247,357 tonnes (previous year: 85,611 tonnes) and 114,171 tonnes (previous year: 44,501 tonnes), respectively. Some of the rapeseed imports declared as Moldovan are likely to be of Ukrainian origin, reflecting changes in transit and trade routes.

Chart of the week (02 2026)

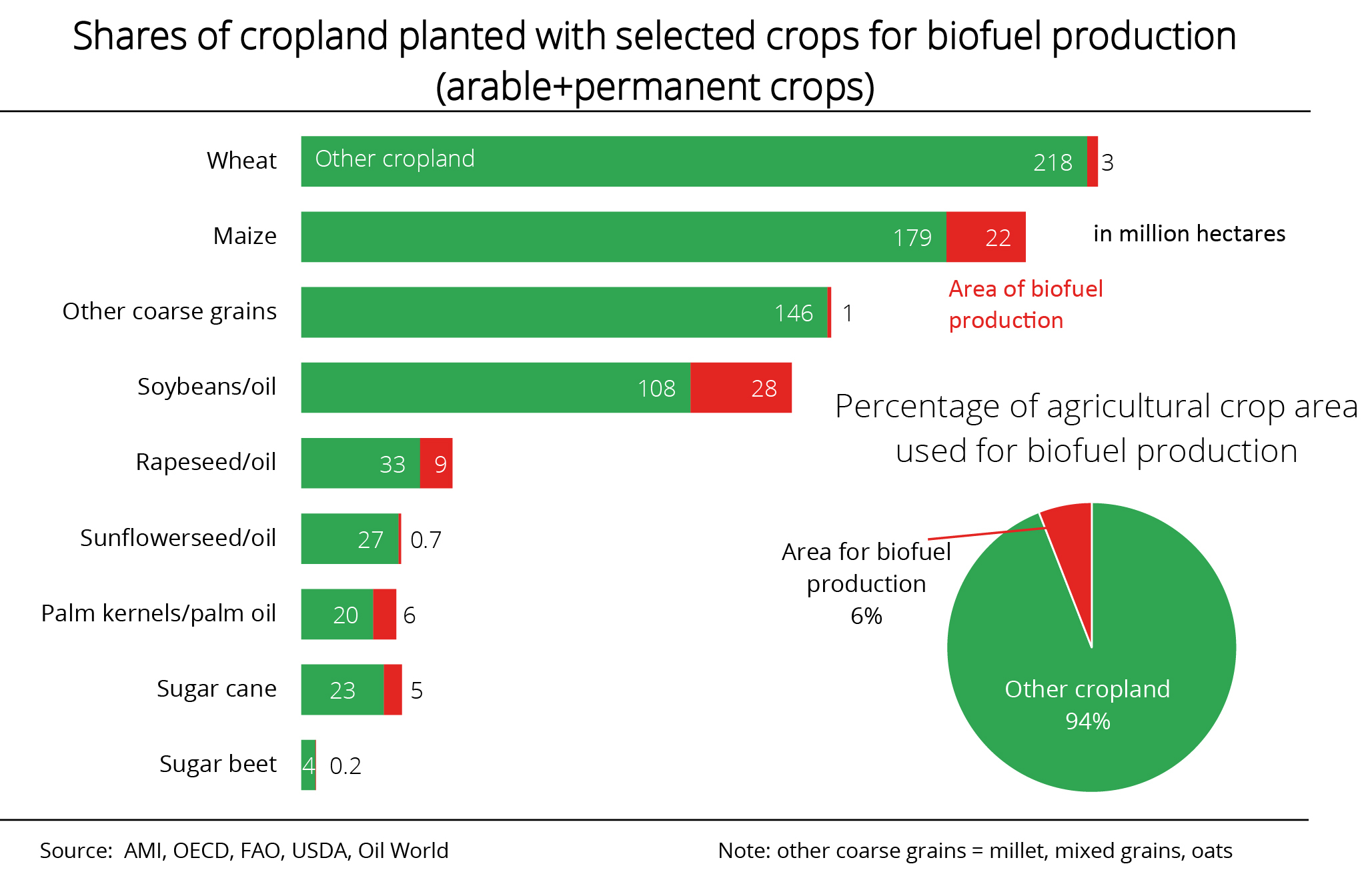

Assessing demand for cropland for biofuels properly

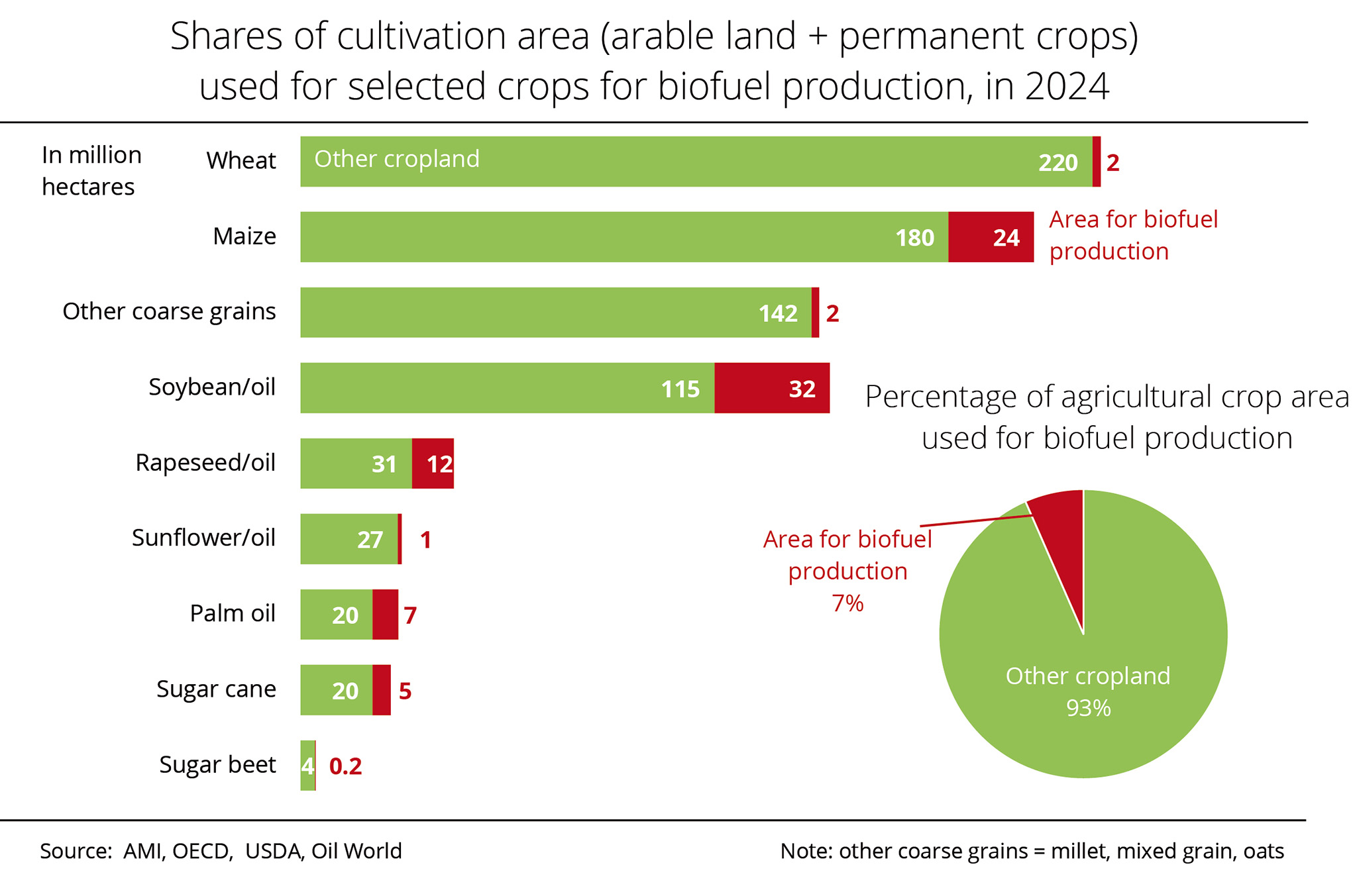

Crop plants were grown on just over 1.2 billion hectares worldwide in 2024. These include grain, oilseeds, protein, sugar and fibre plants, as well as fruits, vegetables, and nuts. The largest share was used directly or indirectly, via livestock feed, for human nutrition. The cultivation of feedstocks for biofuel production accounted for only about 7 per cent of the cultivated land.

Most biofuels are produced in regions with a structural feedstock surplus, specifically, sugar, maize, palm oil and soybean oil. In the absence of this way of processing, considerable volumes would have to be placed on the world market, which, in turn, would have a negative impact on producer prices globally. In other words, processing these feedstocks into biofuels contributes to reducing surpluses as well as generating additional value added. According to Agrarmarkt Informations-Gesellschaft (mbH), at the same time the use of biofuels reduces the need for imports of crude oil or fossil fuel in many countries.

From the perspective of the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP), another effect of biofuel production is that it also yields high-quality protein feed, which is in high demand, and glycerin for the chemical industry. These volumes and their quality influence commodity prices and therefore also have a bearing on the expansion or reduction of cultivation areas, particularly in the case of soybean. UFOP has stated that biofuels are not a factor driving commodity prices. The corresponding feedstock can be redirected to food use at any time as and when needed. For example, at the beginning of the Russian attack on Ukraine rapeseed oil replaced previously imported sunflower seed oil.

If arable farming were to be extensified for political reasons – an aim the EU Commission is pursuing with the reduction strategy for fertilisers and plant protection products under the Green Deal – this option of "buffering" food demand would no longer be available. UFOP has pointed out that the cultivation area would need to be expanded to close this demand gap. As the European and national bioeconomy strategies are being developed, the focus should shift towards advanced and ambitious concepts for a comprehensive appraisal of commodity chains, starting from plant breeding and cultivation. UFOP has called for a careful orchestration of the full set of tools.

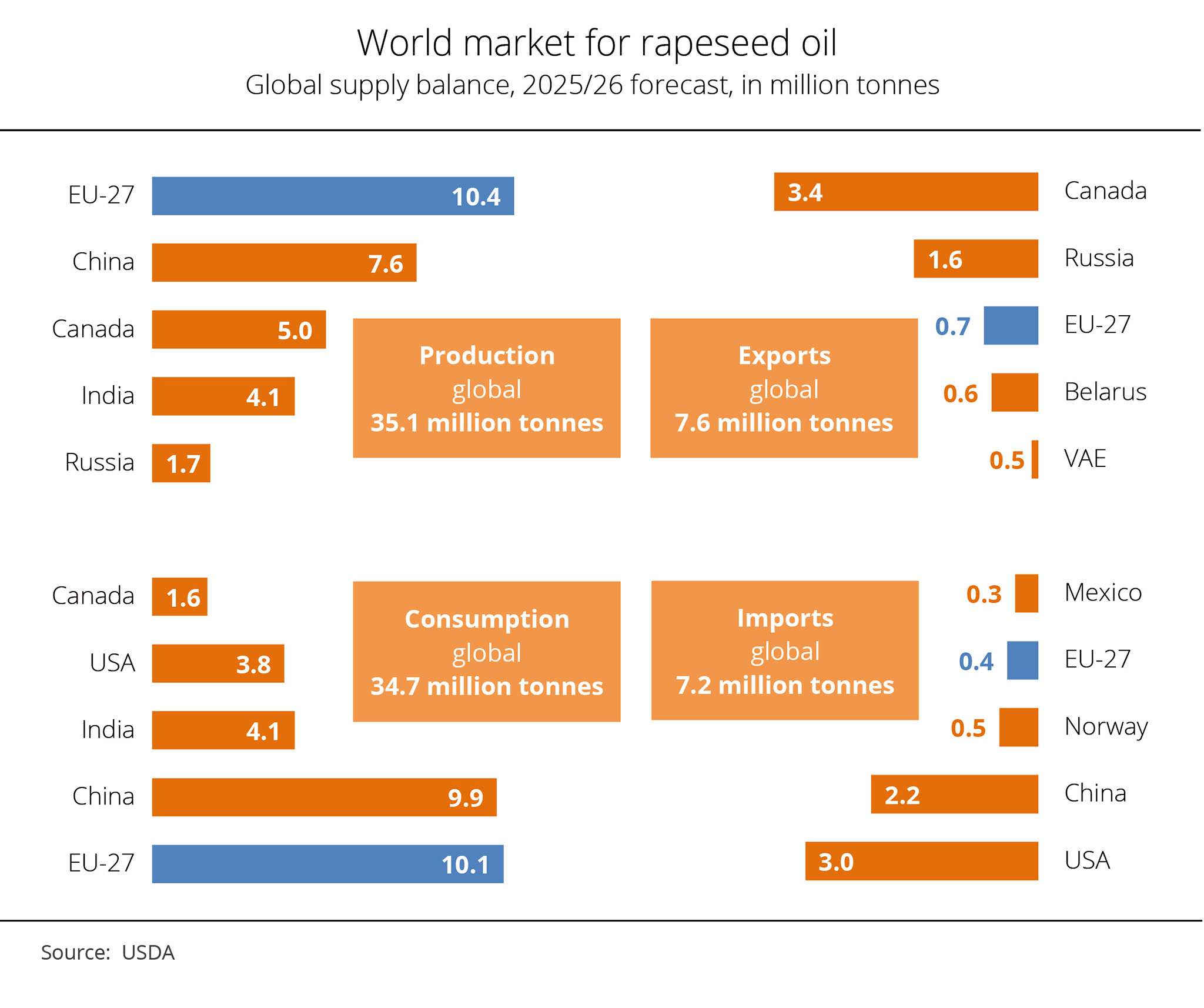

Chart of the week (51 2025)

EU remains leading rapeseed oil producer

Berlin, 17 December 2025. – The EU remains the world's largest producer and consumer of rapeseed oil. China follows, unable to meet its demand entirely from domestic production and therefore having to rely on imports. However, imports have become more difficult due to the trade dispute with Canada.

The US Department of Agriculture (USDA) estimates global rapeseed oil output in the 2025/26 crop year at approximately 35.1 million tonnes, which represents an increase of around 1.4 million tonnes compared with the previous season. The EU is the largest consumer at just under 10.1 million tonnes, followed by China at 9.9 million tonnes and India at 4.1 million tonnes. The US is the largest rapeseed oil importer with imports amounting to 3.0 million tonnes, partly for biofuel production. While EU member states are virtually self-sufficient, China has to import 2.2 million tonnes.

While the US has settled its trade dispute with Canada, the largest global rapeseed oil exporter, as part of its biofuels policy, China's trade conflict with Canada continues. In March 2025, China imposed import duties of 100 per cent on Canadian rapeseed oil imports in response to duties Canada had imposed on imports of electric vehicles from China in the summer of 2024. For this reason, China has had to import rapeseed oil from other countries, which has led to appreciable changes in trade flows.

Chart of the week (50 2025)

EU Commission expects smaller soybean output

An updated estimate by the EU Commission suggests that this year’s soybean harvest in the EU-27 falls slightly short of the previous year's level, following a reduction in cultivation area for the 2025 harvest. The expected yield increases cannot offset this decline in area.

An updated estimate by the EU Commission suggests that this year’s soybean harvest in the EU-27 falls slightly short of the previous year's level, following a reduction in cultivation area for the 2025 harvest. The expected yield increases cannot offset this decline in area.

In its latest estimate, the EU Commission marginally raised its forecast for soybean production in the EU. According to this information, the 2025 harvest is up about 18,000 tonnes on the October estimate, reaching just under 2.9 million tonnes. Nevertheless, this still represents an estimated decrease of 106,000 tonnes year-on-year. The drop is due to a 7 per cent reduction in area planted, as average yields are expected to exceed the previous year's level of 26.8 decitonnes per hectare, as well as the long-term average, rising to 27.8 decitonnes per hectare.

Italy remains the EU's leading soybean-producing country, with output totalling 1.1 million tonnes, followed by France with 387,000 tonnes. Harvests in the Balkan states are projected to fall short of the previous year's levels. This especially applies to Romania with an output of 245,000 tonnes – representing a year-on-year decrease of 54,000 tonnes – despite a 12 per cent reduction in area. According to research by Agrarmarkt Informations-Gesellschaft (mbH), German farmers harvested 134,000 tonnes of soybeans, representing an almost 2 per cent increase compared with 2024.

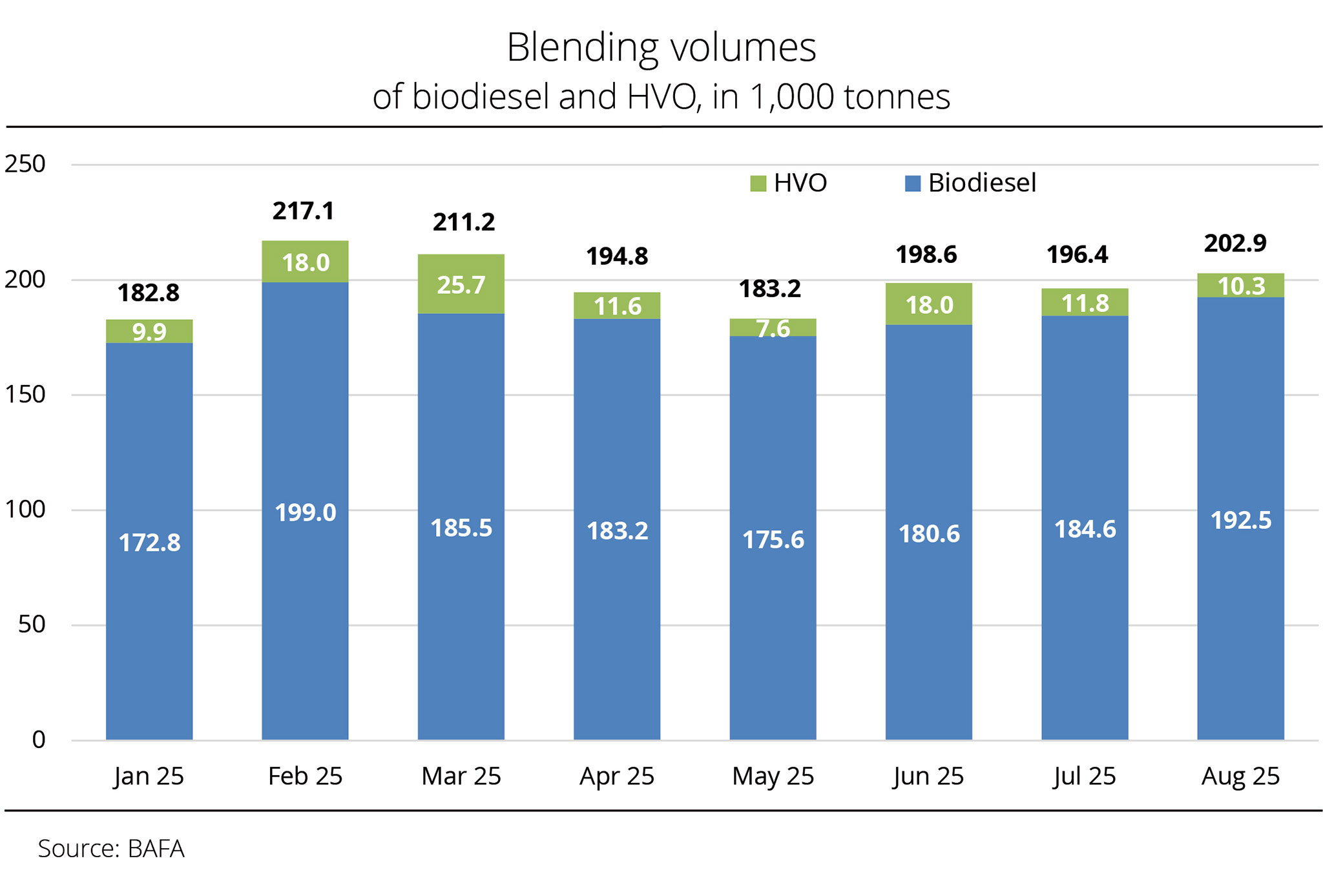

Chart of the week (49 2025)

BAFA enhances transparency in the blending market and now also reports HVO volumes

After a long interruption, the Federal Office for Economic Affairs and Export Control (BAFA) has published the biofuels consumption figures up to August 2025. For the first time, the data also include HVO volumes. BAFA thus meets the call for greater transparency in the blending market that the Union zur Förderung von Oel- und Proteinpflanzen e. V. (UFOP) has repeatedly issued.

In August 2025, biodiesel consumption increased just over 3 per cent on the previous month, reaching 202,900 tonnes while still falling 3 per cent short of the previous year's figure. The HVO volume amounted to approximately 10,340 tonnes, around 12 per cent below the July level. Since at the same time, consumption of diesel fuel decreased 8 per cent, the HVO share in blends rose 0.7 per cent to 7.3 per cent.

In the first eight months of 2025, the use of biodiesel for blending totalled just under 1.6 million tonnes, a decrease of around 2 per cent on the same period last year according to research by Agrarmarkt Informations-Gesellschaft (mbH). The HVO volume reached 112,888 tonnes, also slightly below the previous year's 117,500 tonnes. Consumption of diesel fuel in the period January to August added up to roughly 20.2 million tonnes, exceeding the previous year's level by nearly 2 per cent. Against this background, the incorporation rate decreased 0.2 per cent year-on-year, falling to 7.3 per cent.

The UFOP has justified its call for transparency with the expected increase in importance of HVO as a so-called drop-in fuel, since the incorporation rate of biodiesel in diesel fuel is capped at 7 per cent by volume. HVO, on the other hand, can be blended at rates up to 26 per cent without violating the DIN EN 590 diesel fuel standard. The rising greenhouse gas quota obligations in the draft bill currently under discussion to amend greenhouse gas quota legislation – up to 53 per cent in 2040 –, together with the concurrent ramp-up of e-mobility, primarily support the increased use of HVO.

Chart of the week (48 2025)

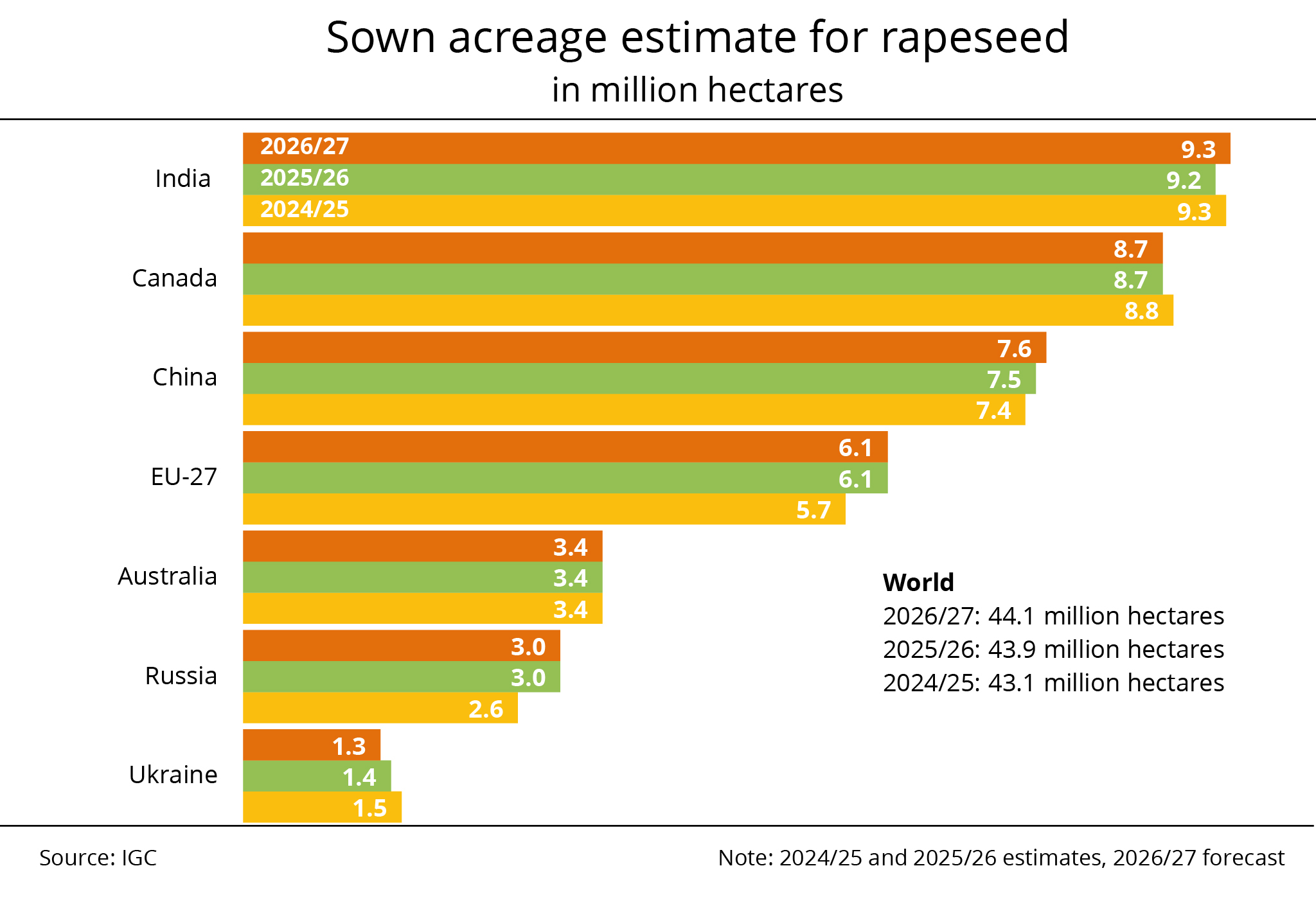

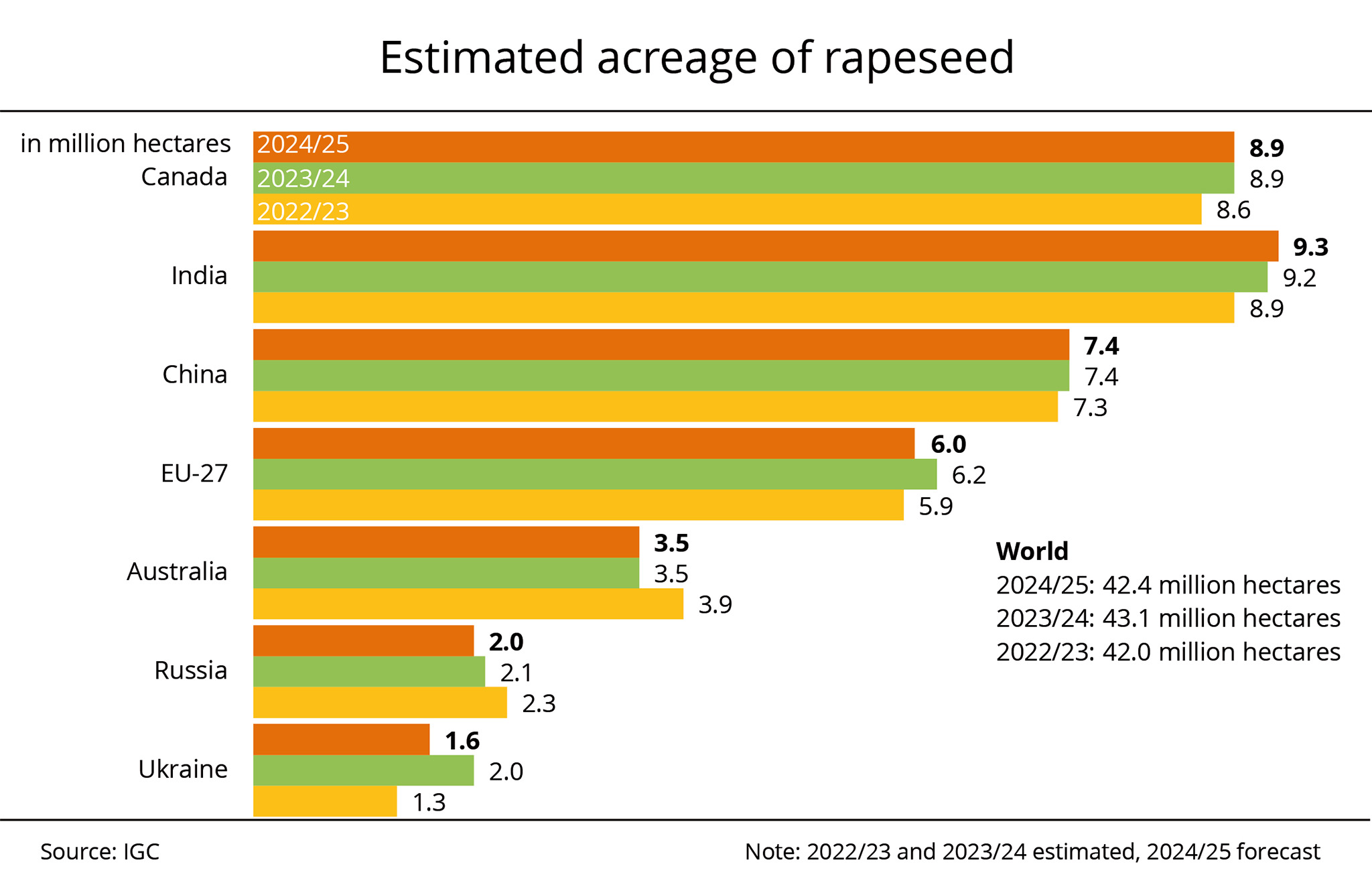

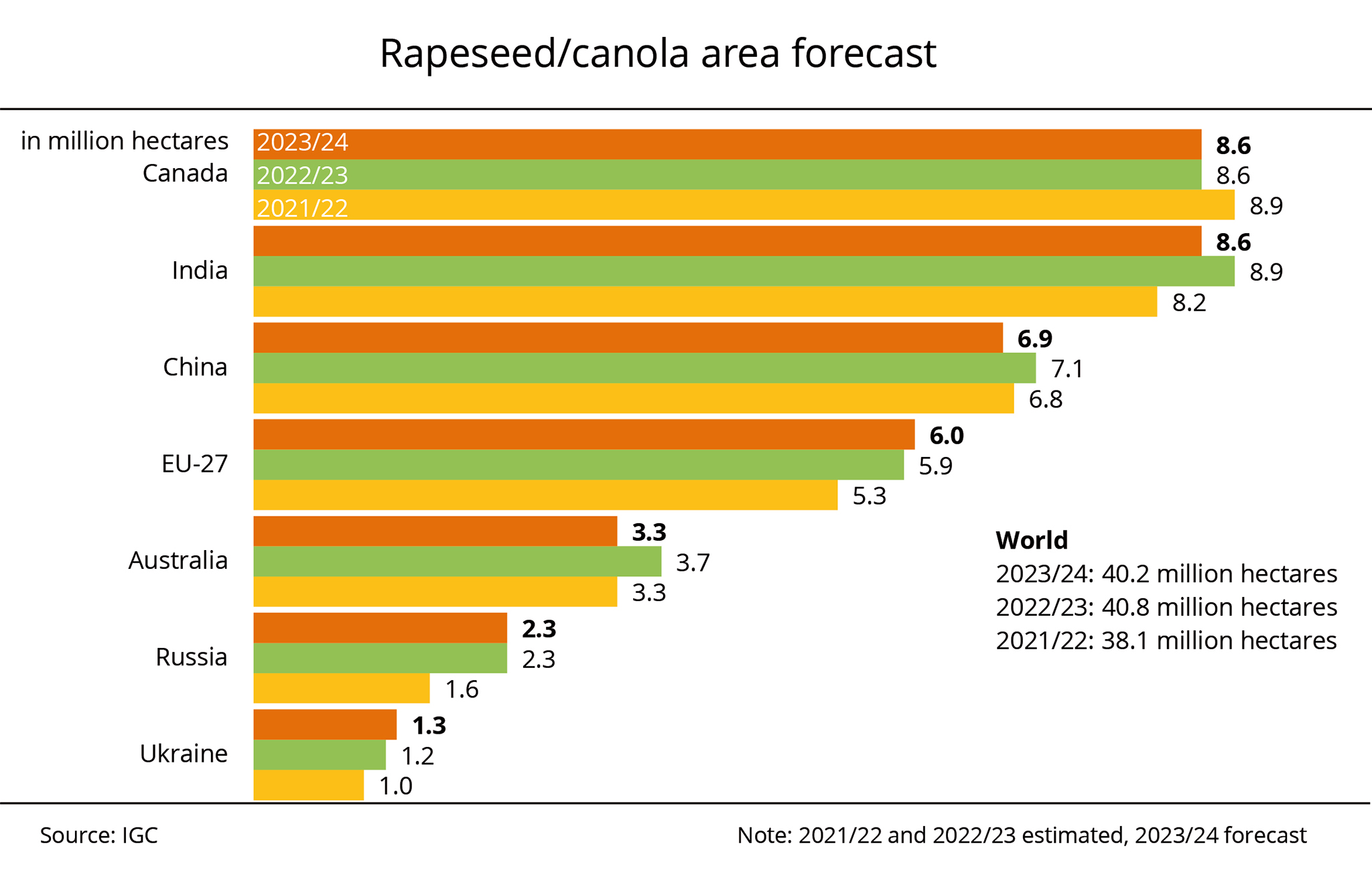

IGC expects all-time high in rapeseed area for the 2026/27 marketing year

In its latest estimate, the International Grains Council (IGC) forecasts the global rapeseed area at 44.1 million hectares. This would mark an increase of 0.2 million hectares compared to the current 2025/26 crop year. In major exporting countries, the rapeseed area is expected to decline slightly, while other regions – especially Asia – are projected to see moderate expansion.

In the EU-27, the rapeseed area is forecast to remain unchanged at 6.1 million hectares. However, in the southeastern EU, especially in Romania, the strong 2025 harvest may encourage farmers to expand their rapeseed plantings. In contrast, other member states are expected to reduce their areas slightly.

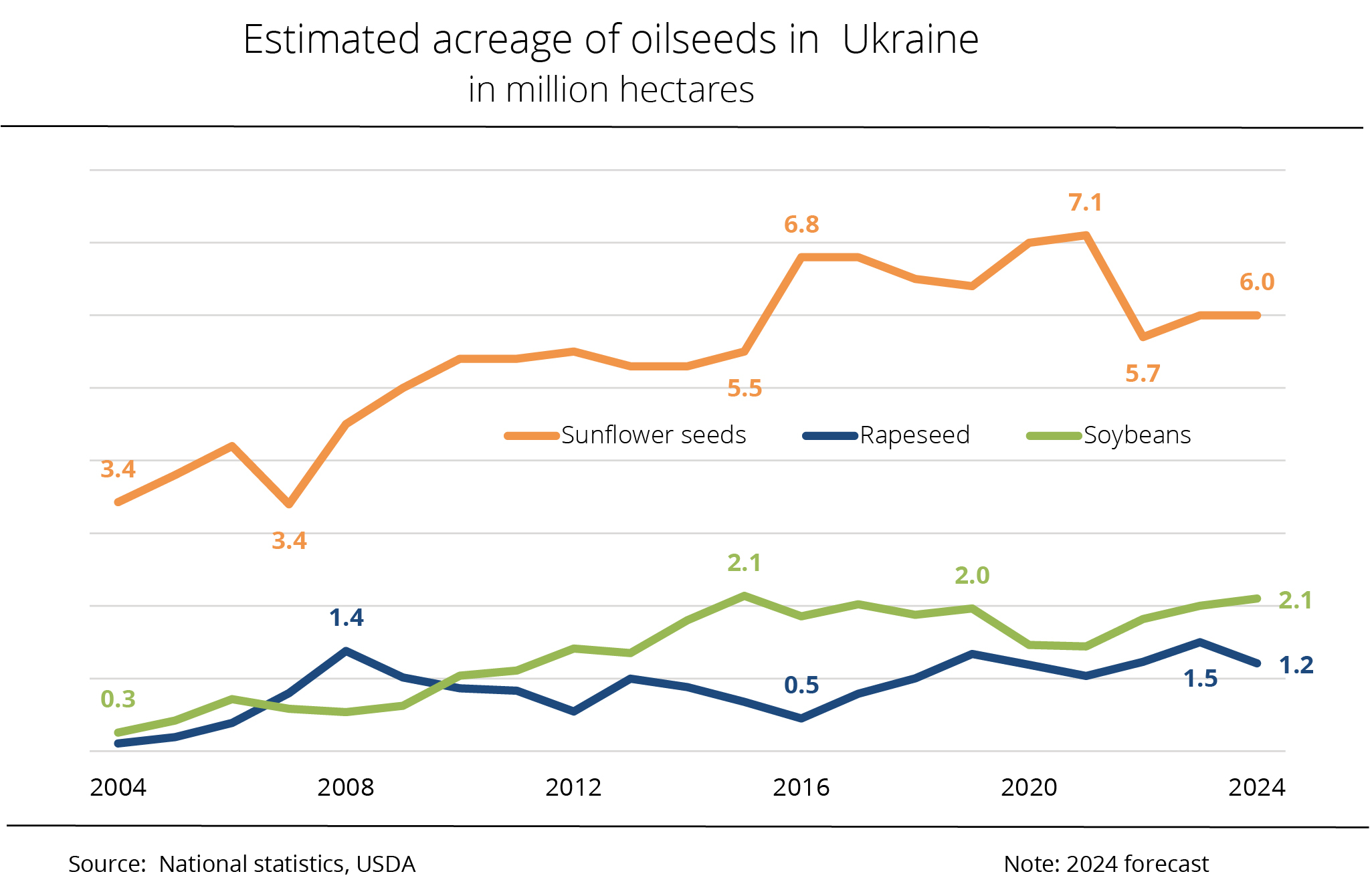

In Russia, the area devoted to rapeseed cultivation is forecast to remain stable at 3.0 million hectares, following significant expansion in the current season. By contrast, according to research by Agrarmarkt Informations-Gesellschaft (mbH), the area planted with rapeseed in Ukraine is expected to decline 100,000 hectares to 1.3 million hectares. Nevertheless, the aggregated area in the Commonwealth of Independent States (CIS) is expected to reach the second largest level on record, underscoring the growing importance of rapeseed as a crop.

Forecasts for leading exporters Canada and Australia remain particularly uncertain, as sowing will not begin for several months. Driven by expectations of brisk international demand, Canada's rapeseed area is projected to remain close to its previous average at 8.7 million hectares. Australia's rapeseed area is likewise expected to stay unchanged compared to the previous year, at 3.4 million hectares.

Chart of the week (47 2025)

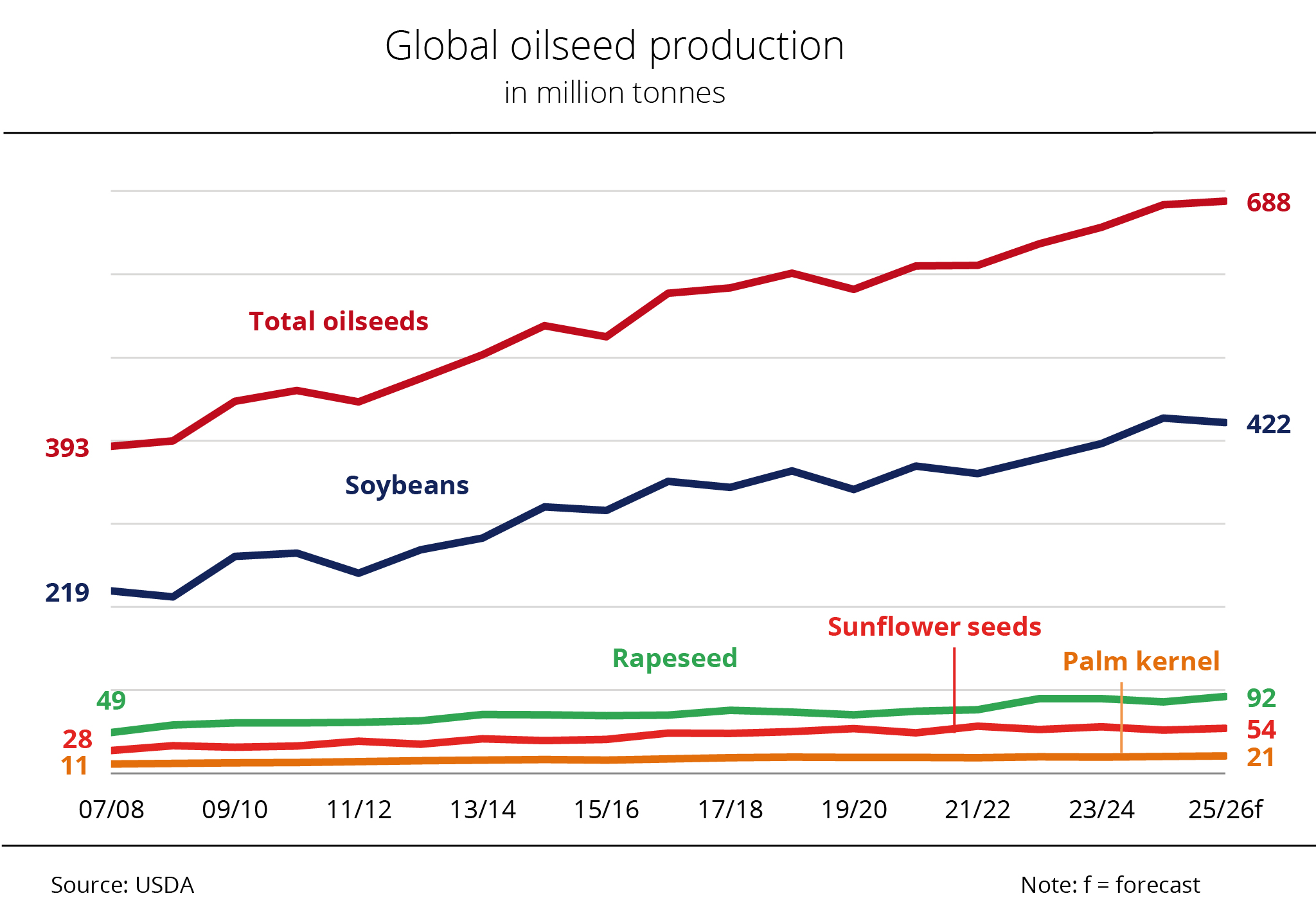

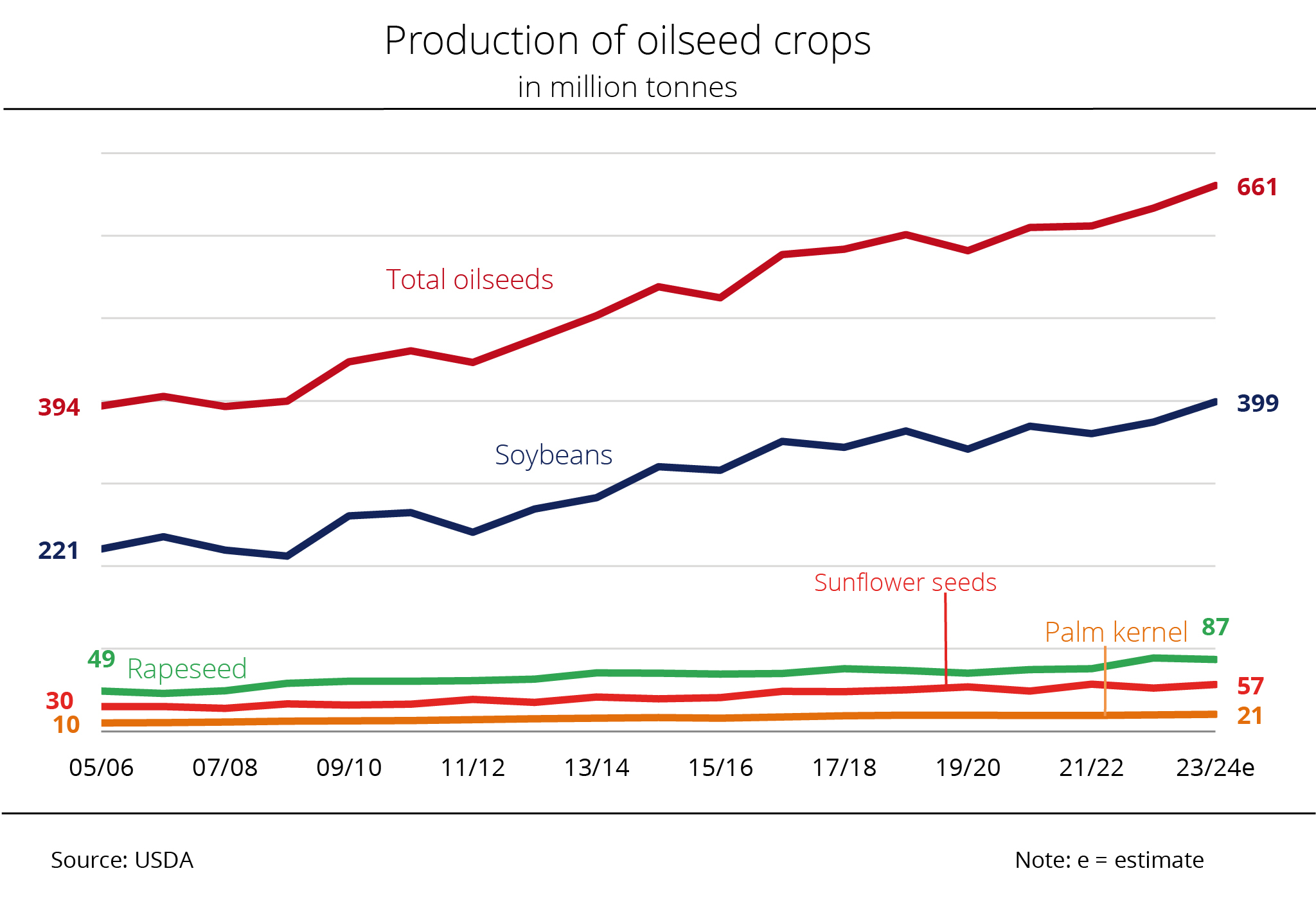

USDA expects record year for oilseed production

Rapeseed harvest to reach all-time high